Integrated Optical Delay Line Market — Strategic Outlook for 2026

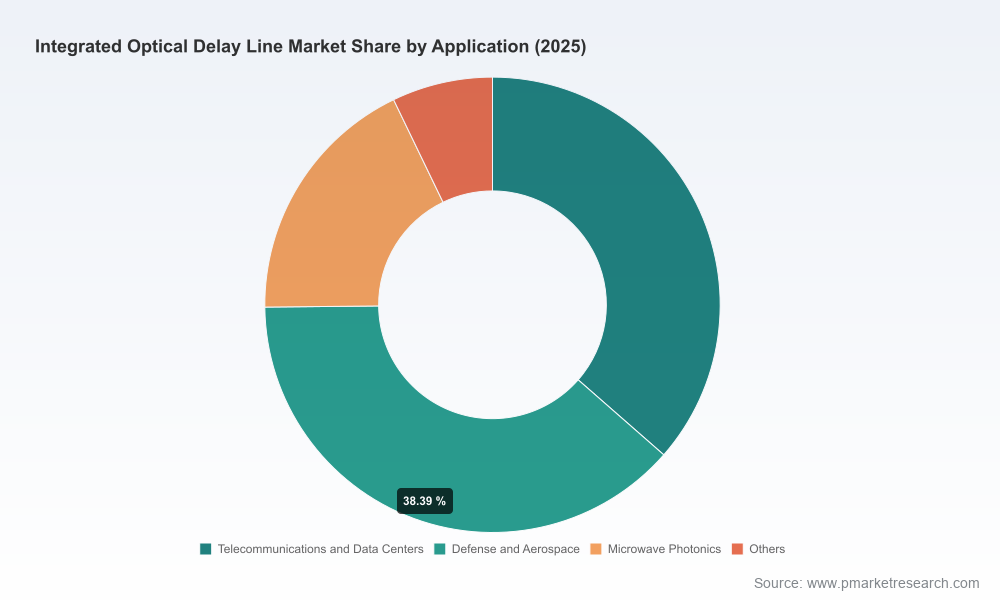

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present a high‑level brief of our Integrated Optical Delay Line (IODL) market study — the evidence base intended to inform executive decisions in 2026. Built on a 2025 base year and a seven‑and‑a‑half percent (7.5%) compound annual growth rate projection, the global market expands from a mid‑hundreds million USD scale in 2025 toward a high‑hundreds million USD opportunity by 2032. This briefing synthesizes the strategic implications we derive from our analysis while deliberately excluding detailed segment tables and granular regional / application breakouts — readers seeking the full datasets and model can access the source report.

Integrated Optical Delay Line Market

Why this market matters for 2026 decision cycles

IODLs are moving from laboratory curiosities and niche fiber solutions into practical building blocks for next‑generation telecom, sensing, microwave photonics and emerging quantum transduction systems. For 2026 planning horizons, three structural dynamics make integrated delay lines a strategic priority:

Integrated Optical Delay Line Market

- Structural growth with predictability — the market demonstrates steady expansion driven by converging demand vectors (telecom/datacom, LiDAR/sensing, microwave photonics and defense applications). Our base/forecast model (2020–2025 historical, 2026–2032 forecast) and scenario sensitivity analyses show resilient upside under conservative adoption curves.

- Technology differentiation creates moat opportunities — material platforms (silicon photonics, lithium niobate, fiber‑integrated approaches and specialty hybrid platforms) and foundry process choices (MPW vs dedicated runs) materially affect device performance, footprint and cost. Competing on waveguide loss, thermal management, and delay density separates winners from commodity suppliers.

- Policy and supply‑chain constraints are binders, not afterthoughts — standards on loss and thermal stability, plus export controls for dual‑use precision delay devices, mean early compliance and policy‑aware product design are competitive necessities.

Market trajectory and interpretive lens

Our topline model shows a clear, sustained upward trajectory across the 2026–2032 forecast window. For strategy teams this implies a deliberate, phased approach: accelerate prototyping and qualification for high‑value use cases this year; scale manufacturing partnerships and customer pilots in 2026–2027; and prepare margin capture and broader commercialization plays into the late‑decade inflection. The 7.5% CAGR embedding in the model is robust enough to underwrite capital allocation for process development and integration efforts, yet not so rapid as to obviate careful go‑to‑market sequencing.

Integrated Optical Delay Line Market

What the PW Consulting report contains (practical, decision‑ready elements)

- Market sizing and forecasts: top‑down and bottom‑up models spanning 2020–2032 (base year 2025), with scenario and sensitivity variants to stress test demand under alternative technology adoption and regulatory outcomes.

- Technology deep dives: comparative performance matrices for silicon photonics, lithium niobate, fiber‑integrated and hybrid platforms; key performance levers (delay density, insertion loss, thermal coefficient, footprint and power consumption); and manufacturing pathway analyses (MPW versus dedicated runs, packaging and testing bottlenecks).

- Supply‑chain & foundry mapping: critical supplier maps, lead‑time risk heatmaps, and a pragmatic partner prioritization framework for MEMS, wafer foundries and assembly houses.

- Competitive landscaping and capability benchmarking: profiles of incumbents and specialists, patent and research intelligence, go‑to‑market strengths and white‑space opportunities.

- Use‑case prioritization and commercial playbooks: ROI and commercialization timelines for telecom/datacenter latency management, FMCW LiDAR, phased‑array true‑time delay, microwave photonics, and quantum/microwave transduction applications.

- Regulatory and export control assessment: practical checklists and mitigation roadmaps for dual‑use export constraints and standards compliance (including IEEE guidance on photonic device performance).

- Investment & M&A guidance: criteria for bolt‑on acquisitions, licensing strategies, and JV formation with foundries or IP holders to accelerate time‑to‑market.

Competitive landscape — what to watch in 2026

IODL competition today is a mix of specialist component houses, research‑led corporate R&D, and systems integrators. Market concentration is moderate—our concentration analysis indicates that the top three players account for less than half of industry revenue, with the top five capturing under two‑thirds—leaving room for both niche innovators and consolidation plays.

- Enablence Technologies (Ottawa): a leader in planar lightwave circuit (PLC) implementations that deliver ultra‑long integrated delays in compact footprints. Their recent partnership activity to supply PLC chips into FMCW LiDAR supply chains signals an aggressive push into automotive and robotics ecosystems where size, robustness and integration matter.

- IBM (Armonk): research and patent strength around electro‑optic transducers and integrated delay architectures positions IBM as a pivotal IP holder for microwave‑to‑optical quantum transduction efforts. The 2025 patent grant for an electro‑optic transducer incorporating delay lines reinforces their strategic posture in quantum interface technologies.

- Microwave Photonic Systems (MPS): specialized in high‑performance photonic delay line systems targeted at RF and radar applications, MPS exemplifies the systems‑level integration play—packaging, thermal control and bandwidth management are their competitive advantages.

- Agiltron: a pragmatic vendor strategy focused on fully integrated modules and variable photonic time delay systems, often bundled with GUI and control layers — appealing to OEMs seeking short integration cycles.

- G&H (Gooch & Housego): long experience in custom fiber optic assemblies and small‑form‑factor variable delays makes them an attractive partner for avionics and defense primes needing tailored solutions.

Recent industry moves to monitor in 2026 include partner ecosystems (component to OEM linkages), patenting trends around transduction and delay‑density techniques, and academic breakthroughs that lower the trade‑off between delay length and footprint. Notably, research demonstrating multimode silicon photonic delay lines that push delay‑density limits has the potential to alter cost and performance dynamics for on‑chip true‑time delay implementations.

Key risks and mitigations for 2026 planners

- Standards and performance compliance: IEEE‑level emphasis on low‑loss waveguide performance and thermal stability makes early standards alignment essential. Mitigation: embed compliance testing in pilot contracts and select foundry processes with certified performance.

- Export controls and dual‑use classification: precise delay devices used in radar and quantum systems draw regulatory scrutiny. Mitigation: build export compliance into contractual frameworks; pursue controlled technology transfer pathways and work with legal/regulatory counsel early.

- Foundry capacity & process risk: while MPW runs accelerate prototyping, scale may require dedicated investments. Mitigation: tiered manufacturing strategy—use MPW for design validation, then secure priority slots or strategic partnerships for scale runs.

- Market adoption pacing: many IODL applications remain in research‑to‑early commercialization phases, particularly for on‑chip phased arrays. Mitigation: stage investment to productize for high‑value and early‑adopter verticals (defense, LiDAR, specialized telecom use cases) while monitoring volume signals.

Actionable recommendations for 2026

- Prioritize supplier and foundry engagements now. Locking in fabrication and packaging pathways reduces time‑to‑market risk for 2026 pilots and 2027 production ramps.

- Build an IP and standards roadmap. Where possible, secure freedom‑to‑operate via licensing or targeted patent filings in electro‑optic transduction and multimode delay architectures.

- Adopt a hybrid go‑to‑market approach. Combine focused vertical plays (defense/RF and LiDAR) with broader telecom/datacenter pilots to balance margin and volume exposure.

- Integrate compliance and export control into product development. Export classification and standards adherence should be part of product requirement specs rather than downstream tasks.

- Use modular product design to de‑risk integration. Standardized interfaces and control stacks accelerate OEM adoption and reduce customization cycles.

Closing — the strategic value of accessing the full report

PWC’s Integrated Optical Delay Line Market study is constructed to support capital allocation, R&D prioritization and commercial strategy for 2026 and beyond. The briefing above highlights the critical strategic considerations and the competitive landscape that executives must navigate. For teams preparing procurements, M&A diligences, or product roadmaps this year, the full report provides the underlying datasets, scenario models, granular segmentation and supplier scorecards that are deliberately omitted here to preserve investigative value and client exclusivity.

Contact PW Consulting to obtain the full report, the financial model (USD, revenue in Million units), and our custom advisory packages that translate findings into executable 12‑ and 36‑month plans tailored to your business objectives.

For detailed analysis of this topic, please visit the official page:Integrated Optical Delay Line Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com