Geographic Information System (GIS) Market Size, Share and Forecast by 2030

Other |

2026-05-11 10:54:46

PW Consulting’s latest Cpvc Power Pipe Market report provides a practical, decision‑oriented view for executives preparing 2026 strategies. Our analysis shows the market expanding from approximately USD 1,185.34 Million in 2020 to USD 1,648.55 Million in 2025, with a forecast trajectory to roughly USD 2,590.72 Million by 2032 — representing a compound annual growth rate of 6.67% across the 2026–2032 forecast window. These headline figures point to sustained demand and margin opportunity, but they mask important regional, application and supply‑chain nuances that will determine winners and losers in the coming 24–36 months.

Cpvc Power Pipe Market

Timing matters: capital allocation, supplier commitments, and greenfield/expansion choices made in 2026 will lock in cost structures and route‑to‑market advantages through a period of steady growth.

Cpvc Power Pipe Market

Risk is concentrated in inputs: CPVC economics remain tightly coupled to PVC feedstock, vinyl chloride monomer and chlorine availability — forces that can swing margins and redirect trade flows rapidly.

Cpvc Power Pipe Market

Regulatory and trade dynamics are changing the competitive map: production constraints and tariff movements are creating near‑term arbitrage and near‑permanent shifts in sourcing strategies for import‑dependent markets.

The market’s expansion to USD 1.65 billion by 2025 and the projected rise toward USD 2.59 billion by 2032 is driven by three structural themes. First, accelerated electrification and grid modernization programs are increasing demand for power‑grade conduit systems with predictable fire, thermal and long‑term reliability characteristics. Second, the densification of telecommunications and increased protection requirements for fiber and power cabling add a parallel consumption stream. Third, industrial modernization — particularly in power generation and process industries — is underpinning steady replacement and retrofit cycles.

These demand themes interact with supply dynamics (see below) to create differentiated pockets of margin and volatility. While headline growth is attractive, the most profitable positions will be taken by firms who combine product performance, compliant manufacturing footprints, and flexible supply strategies.

CPVC manufacturing remains input‑sensitive. In Q2 2025 analysts observed a quarter‑over‑quarter reprieve in some spot PVC/CPVC feedstock prices (a reported ~5.96% softening in North American spot prices), yet price levels remain material — US CPVC prices were reported at USD 2,370/MT in June 2025. At the same time, environmental audits and tighter regulatory enforcement in China and parts of Europe constrained output in 2025, reducing the availability of exportable volumes and putting pressure on import‑dependent regions.

Sharp tariff measures introduced in Q2 2025 further amplified regional price premia for CPVC and related feedstocks. The combined effect: producers with proximate resin integration or long‑dated resin contracts enjoy a considerable cost and delivery advantage, while downstream fabricators dependent on spot purchases face margin compression and service risk.

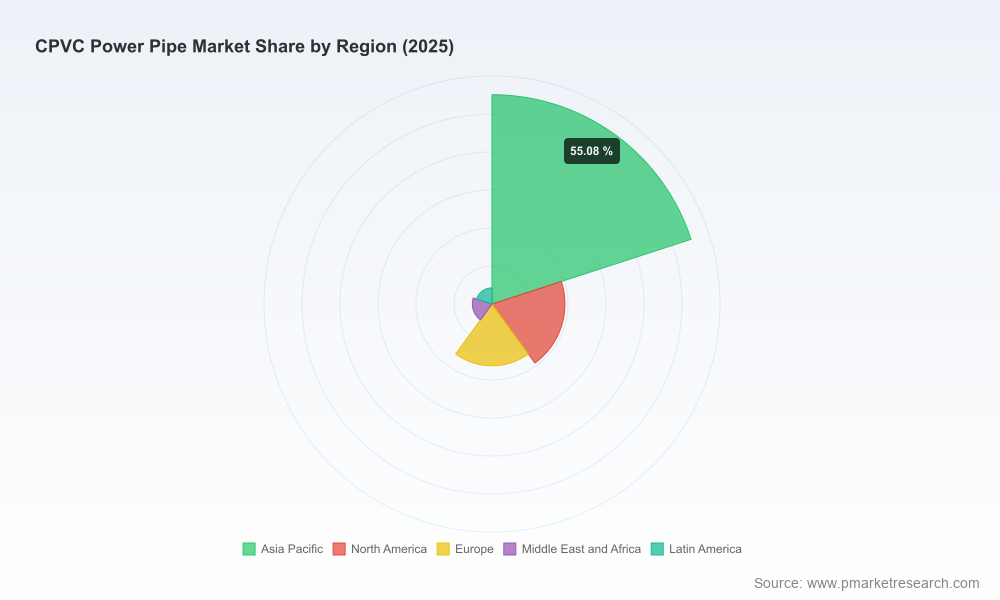

The Cpvc Power Pipe market is functionally fragmented. The three‑firm and five‑firm concentration metrics indicate a market where scale matters but does not dominate: top‑three firms account for roughly 21.45% of market share, while the top five control around 32.18%. That structure creates headroom for regional champions, technical innovators and players who can achieve cost parity with differentiated service or product features.

Key industry participants play distinct strategic roles:

Integrated resin suppliers and compounders (e.g., Lubrizol / Corzan) — control over resin and compound formulation delivers technical differentiation (heat resistance, flame performance) and creates strategic partnering leverage with downstream pipe manufacturers.

Large, standards‑focused fabricators (e.g., Charlotte Pipe, IPEX, Georg Fischer, NIBCO) — offer certified systems, scale manufacturing and established distribution in industrial and commercial channels, and are natural partners for utilities and specification‑driven projects.

Regional champions across APAC and South Asia (e.g., Astral, Supreme, Finolex, Prince, Ashirvad, China Lesso, Hebei Shentong) — excel at local market access, cost‑efficient production and regulatory familiarity; they are often first choice for large infrastructure programs within their home markets.

Given this landscape, strategic options for incumbents and new entrants include vertical integration with resin partners, product premiumization (e.g., certified high‑temperature/high‑voltage lines), and M&A to build scale in under‑penetrated regions.

Our report is designed as a playbook for executives rather than an academic compendium. It contains:

Market sizing and forecasting workbook (transparent methodology and sensitivity levers for 2026–2032).

Supply‑chain maps and resilience heatmaps (feedstock nodes, logistics chokepoints, lead‑time stress-tests).

Vendor scorecards and procurement playbooks (commercial terms, credit/risk profiles, alternative sourcing pathways).

Price‑curve modelling templates tied to PVC/VCM and chlorine inputs with scenario toggles for tariffs and regulatory closures.

Product strategy frameworks (how to prioritize high‑voltage, fire‑resistant and cable‑protection SKUs for margin capture).

M&A and partnership playbook (deal filters, integration checklists, cultural fit diagnostics and a shortlist of acquisition archetypes).

Execution roadmaps (90/180/365 day plans) for supply diversification, CAPEX decisions, and go‑to‑market adjustments.

Regulatory impact matrix and compliance checklist tuned to regions under audit pressure.

Prioritize feedstock security: negotiate multi‑year resin contracts or strategic supply alliances with compounders to mitigate spot volatility and secure technical exclusivity for specialized compounds.

Decentralize critical capacity: target production or tolling arrangements in import‑dependent regions to avoid tariff and audit‑driven supply shocks.

Segment product portfolios: differentiate between commoditized conduit lines and premium, certified high‑performance systems that command higher margins and preferential procurement by utilities.

Use scenario linking for capex: link plant expansion and tool investments to leading indicators (resin forward curves, regulatory audit frequency, tender pipelines) rather than static CAGR targets.

Pursue bolt‑on consolidation: with modest top‑five concentration, targeted M&A remains an efficient path to scale — focus on complementary geography or capability rather than large market share grabs.

Operationalize compliance: preempt regulatory scrutiny with third‑party environmental and quality audits, certification roadmaps and transparent traceability to reassure procurement teams in regulated markets.

Deploy dynamic pricing and inventory controls: combine digital demand forecasting with strategic safety stocks for critical SKUs to smooth earnings and preserve service.

Buyers (utilities, telcos, EPC firms) should price in delivery risk and prefer suppliers with integrated quality regimes and near‑market capacity. Suppliers should focus on product certification, cost position vs. local alternatives, and vertical partnerships with resin producers. Investors should evaluate targets on three vectors: feedstock security, regulatory resilience, and route to premium specifications — those factors explain valuation dispersion more than headline revenue growth.

The window for decisive action is immediate. 2026 procurement cycles, tender calendars and capital investment approvals will determine who secures long‑dated contracts and who must chase spot volumes under premium conditions. PW Consulting’s report combines the quantitative forecasts above with actionable tools and transaction support to translate the market’s momentum into durable competitive advantage.

This release is a strategic preview. To access the complete data tables, regional and application breakdowns, supplier benchmarking appendices and executable implementation modules referenced above, visit our report landing page. The full study includes the underlying models and vendor due‑diligence templates that procurement, strategy and M&A teams will use to operationalize 2026 plans.

For direct inquiries about enterprise licensing, custom scenario runs, or to commission a tailored supply‑chain stress test for your Cpvc Power Pipe portfolio, PW Consulting’s industry practice stands ready to assist.

For detailed analysis of this topic, please visit the official page:Cpvc Power Pipe Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com