Middle East and Africa Restaurant POS Software Market Trends, Challenges, and Forecast 2025 –2032

Home |

2026-06-22 04:48:14

By PW Consulting — Senior Strategic Advisor & Chief Industry Analyst

Fixed Drone Hangar Market

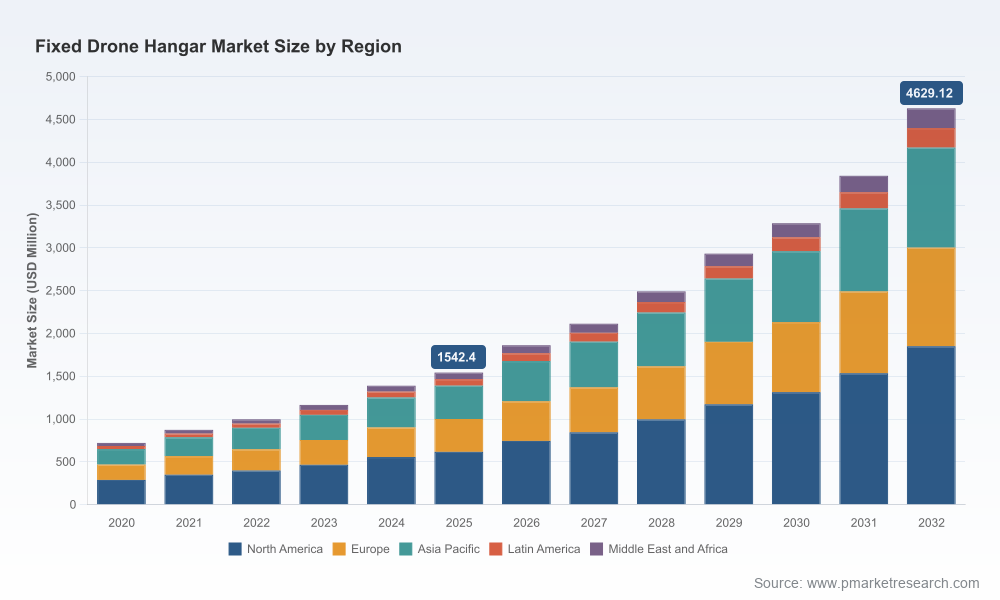

Our new market study on Fixed Drone Hangars positions this emerging infrastructure segment as one of the fastest-growing enablers of industrial unmanned aerial systems (UAS). Anchored on five years of historical analysis (2020–2025) with 2025 as the base year, the research forecasts the sector across 2026–2032 and quantifies a robust compound annual growth rate (CAGR) of 17.0% through the forecast interval. Measured in USD (Million), the market expands from a mid‑teens‑hundreds million baseline in 2025 to multiple billions by the early 2030s — a scale and velocity that will materially impact capital allocation, operational planning, and regulatory engagement for organisations investing in BVLOS-capable fixed installations.

Fixed Drone Hangar Market

Executives evaluating drone-enabled operations at scale face a compressed window to secure first‑mover advantages while mitigating regulatory and integration risk. Our analysis shows the market crossing an inflection point entering 2026: demand pressures from industrial inspection, security/surveillance and logistics use cases, combined with maturing autonomous hangar technologies and modular construction techniques, create a credible path for enterprise deployments that were previously constrained to pilots.

Fixed Drone Hangar Market

Strategic timing: With the market value accelerating notably from the 2025 base, organisations that commit to prototype-to-rollout programs in 2026 are best positioned to influence standards, capture operational learning, and avoid higher retrofit costs later in the cycle.

Regulatory gating: BVLOS approvals and safety frameworks remain the primary deployment friction. The presence of FAA-approved test sites, PSP programs and EASA/CE conformant equipment will determine when hangars become operational assets rather than dormant infrastructure.

Capital planning: The high growth trajectory implies a significant CapEx runway. Strategic investors and operators should align multi-year budgets to the market ramp while preserving optionality for sensor, charging and communication upgrades.

Our study is structured for rapid operationalisation by corporate strategy teams, asset owners, and procurement committees. Highlights include:

Deployment playbooks — stepwise checklists covering site selection, environmental hardening, power provisioning (including off‑grid options), and commissioning for unattended fixed hangars.

TCO and CapEx/Opex matrices — configurable models for scenario analysis that help compare fabric-clad semi‑permanent solutions against hardened modular enclosures and purpose-built autonomous hangars.

BVLOS readiness framework — a pragmatic compliance roadmap that maps facility features (charging, telemetry, secure storage) to regulatory milestones and approval pathways in major jurisdictions.

Technology integration guides — guidance on communications (5G/mesh), automated docking and charging, environmental monitoring, and fleet management interoperability.

Procurement & supplier evaluation templates — scoring matrices and negotiation playbooks to de‑risk vendor selection and service-level commitments.

Scenario-based investment cases — three-staged strategic scenarios (baseline adoption, accelerated scale, regulatory-constrained) with decision gates, KPIs and timing recommendations.

At the market level, the report quantifies a clear growth path: the fixed drone hangar market moves substantially beyond pilot-scale economics in 2026 and, under our central forecast, expands multiple-fold by 2032 driven by both volume and increasing average selling prices for high‑automation hangars. These dynamics are propelled by the convergence of reliable autonomous docking/charging technologies, faster charging architectures, and the broader shift to persistent BVLOS operations that demand secure, weather‑protected, remotely operable facilities.

The competitive environment is a mix of specialised electromechanical integrators, UAV OEMs offering turn‑key hangar solutions, and civil/military fabric structure specialists. Key vendor archetypes include autonomous systems providers with docking/charging IP, modular hangar fabricators, and engineering firms that integrate comms, telemetry and environmental controls.

HEISHA Technology Co., Ltd. (Shenzhen): A rapidly advancing supplier focused on VTOL fixed‑wing hangars with autonomous docking and fleet management features. Their recent product introductions underscore a push toward tightly integrated hangar-management ecosystems tailored to inspection, logistics and emergency response workflows.

Skycharge (Germany): Positions itself as a standards‑driven provider with CE-certified weatherproof charging hangars designed for BVLOS operations. Their modular, cross-platform charging and adaptive docking tech is engineered for reliability in extreme climates.

JOUAV (Chengdu): UAV OEMs expanding into hangar systems are notable for delivering end‑to‑end VTOL automatic hangars that integrate vehicle, communications and hangar controls for unattended medium- and long‑term operations.

mb+Partner (mbptech, Germany): Offers hangar systems that function as mobile runways with embedded connectivity, ground carriage systems and on-site environmental sensing — attractive to operators requiring remote automated launch/land cycles.

Fabric structure specialists (e.g., Rubb, Liri Structure): Provide cost‑efficient semi‑permanent and permanent fabric-clad hangars with options for insulation and rapid deployment — a pragmatic choice where speed and thermal protection are priorities.

Other niche suppliers (including aluminium‑frame and rapid‑deploy solutions): Supply unique value for off‑grid, rapid deployment or special-mission contexts.

While the vendor field is diverse, market competition is increasingly defined by three capabilities: reliable autonomous docking and charging; hardened environmental protection (weather, temperature extremes); and integrated communications/fleet management for BVLOS. Firms that can bundle these capabilities — and demonstrate operational effectiveness in certified regulatory contexts — will capture disproportionate customer attention.

Regulation and standardization are not background noise; they actively shape procurement timing and technical specifications. Two imperatives are clear:

BVLOS approvals and test-site access: Operators require defined pathways (e.g., FAA PSPs, designated test corridors) to validate unattended hangar-based operations. Project timelines must embed regulatory milestones and field-testing windows.

Conformity to regional standards (e.g., CE for EU operations): Equipment-level certifications for weatherproofing, electrical safety and charging interoperability materially affect supplier selection and integration costs.

Practically, the lag between technology readiness and regulatory permission is the single most important programme risk to manage. The report provides a pragmatic regulatory engagement playbook to shorten approval lead times and align procurement with certification cycles.

Adopt an iterative rollout model: Treat the first generation of hangar deployments as platform-level investments. Design sites and contracts to support hardware and firmware upgrades without wholesale replacement.

Prioritise interoperability: Insist on modular charging interfaces, open telemetry protocols and standardised docking interfaces to avoid lock‑in and preserve upgrade flexibility.

Embed regulatory milestones in contracts: Link payment tranches and performance guarantees to specific BVLOS approvals and site certification achievements.

Consider hybrid sourcing: Combine specialist autonomous hangar providers with regional fabricator partners to balance speed, cost and environmental resilience.

Plan for energy resilience: Include off‑grid and backup power options as default line items in procurement, especially for remote inspection or public‑safety sites.

Conduct a 90‑day feasibility sprint: Validate sites, regulatory pathways and pilot supplier integrations to establish a deployment baseline.

Run TCO stress‑tests: Use scenario variants (high‑utilisation, low‑utilisation, delayed certification) to identify breakpoints where redesign or contractual protections are required.

Secure pilot partnerships: Negotiate pilot agreements with at least two vendor archetypes (autonomous integrator + fabric structure specialist) to compare operational cadence and service responsiveness.

Initiate regulatory engagement: Open dialogues with relevant aviation authorities and test-site operators to accelerate BVLOS cert processes and capture lessons learned from early adopters.

This report translates market momentum into boardroom-grade actions. Beyond headline growth figures, it synthesises supplier capabilities, regulatory levers, and field‑proven deployment tactics that allow executives to convert momentum into operational value. We surface the commercial tradeoffs — speed vs. resilience, CapEx vs. scalability, proprietary vs. interoperable systems — and translate them into clear, staged decision points for 2026.

For readers seeking the complete dataset, including granular regional and application splits, supplier share matrices, and the full suite of financial models and procurement templates, the full report provides the comprehensive evidence base and downloadable tools to operationalise these recommendations. Our disclosure approach here intentionally showcases strategic depth while reserving the detailed segmented figures and vendor share tables for the full report to support procurement diligence and capital approvals.

The fixed drone hangar market is no longer a niche adjacency to drone operations; it is a core infrastructure class that will determine who captures the productivity upside of BVLOS-enabled missions. Firms that act in 2026 — with clear regulatory strategies, modular technical architectures, and pragmatic procurement safeguards — will define industry best practice and secure durable advantages as the market scales. PW Consulting stands ready to partner with executive teams to translate this roadmap into capital plans, pilot designs and regulatory strategies tailored to your operational context.

For access to the full analysis, datasets and implementation toolkits, please consult PW Consulting’s Fixed Drone Hangar Market report and engagement services.

For detailed analysis of this topic, please visit the official page:Fixed Drone Hangar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com