Welded Stainless Steel Tubing Market — Strategic Outlook for 2026 Decision‑Makers

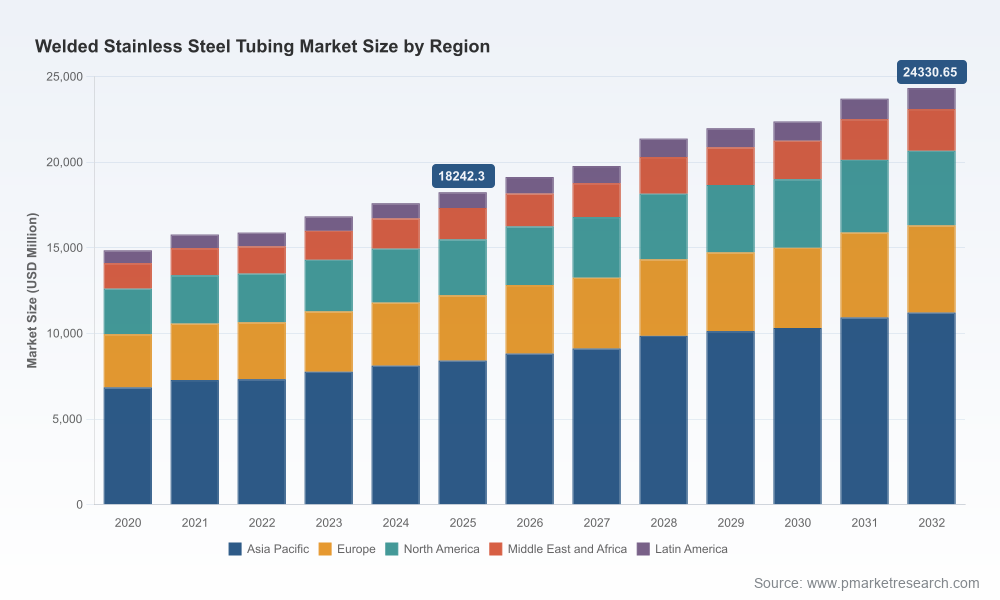

PW Consulting’s latest market study on Welded Stainless Steel Tubing provides a targeted intelligence package designed to sharpen executive choices in 2026. Anchored on a 2025 base year and a forecast horizon to 2032, the report synthesizes market sizing, supply‑chain dynamics, regulatory and standards evolution, and competitive positioning into a practical playbook for manufacturers, material buyers, OEMs, investors, and procurement teams. The headline: the global market is recovering into structurally higher demand, with revenue expanding from a base of approximately USD 18.24 billion in 2025 to a multi‑billion dollar market by 2032 at a compound annual growth rate (CAGR) of 4.2% across the 2026–2032 forecast window.

Welded Stainless Steel Tubing Market

Why this report matters for 2026 strategy

Two decisions dominate boardroom calendars in 2026: where to allocate capital in a mid‑cycle recovery and how to reduce margin volatility in the face of input cost swings and regulatory shifts. Our analysis converts those high‑level questions into executable options. The report blends a quantitative, model‑driven forecast with qualitative scenario mapping to answer the practical questions CEOs and procurement chiefs face this year:

Welded Stainless Steel Tubing Market

- Which product and process investments (e.g., laser welding, precision cold‑draw, specialty alloys) will deliver the highest incremental margin under plausible cost pathways?

- How material pricing volatility and feedstock supply constraints translate into gross‑margin and working‑capital stress across supplier tiers?

- Where are premium niches — heat exchangers, EV thermal systems, and high‑pressure oil & gas components — that sustain price‑over‑cost premiums?

Report contents — practical modules and tools

The study is structured for immediate use. Highlights include:

Welded Stainless Steel Tubing Market

- Top‑down market sizing and bottom‑up validation: a reconciled revenue model for 2020–2025 (historical) and a transparent forecasting engine for 2026–2032 that supports scenario toggles (volume, ASP, alloy mix and conversion rates).

- Cost‑to‑serve and margin decomposition: factory‑level schematics for welded versus seamless process lines, lift factors for laser and hybrid welding technologies, and sensitivity tables for nickel and chromium swings.

- Regulatory & standards impact assessment: clear implications of active ASTM standards on product qualification, project timelines, and specification changes that often drive premium pricing or exclude low‑cost suppliers.

- Technology adoption playbook: comparative assessment of conventional welding, laser‑welded technologies, and precision drawing. The report quantifies performance gains (including fatigue resistance improvements) and maps them to end‑market adoption timelines.

- Supply‑chain risk and supplier segmentation: supplier scoring templates, lead‑time heatmaps, and an actionable supplier hedging checklist for procurement teams to reduce single‑source exposure.

- Competitive landscape and M&A opportunity scanner: concise profiles and strategic posture for leading suppliers, investment triggers, and likely consolidation corridors.

- Commercial templates: tender question sets, technical evaluation rubrics, and a sample short‑list process for sourcing welded stainless tubing in capital projects.

Market dynamics that will shape 2026 plays

The market is being reshaped by three structural forces that matter for near‑term strategy:

- Raw material volatility: nickel and chromium feedstock prices have exhibited substantial swings in recent years, materially affecting unit economics and inventory carrying strategies. Procurement teams must balance shorter contract durations against price‑cap exposure.

- Standards tightening and new specifications: recent ASTM activity introduces clearer pathways for laser and laser‑hybrid welded structural tubing, which reduces buyer uncertainty but raises the bar for manufacturers seeking premium architectural and structural contracts.

- Technology migration into premium applications: laser‑welded tubing is emerging beyond niche architectural uses into critical fatigue‑sensitive applications — offering measurable durability benefits that some OEMs now require, especially in thermal management and emission control systems for vehicles.

Competitive landscape — what to watch

The welded stainless steel tubing sector remains fragmented: the aggregate share of the largest global players is limited, reflecting diverse specializations and a low top‑end concentration. This creates both opportunities and risks for new entrants and incumbents:

- Plymouth Tube Company (Warrenville, IL) — strength in precision and critical applications (aerospace, heat exchangers). Their emphasis on tight tolerances and custom grades positions them well for premium industrial demand.

- Tubacex (Llodio, Spain) — specialization in high‑performance alloys and service to oil & gas and power markets. Their alloy breadth is a barrier in corrosive and high‑temperature segments.

- Marcegaglia Steel (Mantova, Italy) — a broad European portfolio and scale across industrial and sanitary segments, useful in winning integrated supply contracts.

- ArcelorMittal (Luxembourg) and Nippon Steel Corporation (Tokyo) — large, integrated steelmakers whose scale and upstream integration provide cost levers and captive demand advantages in construction and automotive supply chains.

- Sandvik (Alleima) — focus on advanced precision tubes for medical and energy markets; technical differentiation is their competitive moat.

- Smaller, nimble US producers (KVA Stainless, Indiana Tube, Bristol Metals) — competitive on custom work, JIT service and proximity to regional OEMs. Laser‑weld specialists (Stainless Structurals) have begun to leverage standards compliance to capture structural and data‑center opportunities.

- European and Asian regional players (Fischer Group, YC Inox) — important local suppliers in specialized industrial chains and export channels.

Recent industry moves underscore these dynamics: laser‑weld capabilities are gaining market visibility through trade exhibitions and standard alignment, while heat‑exchanger demand continues to buoy premium tubing adoption. The market’s fragmentation — reflected in a modest three‑ and five‑firm concentration — signals room for strategic consolidation around technical capabilities and service models.

Practical strategic recommendations for 2026

Our guidance differentiates by role but centers on three actionable priorities:

- For manufacturers: accelerate selective capex into laser‑weld and hybrid‑weld lines for fatigue‑sensitive applications, paired with certification roadmaps to meet emerging ASTM structural specifications. Prioritize product platforms that command a margin premium through lifecycle cost advantages (e.g., duplex alloys for corrosive environments).

- For OEMs and specifiers: shift procurement to total‑cost‑of‑ownership frameworks that value fatigue life and corrosion resilience. Use our supplier scorecard and tender templates to move quality and delivery metrics to the center of negotiations rather than unit price alone.

- For investors and M&A teams: target bolt‑on acquisitions that add technical welding capabilities or shorten time‑to‑market for certified laser‑welded profiles. The market’s low top‑end concentration makes technical consolidation a compelling value‑creation pathway.

- For procurement leaders: enforce disciplined hedging and indexation clauses for nickel and chromium exposure, and adopt multi‑sourcing strategies for critical project pipelines to protect schedules.

How the report supports execution

This study is not a descriptive summary — it is a working toolkit. Subscribers receive the financial forecast model (Excel) with adjustable levers, a supplier evaluation kit, and bespoke scenario briefings tailored for capital and procurement committees. The numerical backbone — a reconciled market size of roughly USD 18.24 billion in 2025 growing at a 4.2% CAGR through 2032 to an estimated USD 24.33 billion — provides a discipline for investment prioritization and contract sizing.

What we intentionally omit here — and why

To preserve the utility of the full intelligence package, this announcement highlights strategic insight and rationale without reproducing the granular regional and application splits, price decks, or firm‑level revenue breakdowns that drive tactical sourcing and M&A decisions. Those segmented datasets, scenario matrices, and supplier financials are included in the full report and interactive model available from PW Consulting.

Next steps

For teams preparing 2026 budgets, running supplier rationalization exercises, or mapping M&A outreach lists, PW Consulting offers tailored briefings that deploy the report’s model against your specific project assumptions. Reach out to schedule a walk‑through of the forecast engine, supplier scorecards, and the scenario playbooks that convert insight into executable actions.

Our Welded Stainless Steel Tubing Market report combines market rigor, scenario discipline, and procurement pragmatism — the essential components for confident decision‑making in 2026.

For detailed analysis of this topic, please visit the official page:Welded Stainless Steel Tubing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com