Composite Sandwich Panels Market: Strategic Imperatives for 2026 — PW Consulting Market Preview

Executive snapshot

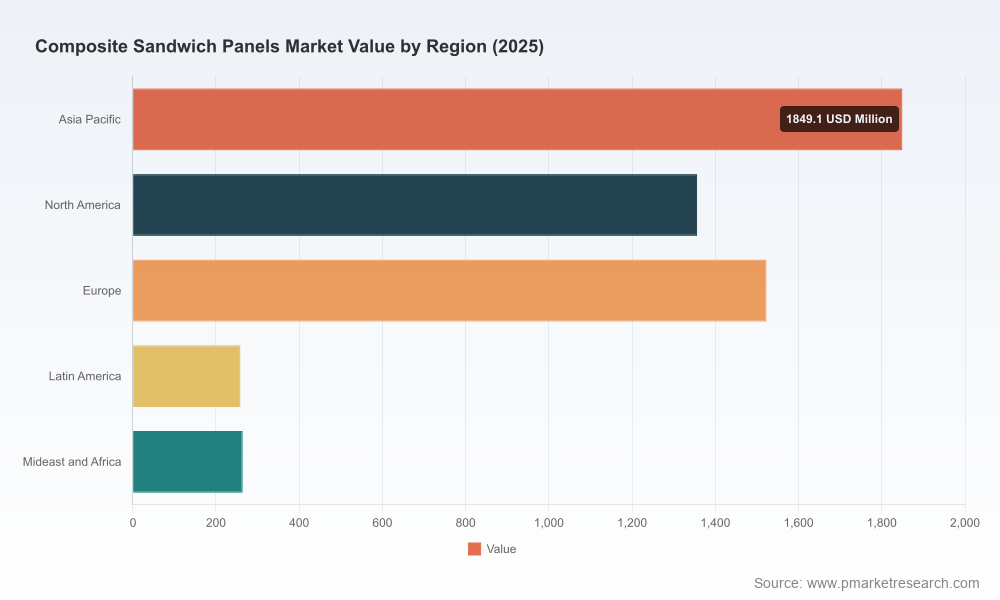

The composite sandwich panels market stands at an inflection point. According to PW Consulting’s latest market model, the industry reached approximately USD 5.25 billion (base year 2025) and is projected to expand at a compound annual growth rate (CAGR) of 7.15% through our forecast window, reaching just over USD 8.5 billion by 2032. This trajectory reflects a combination of regulatory acceleration around thermal and fire performance, renewed traction in transport and modular construction segments, and material-technology shifts that are remapping competitive advantage.

Composite Sandwich Panels Market

Why this report matters for 2026 decision-making

- Timing: 2026 is a make-or-break year for many commercial and capital decisions—capacity investments ordered now will begin contributing to supply only as demand profiles and compliance windows tighten.

- Actionability: PW Consulting’s Composite Sandwich Panels Market report converts market forecasts into operational priorities—procurement hedges, certification roadmaps, manufacturing contingencies, and go-to-market sequencing—for executives who must act this year.

- Signal vs. noise: The market is being shaped by a small set of structural forces (regulation, raw material volatility, and manufacturing innovation). Our analysis separates transient price swings from durable demand drivers to support robust capital allocation and M&A decisions.

Macro dynamics shaping the market

Three structural dynamics are driving the market’s growth profile and risk topology:

Composite Sandwich Panels Market

- Regulatory tightening and performance-driven specification. Stricter fire-safety and energy-efficiency codes are shifting specification toward advanced cores and facings that can demonstrate low embodied carbon, high thermal resistance, and fire performance without sacrificing weight. This is translating into demand for higher-performance sandwich constructions across building envelopes, cold storage, and transportation applications.

- Material and feedstock volatility. Core chemistries—polyurethane (PUR), polyisocyanurate (PIR), thermoplastics, and honeycomb structures—remain sensitive to feedstock cycles tied to global oil markets. At the same time, thermoplastic cores and recycled polyolefins are moving from niche to scale as buyers seek cost-stable, recyclable alternatives.

- Manufacturing innovation and certification. Out-of-autoclave thermoplastic systems, new honeycomb core grades, and mid-temperature stable cores are expanding applicability—particularly in aerospace and high-performance transport—while certifications and qualification programs are becoming gatekeepers to premium segments.

What’s in the PW Consulting report (practical takeaways)

Designed for boards, COOs, and strategy teams, the report goes well beyond forecasts. Key deliverables include:

Composite Sandwich Panels Market

- Detailed market sizing and scenario-based demand models spanning 2026–2032, with stress-tested outcomes for raw material price shocks and regulatory change.

- Input-cost pass-through templates and supplier-risk heat-maps to support procurement strategy and contractual design.

- Capex and capacity planning tools that translate demand scenarios into plant sizing, breakeven timelines, and utilization sensitivities.

- Competitive benchmarking and capability matrices (product technologies, certification status, geographic reach, and channel strength).

- M&A and partnership playbooks: target profiles, valuation heuristics, and integration checklists for bolt-on consolidation or vertical integration.

- Commercial playbooks tailored to construction, transportation, and aerospace buyers—pricing tactics, spec-education programs, and OEM engagement frameworks.

- Regulatory compliance and sustainability toolkits: LCA templates, fire-rating pathways, and product claims positioning to accelerate adoption in regulated markets.

Competitive landscape — reading the field

The market exhibits moderate concentration: the top three suppliers account for roughly one-third of industry revenues, and the top five approach mid-forties in share, leaving substantial share for specialists and regional champions. That mix creates simultaneous opportunities for scale players to consolidate and for agile niche providers to capture premium applications.

Selected strategic profiles and implications:

- Kingspan Group (Ireland) — Focused on high-performance insulated systems and advanced core innovations. Strategic emphasis on thermal efficiency and fire safety positions Kingspan to capture specification-driven opportunities in building envelopes and modular construction.

- Hexcel Corporation (United States) — A specialist in honeycomb cores and aerospace-grade sandwich solutions. Its product pipeline—targeting higher thermal and mechanical stability—illustrates how certification and material R&D unlock premium aerospace and defense margins.

- The Gill Corporation (United States) — A custom provider for aerospace and transportation, with press capabilities for multi-opening panels. Its strength is in tailored structural solutions where weight and dimensional tolerances command price premiums.

- ArcelorMittal (Luxembourg) — A metal-faced panel incumbent leveraging steel’s structural credentials for roofing and wall systems. The company’s moves show how traditional metals providers can defend share via productization and engineering services.

- Tata Steel (India), Assan Panel (Turkey), Nucor (US), DANA Group (UAE) — Regional heavyweights and system suppliers that combine manufacturing scale with local channel access; they are frequently the first choice for industrial and cold-storage builds in their home markets.

- Innovators and specialists (3A Composites, EconCore, Rock West, ACMFG, Hangzhou Holycore, Manni, Metecno) — These firms drive application-specific innovation: lightweight facings, thermoplastic cores, honeycomb cost-reduction, and rapid customization—areas where product differentiation is defensible.

Recent industry developments — what they signal

- Capacity expansions by regional producers are evidence of continuing demand from transportation and construction players—this increases short-term supply flexibility but also raises the bar for differentiation through performance and certification.

- New product introductions and material certifications demonstrate that material innovation—especially thermoplastics and mid-temperature stable honeycombs—is converging with the certification pathways that open aerospace and high-spec transport segments.

- Ongoing investments in production lines and continuous manufacturing suggest a move toward cost-efficient high-volume applications (e.g., 3D automotive parts, modular building), which will compress prices for commodity sandwich panels while enlarging premium niches.

Investment, M&A and partnership themes for 2026

Given the market structure and forecast growth, strategic capital in 2026 should pursue one or more of three archetypes:

- Scale consolidation: Acquiring complementary regional producers to secure channel access and spread fixed costs across larger volumes.

- Technology capture: Acquiring or partnering with innovators in honeycomb cores, thermoplastics, or out-of-autoclave systems to shortcut time-to-market for premium applications.

- Upstream integration: Securing feedstock (foam cores, thermoplastic resins) via joint ventures or long-term contracts to stabilize margins amid raw-material volatility.

Five pragmatic moves for executives in 2026

- Implement dynamic procurement contracts that combine indexed pricing with volume-flex clauses and alternative-feedstock triggers to limit margin erosion from oil-price shocks.

- Prioritize certification projects that unlock aerospace and transport premiums—assess NCAMP-like pathways and allocate development CAPEX accordingly.

- Pursue selective capacity investments in flexible lines geared for thermoplastic and honeycomb structures, enabling rapid product shifts as demand mixes evolve.

- Build sustainability narratives with quantified LCAs and recycled-content declarations—these are rapidly becoming procurement table stakes in key end markets.

- Create a competitive response map: identify which regional incumbents you must partner with, which niche innovators to acquire, and where to invest in go-to-market capabilities to defend or extend margins.

How PW Consulting’s report helps you execute

This market brief is a strategic preview. The full PW Consulting Composite Sandwich Panels Market report contains the granular datasets, model workbooks, supplier dossiers, and playbooks needed to operationalize the recommendations above. We deliberately present high-level strategic conclusions here to help you prioritize—our full package includes the detailed subsegment, regional, and application matrices that enable procurement tender design, plant-location analytics, and transaction due-diligence.

Next steps

For boards and executive teams planning capital allocation, procurement strategy, or M&A in 2026, the decision window is now. PW Consulting can provide an executive briefing, run a tailored scenario workshop using your cost and demand assumptions, and deliver the transactional support materials required to act quickly and with confidence.

Contact PW Consulting to schedule a briefing and gain access to the full report, interactive dashboards, and model templates that underpin these strategic recommendations.

For detailed analysis of this topic, please visit the official page:Composite Sandwich Panels Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com