Egypt Artificial Intelligence Market Is Emerging as North Africa’s Digital Innovation Hub

Networking |

2026-05-26 08:24:55

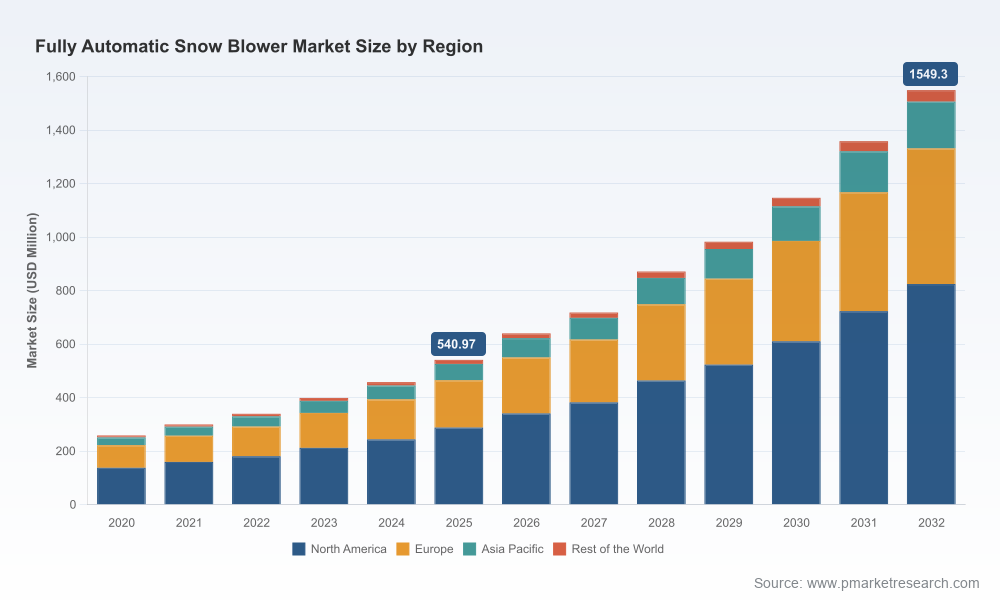

PW Consulting’s latest market research signals a rapid maturation of the fully automatic snow blower market. Our base-year assessment (2025) places the market at USD 540.97 Million, with the market expected to expand at a compounded annual growth rate (CAGR) of 16.22% across the 2026–2032 forecast window and to approach USD 1,549.3 Million by 2032. For executive teams, investors, and public-sector decision makers planning 2026 capital allocation and product roadmaps, this research functions as an operational playbook: it translates macro momentum into executable bets while preserving the granular models and proprietary segment data that drive investment decisions.

Fully Automatic Snow Blower Market

Timing: The step-change between 2025 and 2026 represents a tactical inflection for suppliers and channel partners. Early investments in validation pilots, field service networks, and customer financing can secure first-mover advantages as adoption accelerates.

Fully Automatic Snow Blower Market

Profit pool clarity: High-level concentration metrics show a market that is neither winner-take-all nor fully fragmented — the top three firms account for meaningful share while the top five consolidate a majority. This environment is favorable for targeted M&A, strategic partnerships, and white‑label supply arrangements.

Fully Automatic Snow Blower Market

Operational urgency: Structural headwinds in the labour pool and input-cost volatility are pushing snow management professionals toward automation faster than many broader hardware markets.

Labour substitution and reliability. Industry reporting indicates pronounced seasonal labour shortages — estimated to affect roughly 40–50% of snow removal contractors during peak winter months. The variable availability and increasing cost of seasonal workers are a primary adoption vector for autonomous and fully automatic equipment.

Technology readiness. Convergence of RTK-GPS, LiDAR, camera-based AI perception, and improved battery and powertrain options has closed key capability gaps. Field demonstrations in real snow and storm conditions are now proving reliability thresholds that were speculative three years ago.

Input-market context. Steel, a critical raw material for housings, augers, and frames, has shown moderated volatility with recent pricing benchmarks in Asia and stabilized U.S. short-ton pricing—factors procurement and manufacturing teams must integrate into cost models and hedging strategies.

Customer economics. For many commercial, municipal, and premium residential buyers, the decision calculus has shifted from simple unit cost to fleet availability, predictable operating expenses, and minimized overtime and liability exposure during severe storms.

Proprietary market-sizing models and growth scenarios: multiple demand trajectories (conservative, base, and accelerated) tied to macro adoption triggers and regional winter-event stress-tests.

Segment playbooks: go-to-market strategies by buyer type (residential premium, contractor fleet, municipal/airport deployments), including channel design, pricing architectures, and service-level expectations. Note: the full report contains the complete, model-backed segment allocations and unit economics used to prioritize go-to-market investments.

Technology & product roadmap analysis: maturity maps for navigation systems, perception stacks, human‑machine interfaces, and winterized powertrains along with vendor scorecards and recommended integration partners.

Commercial pilots & procurement templates: end-to-end pilot plans, acceptance criteria, KPIs for clearance rate and uptime, warranty templates, and SLA language tailored to high-liability municipal and airport contracts.

Unit-economics toolkits: total cost of ownership (TCO) calculators, payback sensitivity matrices, and pricing guidance for outright sale, rental, and subscription service models.

Supply-chain risk models: steel exposure analysis, recommended hedging strategies, dual-sourcing playbooks, and nearshoring considerations to reduce lead times in critical winter deployment windows.

M&A and partnership screening: criteria-based shortlists for bolt-on acquisitions (controls, perception, battery integration) and potential white-label agreements to accelerate market entry.

The competitive field is a mix of dedicated robotic innovators, traditional snow‑equipment incumbents, and industrial heavyweights. Market concentration metrics illustrate room for both scale and specialization: the top three players control a substantial share, while the top five capture more than half of the market — creating corridors for specialist entrants to win with focused use cases and for established OEMs to leverage brand and distribution.

Yarbo International Inc. — A clear innovator in the robotic yard market. Yarbo’s S1 fully automatic snow blower and modular M Series demonstrated in-market performance through high‑visibility live events and a viral storm‑response deployment. Their integration of RTK-GPS, AI vision, weather-triggered automation, and modular year-round attachments positions them as a leading pure-play vendor for residential automation and near-residential pilots. Their product showcases highlight 24/7 operation, auto-recharging, and cold‑temperature engineering that will shape buyer expectations for robotic reliability.

Ariens Company — A legacy manufacturer with deep expertise in durable, two-stage clearing units and professional-grade construction. Ariens’ strengths lie in build quality and channel trust; their strategic choice points are whether to invest in autonomous guidance retrofits, partner with perception stack providers, or remain focused on operator-guided premium equipment for professional users.

The Toro Company — Leverages extensive product engineering across turf care and battery platforms, and is well positioned to transfer autonomy lessons from related equipment to snow-clearing variants. Toro’s go-to-market advantage is strong dealer networks and a history of delivering user-oriented, battery-powered solutions at scale.

Husqvarna AB — Brings autonomy pedigree from robotic lawn care to winter-use considerations. Husqvarna’s strengths are global distribution and robotics R&D; the strategic question is how to winterize and scale their perception and navigation IP for heavy-snow environments.

Larue — A specialist in high-capacity, industrial and airport-grade clearing. Larue’s competitive moat is engineering for extreme, continuous-use scenarios; the opportunity is in marrying that reliability with semi-autonomous systems for large-mission applications.

For OEMs and product teams: accelerate field validation on critical winter scenarios now. Short, iterative pilots across multiple microclimates will yield the most actionable reliability data before the 2026–2027 selling season.

For investors and M&A teams: prioritize targets that fill gaps in perception, winter powertrain durability, or service networks. A small number of bolt-on acquisitions can materially compress time-to-market.

For channels and contractors: build hybrid service models combining human crews with autonomous units. This approach reduces peak staffing risk and enables new revenue through managed service offerings.

For municipalities and airports: adopt phased procurement that starts with pilot corridors and scales to fleet conversion linked to performance milestones and uptime guarantees.

For suppliers and contract manufacturers: secure raw material agreements and conditional replenishment strategies for winter-critical components; localized final assembly can be a de‑risking lever.

Raw-material volatility — mitigate with multi-year supply contracts, indexed hedges, and redesigns that reduce steel intensity where possible.

Operational reliability in extreme weather — prioritize sensor fusion, redundant navigation pathways (RTK + LiDAR + vision), and clear maintenance routines; embed these into warranty and SLA structures.

Liability and regulation — invest in certification processes and third-party testing; establish clear operator override and safe‑zone protocols for public deployments.

Buyer acceptance and cost sensitivity — design flexible commercial models (rental, subscription, outcome-based pricing) to lower adoption friction.

Cybersecurity and data privacy — harden connectivity stacks and define data ownership in procurement contracts.

The macro trajectory — from a base of roughly USD 541 Million in 2025 to a materially larger market beginning in 2026 — creates an accelerated runway for winners and second movers alike. Companies that prioritize operational pilots, invest in winterized autonomy engineering, and build outcome-based commercial models will capture disproportionate share as buyers shift from manual labor to automated, predictable snow-clearing solutions. Conversely, delay risks leaving strategic options limited to price competition or late-stage catch-up M&A.

This preview is designed to surface the strategic choices and operational playbooks teams must act on in 2026. PW Consulting’s full Fully Automatic Snow Blower Market report includes the detailed segmentation, proprietary scenario models, vendor scorecards, downloadable TCO and pilot KPIs, and a curated list of potential acquisition and partnership targets that underpin the recommendations summarized here. For organizations preparing budgets, pilots, or investment memoranda for 2026, access to the full dataset and executable templates will materially shorten decision cycles and reduce execution risk.

To obtain the complete report package, supporting dashboards, and bespoke consulting engagements tailored to your role (OEM, investor, municipality, or service provider), please consult PW Consulting’s market portal or contact your PW account team for immediate guidance and licensing options.

For detailed analysis of this topic, please visit the official page:Fully Automatic Snow Blower Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com