Runway Lighting System Market Industry Analysis

Other |

2026-06-02 06:11:13

PW Consulting’s latest Wall Mount Electric Cabinet Market study (base year 2025; forecast period 2026–2032) delivers a focused strategic briefing for executives making capital, product and go‑to‑market decisions in the coming 12–24 months. At a global scale the market reached roughly USD 6.48 billion in 2025 and, under our central case, is expected to continue growing at a mid‑single‑digit compound annual growth rate (CAGR of 5.43%) through the 2026–2032 forecast window. This preview explains why those headline numbers matter, what pragmatic tools the full report contains, and which commercial moves we expect to separate winners from followers in 2026.

Wall Mount Electric Cabinet Market

Strategic capital allocation: The steady mid‑single‑digit expansion of the overall market masks diverging economics by product architecture, material choice, and end‑user demand profile. Boards and CFOs need scenario‑based valuations — not point estimates — to choose between capacity investments, product R&D, or M&A.

Wall Mount Electric Cabinet Market

Procurement and cost risk management: Input cost volatility and labor availability are already reshaping sourcing strategies. Manufacturers that move from spot buying to structured hedging and strategic supplier partnerships will secure margin advantage as 2026 procurement cycles are negotiated.

Wall Mount Electric Cabinet Market

Regulatory and sustainability compliance: IEC 62208 and new energy efficiency requirements in major markets are transforming product requirements (e.g., enclosure thermal management and ingress protection). Companies that lock compliance and certification roadmaps into new product timelines will accelerate market access and reduce time‑to‑revenue.

Service and software as differentiation: The winner’s playbook is shifting toward bundled offerings — hardware plus monitoring, edge compute readiness, and lifecycle services. Product roadmaps that include digital hooks (telemetry, environment sensing, predictive maintenance) are commanding higher margins.

Proven methodology and data assets: Detailed description of our top‑down and bottom‑up market sizing method, data sources, and confidence intervals — enabling clients to stress‑test the headline forecast against internal data.

Demand driver analysis: Sectoral and macro drivers (industrial automation, distributed energy, telecom densification, commercial retrofits) translated into demand scenarios and growth vectors for 2026 planning.

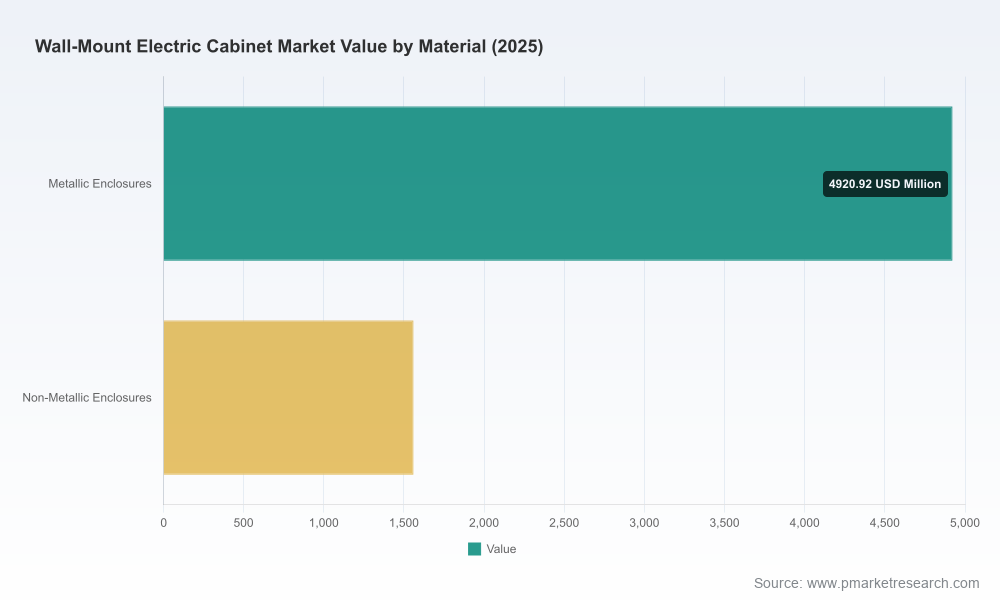

Segmentation framework (with guarded granularity): We map the market across material types, enclosure families, end‑use verticals and distribution channels, and we provide the decision frameworks investors need — while preserving the granular tables for report purchasers.

Pricing and total cost of ownership (TCO) models: Ready‑to‑use Excel models that quantify the impact of materials mix, finish level, certification requirements and lifecycle service revenue to evaluate margin trade‑offs per product family.

Supply chain stress‑tests and procurement levers: Scenario playbooks that model raw‑material fluctuations, labor constraints, and logistics disruptions and recommend supplier diversification, long‑term contracts and near‑shoring thresholds.

Competition and capability mapping: Comparative scorecards across engineering, certifications, modularity, digital integration and channel reach for the leading vendors and meaningful challengers.

M&A and partnership screens: A prioritized list of capability gaps and target archetypes (regional scale plays, specialty material players, IIoT/software enablers) aligned to buyer‑type and price expectations.

Implementation toolkits: 90‑day pilots, six‑month operational sprints and 18‑month transformation roadmaps tailored to manufacturers, distributors and system integrators.

The sector exhibits a moderate concentration: the top three global vendors account for roughly one‑third of market revenue, while the top five remain under half of total market value. That structure creates both scale advantages for global incumbents and open windows for focused specialists.

Schneider Electric — With its Spacial series and recent launches of EcoStruxure‑ready wall‑mount cabinets, Schneider is pushing the enclosure as a platform for edge compute and integrated telemetry. For market players, the strategic lesson is clear: IoT‑enabled hardware unlocks recurring revenue but requires early investment in integration APIs and cybersecurity validation.

ABB — ABB’s Mistral portfolio and recent certification wins for North America underscore certification as a competitive moat. Rapidly changing approval regimes mean product roadmaps must include parallel certification lanes to avoid bottlenecks when entering regulated markets.

Eaton — Eaton’s modular wall‑mount series shows how configurability can reduce lead times and improve aftermarket upsell. Manufacturers should evaluate platform architectures that enable custom BOM assembly without fragmenting manufacturing efficiency.

Rittal — Recent product refreshes highlight modularity and climate‑control integration. Rittal’s trade‑show cadence demonstrates the importance of continuous product marketing to support channel pull.

Hammond Manufacturing, nVent HOFFMAN, Legrand — These players illustrate contrasting strategies: cost leadership in standardized steel or polycarbonate enclosures, hazard‑rated niche certifications and low‑voltage distribution specialization, respectively. Each provides a template for competing without global scale.

Materials and production economics — expect continued pressure on fabrication margins unless manufacturers optimize material usage, invest in automation welding and powder‑coat efficiencies, or shift some demand toward engineered non‑metallic solutions where technically acceptable.

Certification timelines — markets with tightened energy and safety standards will create first‑mover advantages for certified enclosures and integrated cooling designs.

Productization of services — embedding sensors, analytics and remote management into cabinets will change purchase criteria and enable annuity revenue streams that justify higher upfront ASPs.

Channel consolidation and distribution economics — distributors will increasingly favor suppliers offering configurable, in‑stock SKUs combined with short lead‑time fulfillment and engineering support.

Prioritize certification as strategic capex: Allocate a dedicated budget line to accelerate IEC/UL certifications in parallel streams; missing certifications will cost more than the up‑front expense through delayed access to key projects.

Lock procurement through hybrid sourcing: Combine long‑term contracts for base metals with a secondary spot program for opportunistic purchases; couple this with supplier scorecarding to enforce quality and lead‑time SLAs.

Invest in modularity and configurable platforms: Design families that share common sub‑assemblies to capture higher mix without linear cost increases and to enable faster customization for verticals like telecom and renewables.

Rapidly pilot IoT‑enabled enclosures: Execute two customer pilots in 2026 that bundle environmental monitoring and remote diagnostics — use pilot learnings to craft service pricing and lock channel agreements.

Adopt a dual M&A lens: seek tuck‑ins that add technical IP or geographic reach for immediate route‑to‑market; concurrently maintain a watchlist of technology plays (edge compute, cooling) for transformative acquisitions.

Embed sustainability metrics into product decisions: Consumers and large buyers are filtering suppliers by lifecycle emissions and recyclability. Establish product carbon footprints to support public tenders and enterprise buyers.

90 days — Run a procurement stress test, set up a certification gap analysis, and launch a digital enclosure pilot with one strategic customer.

6 months — Roll out modular platform prototypes, negotiate multi‑year raw material agreements, and secure at least one key regional certification for a lead product family.

18 months — Scale assemblies into production, embed remote monitoring into a standard SKU, finalize at least one strategic M&A or partnership, and convert pilot economics into a commercial pricing model.

This preview outlines the structures and strategic moves that will define competitive advantage in 2026. The full PW Consulting Wall Mount Electric Cabinet Market report contains the granular segmentation tables, regional demand curves, supplier scorecards, downloadable TCO and pricing models, and transaction comparables necessary to implement the recommendations above. These detailed exhibits and the interactive Excel toolkit are available to licensed report purchasers and advisory clients.

Contact PW Consulting to arrange a briefing with our industry team, book a workshop to adapt the models to your business, or request an executive summary tailored to your company’s strategic questions. Our mandate is to convert market intelligence into executable advantage — and 2026 is the year to act.

For detailed analysis of this topic, please visit the official page:Wall Mount Electric Cabinet Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com