e-Clinical Solutions Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-02 11:50:23

PW Consulting’s latest industry brief on the Bone Cutting Forceps market synthesizes primary research, supplier diligence, regulatory mapping and scenario modelling to equip executive teams for decisive action in 2026. The report documents a steady historical expansion (from a mid‑hundreds USD million base in 2020 to USD 285.5 Million in 2025) and presents a rigorous forecast that anticipates continued expansion through 2032 at a compound annual growth rate of 5.85%. By 2032, our baseline projection puts the market size in the low‑to‑mid hundreds of millions of USD, reflecting durable demand driven by orthopedic and related surgical volumes, product longevity, and ongoing replacement/upgrade cycles.

Bone Cutting Forcep Market

Capital allocation: With a predictable mid‑single digit CAGR in the forecast window, manufacturers and investors can move from opportunistic spending to structured investment in capacity, precision manufacturing and aftermarket services.

Bone Cutting Forcep Market

Portfolio prioritization: Companies must balance premium, high‑durability offerings (e.g., titanium or treated alloys) against cost efficient stainless steel ranges, while preparing for regulatory scrutiny of reusable devices.

Bone Cutting Forcep Market

M&A timing: Consolidation signals are emerging; 2026 is a pivotal year to decide whether to pursue tuck‑ins that add service/refurb capabilities, broaden instrument portfolios, or acquire scale in distribution.

Our historical compilation shows steady recovery and growth after 2020, culminating in a 2025 market value of USD 285.5 Million. The forecast from 2026 through 2032 embeds demographic trends, surgical throughput assumptions, and technology adoption curves; it drives to a market size consistent with robust—but not hyperbolic—expansion by 2032. The implied growth path supports multi‑year strategic plans rather than short‑cycle speculation.

Market sizing and scenario modelling — including base, upside and downside cases for 2026–2032, with transparent assumptions and sensitivity tables to stress‑test strategies under different demand, pricing and regulatory scenarios.

Competitive heatmaps — a vendor matrix that scores manufacturers on product breadth, material competency, aftermarket services (repair/refurbish), distribution reach and quality certifications. Note: detailed segment shares and company revenues are reserved for the full report.

Regulatory & compliance playbook — a practical checklist mapping EU MDR, FDA pathways, and ISO 13485 expectations for reusable surgical instruments, plus sterilization validation considerations for autoclave‑rated devices.

Procurement and pricing playbook — benchmarking approaches, negotiation levers for OEMs and group purchasing organizations, and guidance on lifecycle cost analysis for hospitals prioritizing reusable instruments.

Manufacturing & supply‑chain diagnostics — audit templates for material sourcing (surgical‑grade stainless and high‑performance alloys), process controls for heat treatment and surface finishing, and CAPEX planning for precision machining and inspection.

M&A and partnership guide — target qualification criteria, integration risk checklists, and modelled accretion/dilution scenarios for deals involving product portfolios, service hubs or distribution networks.

Adoption & service models — go‑to‑market options for combining new instrument sales with refurbishment, warranty programs and sterile supply partnerships to increase recurring revenue.

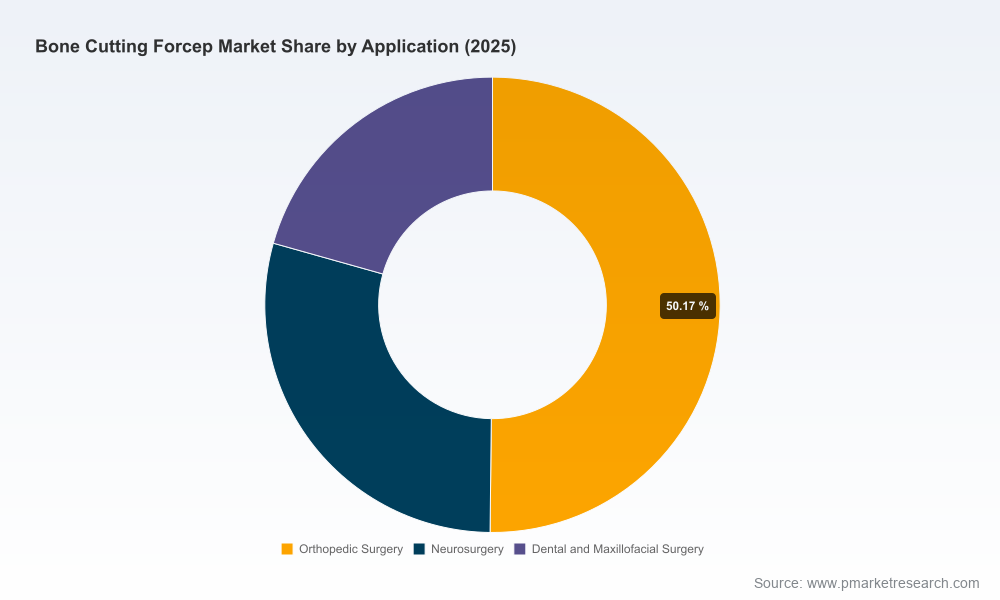

The Bone Cutting Forceps market remains modestly concentrated: top‑tier manufacturers occupy a meaningful but not dominant portion of market value, leaving room for specialists, aftermarket players and regional suppliers. Several patterns stand out:

Premium incumbents with strong mechanical design and service capabilities continue to defend margins by emphasizing durability, ease of sharpening/disassembly and clinician preference. An example is Stille AB (Torshälla, Sweden), a premium manufacturer known for precision double‑action designs and screw‑joint serviceability. In a strategic move that underscores consolidation dynamics, Stille AB acquired Surgical Holdings in September 2025 — an acquisition that expands its portfolio and adds repair/refurb capabilities to its offering.

Large device companies and hospital‑supply integrators carry broad instrument ranges and distribution scale. Integra LifeSciences (Miltex), based in Princeton, New Jersey, exemplifies this strategy with a wide catalogue that covers multiple clinical patterns and indications, supporting integrated procurement relationships with health systems.

Regional specialists and cost‑focused producers remain competitive by offering proven stainless‑steel instruments compliant with recognized standards. UK‑based Surgical Holdings (prior to acquisition) built credibility on BS‑compliant 420 stainless products and repair services; US suppliers such as gSource and GerMedUSA/GerVetUSA serve niche clinical and veterinary segments with focused portfolios and supply reliability.

Opportunities for aftermarket service consolidation are material: refurbishment, sharpening and certified repair present recurring margin streams and strengthen customer stickiness, particularly within orthopedic and podiatry pathways.

Device classification and compliance: Bone cutting forceps are subject to reusable medical device rules under major regulators. Manufacturers must design for repeated autoclaving and demonstrate compliance with quality systems such as ISO 13485. Regulatory readiness is a table‑stakes requirement for market access.

Material selection: High‑quality instruments are typically manufactured from surgical‑grade stainless steels (e.g., 420 or equivalent) or higher‑end alloys when performance and weight are differentiators. Material choice drives lifecycle costs, sterilization performance and clinician acceptance.

Certification: CE marking, ISO certifications and, where applicable, FDA clearances underpin customer procurement decisions. Demonstrable traceability and sterile‑processing validation increasingly matter to hospital supply chain teams.

Prioritize regulatory hygiene: For growth and M&A, ensure all product lines meet current reusable device standards and that technical documentation is audit‑ready. Post‑market surveillance processes should be operationalized to reduce recall and liability risk.

Build service‑oriented revenue: Expand certified repair/refurb options and extended warranty programs to monetize instrument longevity and increase lifetime customer value.

Segment product strategy: Maintain a two‑track portfolio—premium, differentiated instruments for specialty orthopedics and a cost‑effective baseline line for general surgery and high‑volume settings. Avoid a one‑size‑fits‑all approach.

Use M&A tactically: Targets that add service hubs, regional distribution or complementary instrument patterns offer faster payback than large platform deals. The 2025 consolidation activity illustrates this playbook.

Operationalize supplier risk management: Hardening supply chains for precision alloys and tight‑tolerance machining will reduce downtime risk and support premium positioning.

This briefing is an extract of a full PW Consulting market study designed for boards, strategy teams and corporate development functions. The full deliverable includes detailed modelling files, a vendor scorecard, an M&A target heatmap, and a procurement playbook that operational teams can apply immediately.

We intentionally present high‑confidence insights and actionable recommendations here while withholding segment‑level tables and proprietary company metrics that form the backbone of deal diligence and bid strategy. Organizations preparing capital budgets, M&A pipelines or product roadmaps for 2026 should obtain the full report to access the granular segmentation, regional demand analyses, pricing benchmarks and downloadable datasets that our clients use for execution.

Contact PW Consulting’s Life Sciences and Medical Devices practice to request the complete Bone Cutting Forceps Market report and accompanying data pack. Engage us for a short, confidential workshop to translate the findings into a 90‑day actionable plan for your business.

For detailed analysis of this topic, please visit the official page:Bone Cutting Forcep Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com