Snacks Bars Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-19 12:56:41

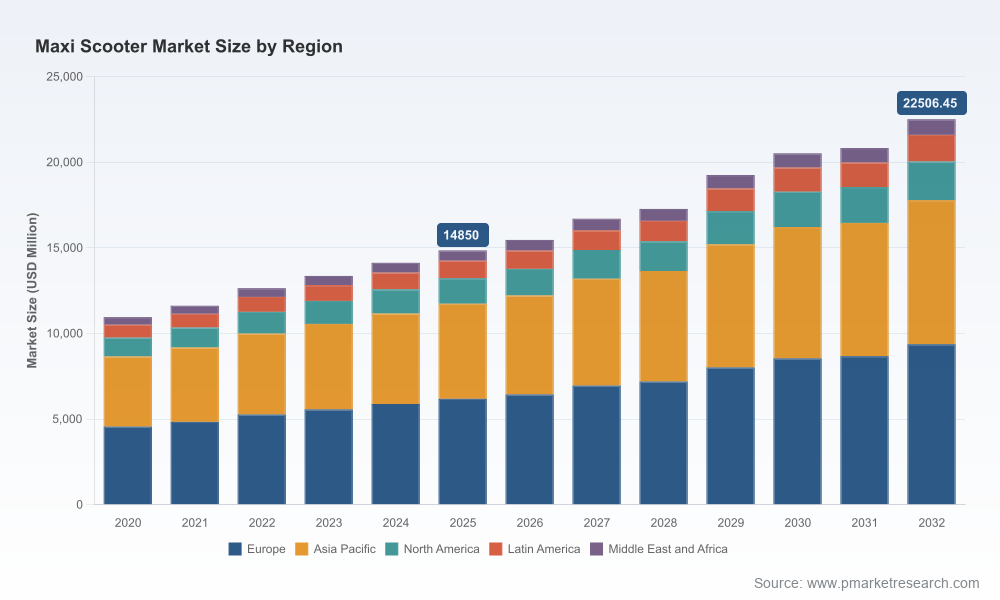

PW Consulting’s new Maxi Scooter Market report—anchored on a 2025 base year and a 2026–2032 forecast horizon—translates quantitative momentum into a strategic playbook for executives who must decide where to invest, partner, and pivot in 2026. The market is no longer a narrow niche: total industry revenues have expanded significantly over the past half-decade, moving from roughly USD 10.9 billion in 2020 to approximately USD 14.85 billion in 2025, and are forecast to grow at a compound annual growth rate (CAGR) of about 6.12% through 2032, reaching a materially larger market by the end of the period. This briefing highlights the levers that will matter to OEMs, suppliers, distributors and investors—while preserving the report’s proprietary segment-level detail to encourage direct download of the full study.

Maxi Scooter Market

Timing matters: 2026 is a pivot year. Policy tightening, product refresh cycles and a wave of new electric and high-displacement launches converge to create a compressed decision window for platform investments and channel expansion.

Maxi Scooter Market

Capital allocation clarity: the report quantifies the trade-offs between electrification investments and continued optimisation of internal-combustion maxi platforms—enabling CFOs to model capex scenarios against market growth and regulatory tailwinds.

Maxi Scooter Market

Partnerships as force multipliers: strategic alliances—especially around electric architectures and market-entry distribution—are now a primary route to scale. Our analysis identifies the partnership archetypes that deliver speed to market and margin protection.

The macro trajectory is robust and predictable enough to underpin multi-year investments. After steady expansion through 2025, the market’s forecast CAGR of ~6.12% implies a materially larger addressable pool by 2032. That pace accommodates both broad-based growth in premium touring and sport maxi scooters and accelerated adoption of electrified variants in regulatory-tight jurisdictions. Importantly, the market exhibits moderate concentration: the largest three players control a meaningful share but do not constitute a closed oligopoly, and the five-largest cohort leaves ample room for challengers and new entrants to displace value through innovation or selective geographic focus.

Our competitive review synthesises public product lines, positioning strategies and near-term initiatives for the sector’s core participants. Key strategic observations include:

Legacy OEMs are leveraging brand strength and tried-and-tested touring platforms to defend high-margin segments. Established European and Japanese players continue to emphasise premium build, electronics and comfort as differentiators.

Japanese manufacturers are pairing refined engines and transmission innovations (including DCT options) with aggressive geographic expansion in premium segments—targeting both mature and high-growth emerging markets.

Taiwanese OEMs are executing a dual strategy of advanced ICE touring models and partnerships to accelerate their electrified roadmap, using competitive pricing and proven long-range platforms to enter larger markets.

European niche manufacturers concentrate on distinctive multi-wheel and premium urban GT propositions, betting on styling and stability features to command premium pricing in congested urban corridors.

Newer entrants and China-origin brands are attacking the value end and selectively moving upmarket by incorporating modern electronics and adventure styling to capture aspirational buyers at lower price points.

Notable recent developments underscore these dynamics. Strategic collaborations to accelerate electrification and platform sharing have intensified, including a high-profile partnership aimed at launching a premium electric maxi-scooter in 2026; OEM product refreshes and targeted market entries (including US and India premium segments) further signal an aggressive competitive cadence into 2026.

Electrification is complex, not binary. While electric maxi scooters are gaining visibility—driven by low-emission zones and incentive programs—internal-combustion platforms remain commercially significant through 2026, particularly for long-distance touring customers and markets where charging infrastructure is nascent.

Safety and electronics are non-negotiables. Regulatory baselines (for example, mandatory ABS for vehicles above a certain displacement in key markets) are driving the adoption of more advanced braking and stability systems across product lines. These features increase engineering weight and bill-of-materials complexity but are essential for market access.

Emissions and powertrain engineering: tightening pollutant limits push suppliers and OEMs to adopt higher-pressure fuel systems and more sophisticated aftertreatment strategies; these technical requirements are reshaping powertrain roadmaps and supplier relationships.

Vehicle architecture trade-offs: improvements in suspension travel and ride stability—typical travel ranges have become more ambitious—plus safety modules add incremental mass and cost. Successful platforms balance these trade-offs without compromising ride dynamics or fuel/electric range.

Product & Engineering: Prioritise modular architectures that permit both ICE and electric drivetrains to share key subframes and electronics suites. This reduces time-to-market for electrified variants while preserving ICE revenue during the transition.

Supply Chain & Sourcing: Secure long‑lead BOM items such as advanced ABS modules and battery cells (for electrified variants) through flexible agreements. Component weight and thermal management considerations should be modelled into all new platforms.

Commercial & GTM: Territory prioritisation must account for regulatory stringency and charging infrastructure. Channel strategies that combine dedicated experiences for premium buyers with scalable aftersales networks will deliver higher lifecycle value.

M&A & Partnerships: Look for bolt-on acquisitions that fill capability gaps—battery management, power electronics, or telematics—or local distribution partners that accelerate market entry with acceptable payback profiles.

Within 90 days: complete a scenario-based portfolio stress test that models electrified versus ICE returns under three regulatory scenarios. Use our Monte Carlo templates included in the full report to quantify upside and downside.

Within 180 days: identify two strategic partnerships—one technical (battery or motor supplier) and one commercial (local distributor or ride-hailing partner)—that shorten time-to-market for a flagship model.

Within 12 months: commit to a production architecture that preserves a modular electronics backbone to support OTA updates, ADAS compatibility and multi-powertrain integration.

Organisation: create a cross-functional electrification steering committee with P&L accountability and clear KPI cadence tied to market rollout milestones.

Concise executive dashboards with scenario modelling templates for 2026–2032 that executives can use to stress-test investment cases.

Go-to-market frameworks that map product, price and channel options to regulatory and infrastructure scenarios in priority markets.

Supplier and component risk matrices—highlighting long‑lead items, critical weight/mass drivers and engineering complexity hotspots that influence platform economics.

Competitive positioning maps and playbooks: comparative strengths, white-space opportunities and actionable countermeasures tailored to OEM size and ambition.

M&A screening criteria and a short-list of target archetypes for capability acceleration, including integration risk checklists.

Senior leaders should treat the report as an operational blueprint rather than a purely academic forecast. Use the macro topline—market size and 6.12% CAGR—as the funding boundary within which to prioritise projects. Then apply the tactical tools (scenario templates, supplier matrices, and partnership archetypes) to convert those priorities into executable milestones for 2026. Importantly, the analysis purposely abstracts and aggregates segment-level data in this release to preserve the report’s proprietary, downloadable models that you will need to run to tailor decisions to your organisation.

The maxi scooter market in 2026 will reward clarity of strategy, speed of execution and partnerships that reduce technological and market-entry risk. PW Consulting’s report provides the analytical backbone and practical toolset to move from strategic intent to measurable results—whether that means defending a leadership position, scaling a regional entry, or pivoting to electrification. For executive teams planning 2026 budgets and board-level investment approvals, the report converts market momentum into a defensible path forward.

For full segmentation, detailed competitive benchmarking, and the tactical templates referenced above, access the complete Maxi Scooter Market report on our website. The downloadable models and annexes contain the segment-level detail necessary to operationalise the strategies outlined here.

For detailed analysis of this topic, please visit the official page:Maxi Scooter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com