Desiccated Coconut Market Insights: Rising Use in Bakery and Snack Applications

Other |

2026-06-03 12:00:23

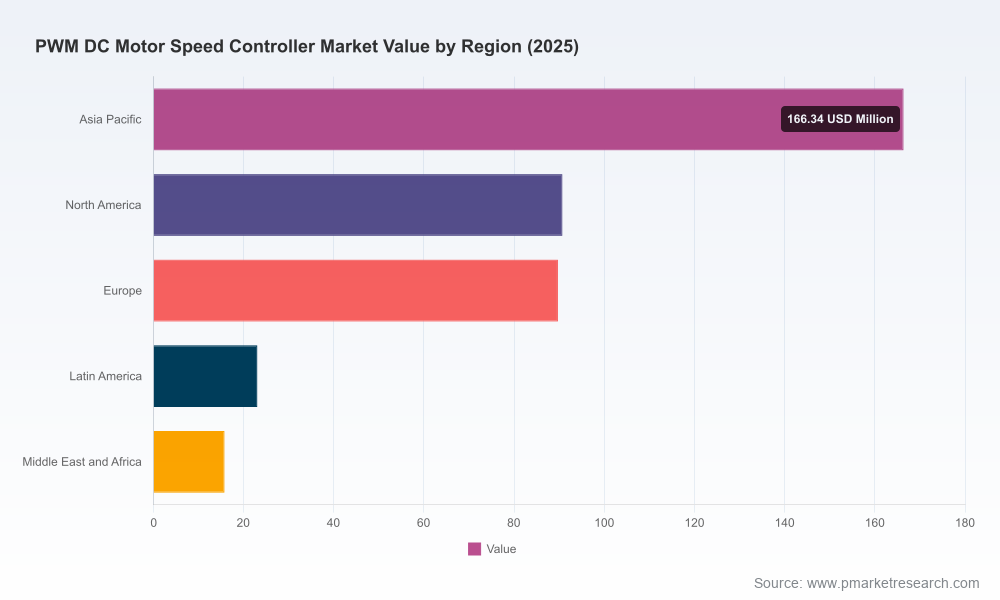

PW Consulting’s latest market research on the PWM DC motor speed controller market provides the strategic intelligence executives need to make high‑stakes product, sourcing, and M&A decisions in 2026. The study combines rigorous market accounting with practical playbooks and supplier benchmarking designed to be implemented within 12–18 months. The headline: after expanding from roughly USD 284 million in 2020 to USD 385.5 million in the base year (2025), the market is forecast to grow at a 6.42% CAGR through our forecast window, reaching an estimated ~USD 596 million by 2032. This trajectory underscores both steady demand and pockets of accelerated opportunity driven by electrification, automation, and miniaturization trends.

Pwm Dc Motor Speed Controller Market

Decision velocity: Hardware development cycles remain compressed. Our report translates market growth and component dynamics into concrete timing for product launches, qualification runs, and procurement commitments so teams can prioritize roadmap items that will capture near‑term revenue and limit time‑to‑market risk.

Pwm Dc Motor Speed Controller Market

Cost & supply clarity: With raw material and wafer price volatility increasing, procurement and design leaders need forward‑looking cost scenarios. We quantify sensitivity to silicon wafer and copper price moves and show how component mix choices change BOM volatility.

Pwm Dc Motor Speed Controller Market

Regulatory readiness: Standards and compliance are now differentiators. Our compliance matrix maps the practical implications of IEC and RoHS updates for controller design and supplier selection, reducing certification time and avoiding rework downstream.

Granular market accounting and validated forecast (base year 2025) with scenario models (base, downside supply shock, and accelerated adoption) that translate macro CAGR into addressable volumes and revenue lanes for product managers and CFOs.

Technology and product taxonomy that separates control topology (H‑bridge, dual H‑bridge, integrated MOSFET drivers), power classes, and control features (current sensing, regenerative braking, sensorless control) to guide architecture tradeoffs.

Supplier benchmarking and capability maps: objective scorecards that evaluate performance, pricing, roadmaps, and automotive/industrial qualifications to inform sourcing and partnership decisions.

Component cost‑builds and sensitivity analysis, including thermal margins, PCB layout implications, and mechanical packaging constraints for high‑power modules.

Regulatory & certification playbooks: step‑by‑step for IEC functional safety alignment and automotive grade qualification paths for teams targeting vehicle electrification programs.

Three executable growth playbooks (market entry for new OEMs, scale for established suppliers, and an M&A digest for PE and corporate development teams) with prioritized actions and typical ROI timelines.

The PWM DC motor controller ecosystem combines large semiconductor vendors, component specialists, and niche system suppliers. Market concentration is moderate: the top three vendors account for a meaningful share of industry revenue, while the top five capture a larger portion (CR3 ~31.5%, CR5 ~46.8%). This structure creates opportunities for both incumbents to extend platform control and for nimble specialists to win design‑wins in targeted segments.

Infineon Technologies AG — strength in power semiconductors and integrated motor control ICs; recent trade show activity reinforced its industrial focus and system‑level offerings.

STMicroelectronics — consistent innovation in low‑voltage PWM drivers; their recent low‑voltage driver launch signals intent to capture battery‑powered device segments.

Texas Instruments — broad family of DRV drivers with integrated features for high‑precision control; new high‑current dual H‑bridges expand options for motor OEMs.

Analog Devices — strong analog control and sensing IP, often chosen where precision and noise immunity are priorities.

onsemi, ROHM, Toshiba, NXP, Microchip — each brings differentiated value: onsemi for application‑specific high‑efficiency devices; ROHM and Toshiba for voltage/current envelopes; NXP and Microchip for MCU + driver system solutions and automotive qualification capabilities.

Pololu, Cytron, Dimension Engineering (Sabertooth) — represent modular, off‑the‑shelf controller options favored by rapid prototyping and certain industrial subsegments because of ease of integration and proven field reliability.

Recent vendor moves are instructive for 2026 planning: ST’s low‑voltage driver launch (Oct 2025) tightens competition in battery‑operated devices; TI’s high‑current DRV release (Sep 2025) broadens high‑performance options; Infineon’s MOTIX showcase (Electronica 2025) signals deeper system play; and NXP’s AEC‑Q100 certification updates (Apr 2025) lower the barrier to automotive adoption. For OEMs, these dynamics mean procurement teams must balance near‑term availability against long‑term feature roadmaps when locking design partners.

Raw material pressure: silicon wafer pricing for power MOSFETs rose materially, driving higher ASP risk for power stages. Our report models price pass‑through and suggests hedging thresholds for multi‑year supply agreements.

Copper for inductors and coils remains a cost driver. We include sensitivity tables that show how coil design choices affect BOM and thermal performance.

Regulatory constraints: updates to RoHS create rework risk for legacy manufacturing flows; we provide an action checklist to avoid CE mark delays.

Thermal management: for high‑power controllers (notably >100A designs), junction temperature limits make cooling architecture and MOSFET selection critical; our engineering checklists and thermal headroom calculators help avoid costly failures in qualification.

Lock flexible supply agreements for power MOSFETs and inductors with price reopener clauses tied to index benchmarks to mitigate short‑term wafer/copper shocks.

Prioritize designs that simplify certification (modular controller blocks with clear isolation and diagnostic layers) to shave months off time‑to‑market for industrial and automotive programs.

Invest in thermal management early: a marginally higher cold‑plate or PCB copper budget saves rework at qualification—and enables competitive high‑current SKUs.

Segment product roadmaps by control sophistication: low‑voltage, low‑cost controllers for battery devices; precision current‑sense controllers for robotics; high‑current regenerative controllers for industrial motion.

Use supplier scorecards from the report to run targeted RFIs; pair preferred semiconductor vendors with modular controller houses to speed integration.

For corporate development: target niche controller firms with strong design‑win pipelines rather than broad product catalogues to capture technology differentiation quickly.

Data pack and models: editable spreadsheets with forecast scenarios, BOM sensitivities, and supplier pricing inputs mapped to product lines.

Vendor scorecards and RFP templates: prebuilt tools to accelerate supplier selection and negotiation.

Technical playbooks: component selection guidelines, thermal design calculators, and certification timelines mapped to target geographies and end markets.

Workshops and sprint support: two‑day strategy sprints to translate findings into commercialization plans, and technical clinic sessions to de‑risk supplier integration.

This release is intentionally a strategic preview. It highlights market scale, growth trajectory, supply pressures, and the competitive moves shaping 2026 decisions, while reserving the detailed segmentation tables, proprietary vendor scoring, and deal‑level M&A targets for the full report and client portal. Executives who require the complete dataset—including downloadable models and the vendor benchmarking matrix—should contact PW Consulting to access the full PWM DC Motor Speed Controller Market report and secure advisory slots for implementation planning. In volatile markets, the right intelligence converts incremental margin pressure into strategic advantage—this report is designed to do exactly that.

For detailed analysis of this topic, please visit the official page:Pwm Dc Motor Speed Controller Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com