El panorama de apuestas en España: Descubre las mejores casas de apuestas en línea

Other |

2026-05-13 20:26:22

PW Consulting today publishes an executive-level briefing drawn from our forthcoming Multi Loop Controller Market report, designed to inform executive decisions across procurement, operations, and corporate development in 2026. Built on a seven‑year historical baseline and a forward-looking model covering 2026–2032, the analysis illuminates where suppliers, end users, and investors should focus attention as the market evolves. At the macro level the market—valued at approximately USD 584.3 Million in our 2025 base year—is forecast to expand to the high‑seven‑hundreds by 2032, growing at a compound annual growth rate (CAGR) of 4.38% over the forecast period. This briefing summarizes the strategic takeaways; the comprehensive dataset, segment matrices, and actionable tools are available in the full report.

Multi Loop Controller Market

Alignment of CapEx and automation strategies: Manufacturers and process operators are balancing the economics of panel space, PLC load, and control fidelity. Our analysis translates market trends into procurement timing and replacement vs. retrofit thresholds for different asset classes.

Multi Loop Controller Market

Vendor consolidation and partner selection: With a moderately concentrated market structure—where the leading three and five firms capture a meaningful share—we map supplier capabilities to buyer requirements so procurement teams can shortlist partners aligned to integration, scale, and lifecycle support.

Multi Loop Controller Market

Risk management under supply uncertainty: The controllers’ dependency on semiconductors and specialized electronic components makes supply‑chain risk a first‑order consideration. The report embeds scenario modelling to stress test sourcing strategies and inventory policies against semiconductor market volatility.

Regulatory and quality compliance: Regulated industries face tighter expectations around process fidelity, auditability, and traceability. Our briefing shows how controller selection (features such as audit trails, AMS 2750F capability, and health‑index diagnostics) materially affects compliance costs and time‑to‑market.

The full report is structured as an operational playbook rather than an academic survey. Key deliverables include:

Market sizing and validated forecast model (2020–2032) with scenario toggles for upside/downside demand and component shortages.

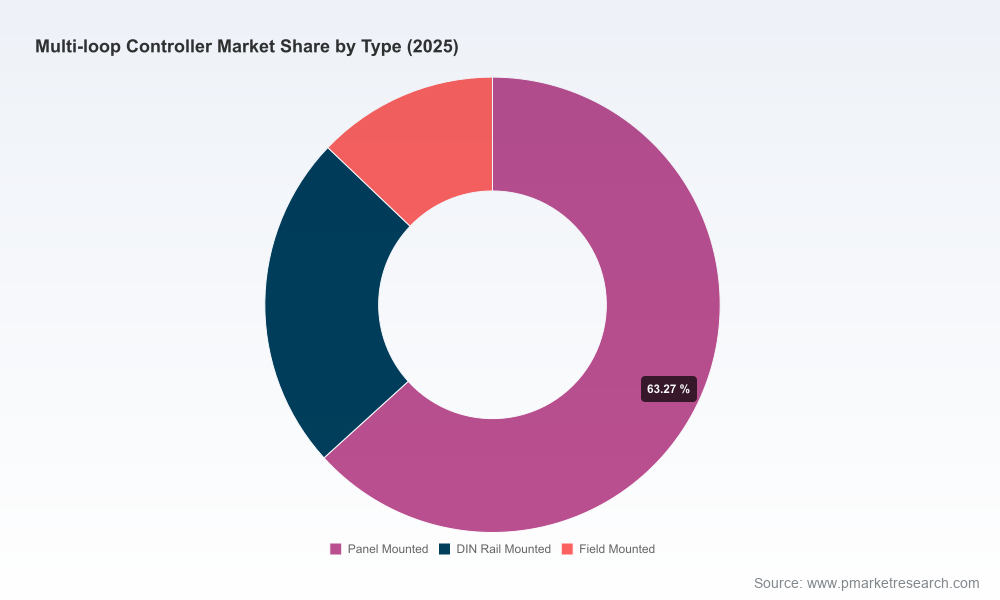

Technology and product taxonomy: panel, rail, and field architectures; communication stacks; and integration patterns with PLCs and MES.

Buyer persona maps and use‑case matrices that link application requirements (e.g., thermal zone density, regulatory data logging, cycle time, and uptime targets) to technical specifications and procurement checklists.

Supplier diligence toolkit: a standardized vendor scorecard, comparative capability heatmaps, and an M&A playbook for strategic buyers seeking inorganic growth or supply resilience.

Implementation blueprints and TCO models: payback calculators, retrofit decision trees, panel‑space optimization guidelines, and a staged rollout plan for digital enablement (edge telemetry, condition monitoring, security).

Operational annexes: commissioning checklists, validation templates for regulated environments, and a set of KPIs to monitor field performance post-deployment.

The vendor field blends global OEMs with specialist control houses. Our competitive analysis synthesizes product architecture, scale, compliance profile, software ecosystems, and channel reach to identify where each player adds differentiated value:

Watlow / Eurotherm — Strength in scalable, enterprise‑grade solutions. Watlow’s modular EZ‑ZONE architecture (noted for very high loop counts) and Eurotherm’s advanced multi‑loop controllers position them for projects where high‑density zone control and integration with broader thermal systems are priorities. Their combined offering targets large process lines that prioritize centralized control and service ecosystems.

Azbil Corporation — A strong play in precision and predictive maintenance. Azbil’s controllers emphasise accuracy, rapid sampling, and health‑index analytics, making them attractive to semiconductor fabs and other high‑precision industries that require embedded diagnostics for uptime assurance.

BrainChild Electronic — Niche strength in regulated and user‑centric interfaces. BrainChild’s offerings combine ergonomic touch interfaces, data‑logging with audit trails, and compliance to standards such as AMS 2750F and 21 CFR Part 11—attributes that resonate with aerospace, thermal processing, and pharma customers.

Fuji Electric, RKC, West Control Solutions (Gems Sensors group) — Broad portfolios covering modular rail and panel systems, with proven footprints in industrial OEMs and system integrators. These suppliers often compete on integration simplicity, local support, and proven uptime in heavy process environments.

Omega, Gefran, Athena Controls, Chromalox, Omron — These vendors provide complementary value propositions: ease of deployment for mid‑range installations, specialized industrial interfaces, and integration with automation ecosystems (PLCs, I/O, and HMI). Their products are commonly chosen where rapid deployment and compelling total cost of ownership matter most.

Collectively the market shows a moderate concentration: the top three firms capture a material share of revenue, and the top five firms extend that reach further. This creates a strategic window for mid‑tier challengers to carve niches via software differentiation, modularity, or regulatory compliance specialties.

Modularity and high‑loop scalability: Demand is accelerating for solutions that reduce panel footprint and PLC load by consolidating zones into scalable multi‑loop systems. This trend favors architectures that can scale incrementally and integrate with plant automation standards.

Regulatory and audit requirements: Products offering built‑in audit trails, validated data logging, and standards alignment (e.g., AMS 2750F, 21 CFR Part 11) are increasingly table stakes in regulated segments; vendors who bake compliance into firmware and reporting workflows gain procurement preference.

Predictive operational strategies: Health‑index and analytics capabilities are shifting purchasing conversations from pure capital procurement to operational reliability investments. Embedded diagnostics reduce maintenance churn and extend asset life, affecting vendor selection and service contracts.

Supply‑chain sensitivity: Semiconductor tightness and electronic component variability mean buyers need multi‑sourced strategies, longer lead‑time planning, and options for backwards‑compatible upgrades to limit downtime exposure.

Adopt a supplier segmentation approach: Classify suppliers into strategic, tactical, and contingency tiers. Reserve strategic RFPs for vendors that demonstrate lifecycle support, software‑driven analytics, and compliance credentials.

Standardize on modular platforms where possible: Prioritize controllers that allow incremental expansion and standard communication protocols to minimize PLC rework and reduce engineering hours for future changeovers.

Build compliance and data‑integrity checks into procurement specs: For regulated lines, require audit‑trail proof points, validation test cases, and a roadmap for firmware updates and long‑term data exportability.

Run supply‑shock war games: Use the report’s scenario models to stress test inventory policies and procurement cadence under component shortage and demand surge scenarios.

Invest in proof‑of‑concepts for analytics: Pilot health‑index or condition monitoring integrations on a representative asset cluster to quantify uptime gains and refine the business case for broader rollouts.

This briefing is a curated preview designed to accelerate high‑quality strategic conversations in 2026. The full PW Consulting Multi Loop Controller Market report delivers the comprehensive dataset (historical series and granular forecasts for 2026–2032), detailed supplier scorecards, downloadable TCO models, and executable implementation templates. For procurement teams, OEs, and private capital investors preparing 2026 investment or sourcing decisions, the full report is the working document to convert market insight into operational outcomes.

To obtain the complete report, proprietary datasets, and the vendor diligence toolkit, please visit PW Consulting’s market research portal or contact our industry team to schedule a briefing and tailored workshop.

For detailed analysis of this topic, please visit the official page:Multi Loop Controller Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com