Solid Fuel Testing Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

PW Consulting’s new market study on Solid Fuel Testing presents a forward-looking, actionable playbook for decision-makers preparing for 2026 and beyond. Grounded in five years of historical tracking and a detailed forecast through 2032, this preview summarizes the strategic value embedded in the full report: a combination of macro clarity, scenario-driven operational guidance, and competitive intelligence that enables commercial, technical, and regulatory leaders to prioritize investments and partnerships while preserving commercial sensitivity.

Solid Fuel Testing Market

Market snapshot: what the headline numbers mean for strategy

Our base-year sizing for 2025 places the global solid fuel testing market at USD 482.5 Million, with an initial uplift expected in 2026 to roughly USD 502.5 Million. PW Consulting’s forecast horizon (2026–2032) anticipates a compound annual growth rate (CAGR) of 4.59%, taking the market toward approximately USD 661.0 Million by 2032 under the central scenario. That steady growth masks material structural change: demand drivers are shifting from purely volumetric testing towards integrated quality, traceability, and sustainability verification services.

Solid Fuel Testing Market

- Moderate, predictable expansion (mid-single-digit CAGR) creates room to transform margin profiles through service differentiation rather than relying on volumetric throughput alone.

- Near-term inflection points — regulatory updates, renewable fuel mandates, and accelerated feedstock diversity — will determine which participants capture premium pricing for advanced analytical and certification services.

Why this matters for 2026 corporate decisions

- Regulatory timing equals commercial windows: Several regulatory developments scheduled for 2026–2027 (notably adjustments to renewable fuel volumes and emissions standard revisions) will create discrete demand surges for verification, re-testing, and compliance advisory services. Companies that align lab capacity and compliance offerings with these windows can secure higher utilization and pricing.

- Feedstock diversification increases testing complexity: As industrial consumers and fuel suppliers incorporate higher shares of biomass and waste-derived fuels, testing requirements expand beyond proximate and calorific assays to include chloride, trace elements, and specialized petrography for certain blends.

- Value migration to data and proof: Buyers are willing to pay for traceable, auditable data chains — mobile sampling to certified lab analysis to digitally signed certificates — especially where sustainability premiums are at stake.

- Regional supply chains matter: While global laboratories and networks will continue to serve multinational flows, regional and port-adjacent capabilities remain essential for rapid turnaround and chain-of-custody integrity.

What the PW Consulting report delivers (practical, operational outputs)

- Actionable market model: a scenario-ready revenue model covering 2026–2032 that supports custom sensitivity testing. The model is provided in a format executives can adapt to their own throughput or pricing assumptions.

- Three scenario frameworks: Central (policy-stable), Upside (accelerated renewables and stricter emissions), and Downside (demand compression). Each scenario maps to operational KPIs — utilization, mix-shift to advanced testing, and margin impact.

- Service stack economics: margin-by-service archetypes (basic compositional testing vs. advanced trace-element/traceability services), with recommended pricing levers and cost-to-serve thresholds to protect margins as volumes fluctuate.

- Go-to-market playbook for labs and service providers: prioritized investments (mobile sampling fleets, ISO/IEC 17025 accreditations, LIMS upgrades), partnership templates with ports and fuel aggregators, and a tactical M&A scorecard for acquiring specialist capabilities.

- Regulatory-compliance matrix: mapping of major standards and testing requirements to business processes — a practical checklist for compliance teams and procurement groups preparing for 2026 rule changes.

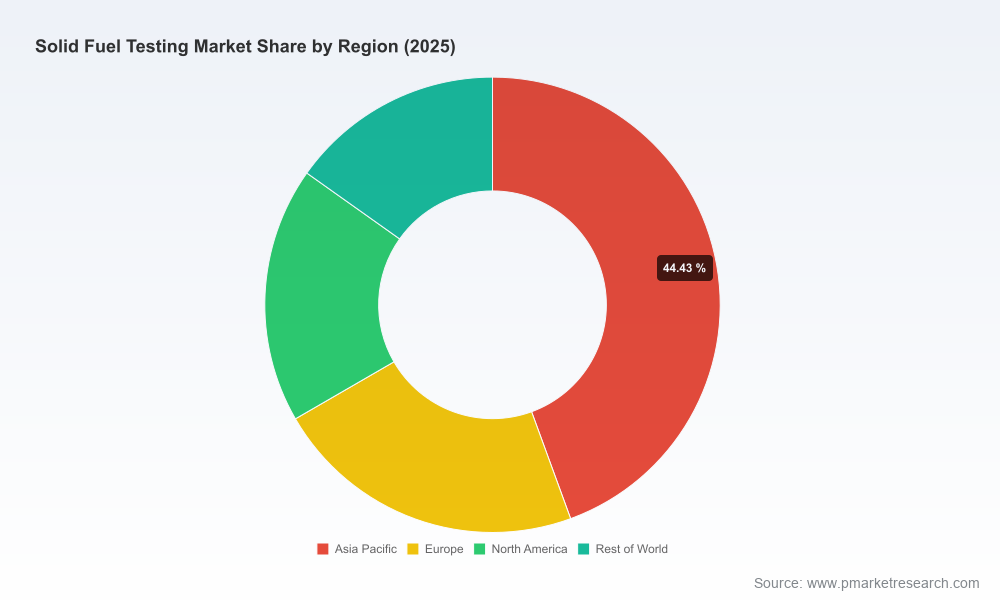

- Vendor and capability benchmarking: qualitative profiles and capability maps that highlight where global integrators compete with nimble regional specialists (note: detailed revenue splits and region-by-application figures are reserved for the full report).

Competitive landscape — concise strategic assessments

The market combines large, global testing networks with a deep bench of regional specialists. Leading players maintain broad, vertically integrated service portfolios and significant lab networks; niche laboratories focus on speed, local presence, and specialist methods. Key firms highlighted in the study include Intertek, SGS, Bureau Veritas, ALS, AmSpec, Control Union, McCreath Laboratories, and Standard Laboratories. Our qualitative assessment identifies strategic vectors for each cohort:

Solid Fuel Testing Market

- Global integrators (e.g., Intertek, SGS, Bureau Veritas): These firms leverage global sampling networks, standardized processes, and cross-border certifications. Their advantage is end-to-end visibility for multinational trade flows and large-volume customers. Recent capability additions — including enhanced sustainable fuel analysis at major centers — demonstrate intent to capture higher-value verification work linked to sustainability claims.

- Regional specialists (e.g., ALS, McCreath, Standard Laboratories): These players secure competitive advantage through fast turnaround, port proximity, and deep relationships with local commodity handlers. Their business is resilient to short-term policy noise and attractive to buyers prioritizing speed and chain-of-custody.

- Biofuel-focused providers (e.g., AmSpec, Control Union): Specialization in biomass and biofuel testing — including ISO 17025-accredited labs in strategic export markets — positions these firms to capture the growing verification load from renewable fuels and sustainability certification needs.

Collectively, the market is moderately concentrated: a handful of global players control a material portion of revenue, while numerous regional and niche labs retain strong local market positions. This structure creates opportunities for bolt-on M&A, selective capacity expansion, and differentiated service propositions without large-scale price wars — provided firms follow disciplined go-to-market strategies.

Strategic priorities for 2026 — recommended actions

- For labs and service providers: Fast-track investment in digital LIMS and certificate-of-analysis automation to capture margin on traceability services. Prioritize mobile sampling assets and port-located micro-labs to shorten lead times and protect premium business.

- For industrial fuel consumers (utilities, steel, cement): Centralize testing procurement and require auditable chain-of-custody as a condition of supplier contracts. Invest in in-house spot-testing capabilities for rapid acceptance decisions while outsourcing complex trace-element work.

- For traders and commodity handlers: Use third-party validated testing as a value-differentiator in contract terms. Consider co-investing with testing partners in port-side sampling to reduce acceptance disputes and inventory risk.

- For investors and M&A teams: Target regional leaders with strong port relationships, or niche labs offering advanced analytics for biomass and waste-derived fuels. The most accretive acquisitions are those that add differentiated services or dramatically shorten service delivery time.

- For compliance teams and policy-facing organizations: Map upcoming rule timelines to testing capacity and reallocation needs — particularly in years with updated renewable fuel volumes or emissions rules — and secure contingency lab capacity ahead of enforcement milestones.

Risk scenarios and indicators to monitor

- Regulatory shifts: track rulemakings and final volumes for renewable fuel programs and emissions standards — these dictate demand timing and technical scope.

- Feedstock mix: monitor the pace of biomass and waste-derived fuel uptake in heavy industries; faster adoption increases demand for specialized assays.

- Turnaround and capacity: lab backlogs are an early warning for pricing pressure or margin erosion; measure regional TAT and backlog as leading indicators.

- Technological disruption: emerging rapid field assays and sensor-based calorific measurement can compress basic testing margins but create upsell opportunities for confirmatory lab work and certification.

How PW Consulting supports execution

The full Solid Fuel Testing Market report packages the data, models, and playbooks referenced here into a single delivery that includes the editable revenue model, scenario worksheets, procurement templates, and a confidential vendor capability appendix. For executive teams preparing 2026 budgets, the deliverables are designed to be directly actionable: they translate market signals into investment thresholds and go/no-go decision points.

We intentionally present a high-level public view in this release to protect sensitive sub-segment data and commercial assumptions contained in the complete study. Clients who require the detailed regional, fuel-type, and test-type splits, or bespoke scenario tailoring for corporate planning, are invited to access the full report and modeling toolset via PW Consulting’s research portal.

Next steps

- Download the executive briefing and request the full dataset and model for internal sensitivity analysis.

- Schedule a PW Consulting strategy session to align test-capacity investments and M&A priorities with your 2026 operating plan.

PW Consulting — bringing pragmatic market foresight and execution-ready guidance for organizations navigating the evolving solid fuel testing landscape in 2026.

For detailed analysis of this topic, please visit the official page:Solid Fuel Testing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com