Uttar Pradesh Pollution Control Board NOC Complete Guide for Businesses in UP (2026)

Other |

2026-05-28 06:19:08

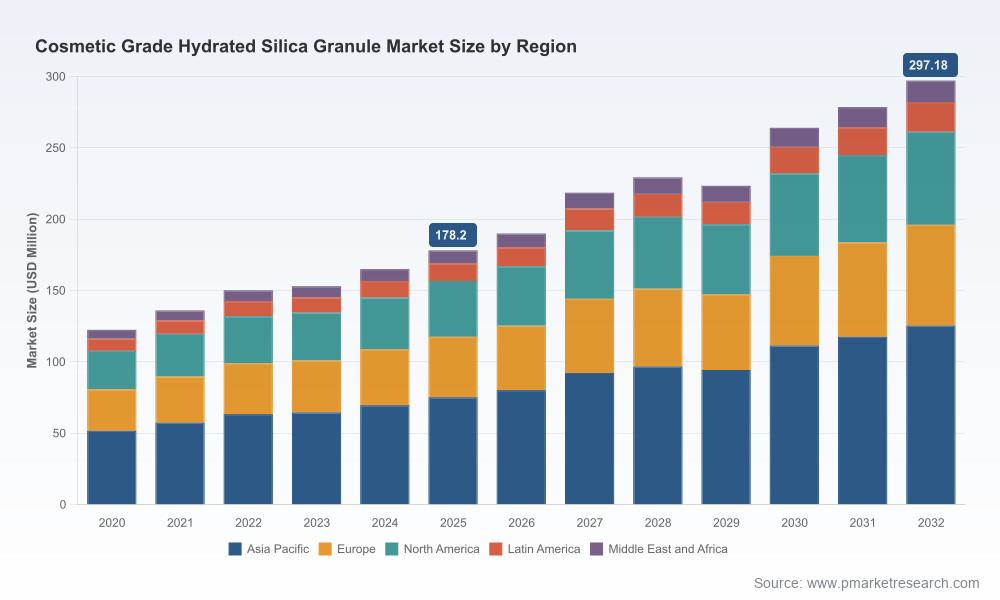

As demand for advanced tactile and optical effects in personal care intensifies, the cosmetic grade hydrated silica granule market is entering a phase of strategic reallocation rather than purely incremental expansion. Our new market study — covering historical performance (2020–2025) and projecting through 2032 — finds the industry on a sustained growth trajectory (7.58% CAGR for the forecast window), with the market value expanding from a strong 2025 baseline and approaching the high hundreds of millions (USD Million) by the end of the forecast horizon. For executives planning investments, supply agreements, or portfolio pivots in 2026, the insight set presented in this preview is intended to sharpen decision-making while directing readers to our full report for the complete data matrix and scenario tables.

Cosmetic Grade Hydrated Silica Granule Market

Timing: 2026 is a year in which supply chain realignments and product innovations launched in 2024–2025 begin to materially affect margin dynamics. Procurement teams need forward-looking cost curves tied to both feedstock and manufacturing energy assumptions; R&D leaders must calibrate formulations to meet evolving “clean” and sensory expectations without sacrificing cost-to-serve.

Cosmetic Grade Hydrated Silica Granule Market

Value capture: The market concentration profile shows meaningful aggregation among leading suppliers. With the top three players controlling a sizeable share and the top five commanding a clear majority, there is a structural opportunity for mid-tier producers and brand owners to differentiate through specialty grades, service models, and supply-chain resilience rather than competing on commodity pricing alone.

Cosmetic Grade Hydrated Silica Granule Market

Regulatory clarity and product stewardship: Contemporary safety assessments distinguish synthetic amorphous hydrated silica from crystalline forms. That distinction underpins new product claims, compliance roadmaps, and risk registers for cosmetic formulators — an operationally critical point for 2026 launches.

Demand-side innovation: Cosmetic R&D is prioritizing textures that deliver mattifying, oil-control and soft-focus optical effects across foundations, powders, and skincare. These functional requirements create a premiumization pathway for specialty hydrated silica grades that combine tailored particle morphology with surface treatment options.

Upstream cost signals: Sodium silicate remains the primary feedstock for precipitated hydrated silica. As of February 2026, benchmark sodium silicate pricing averaged roughly USD 0.55/Kg in Northeast Asia and USD 0.63/Kg in Europe. These figures — and their regionally divergent trajectories — are the principal levers behind raw material-driven margin variability for manufacturers and should be a core input into 2026 procurement strategies and contract design.

Manufacturing and energy exposure: Production of precipitated hydrated silica is energy intensive and sensitive to soda ash and silica sand feedstock inputs. Energy-cost volatility and regional energy policy shifts in 2025–2026 can rapidly change unit economics; scenario planning must therefore model both short-cycle and structural energy scenarios.

Regulatory and safety frameworks: Industry-endorsed safety assessments affirm safe use of amorphous hydrated silica when formulated appropriately. That regulatory clarity reduces uncertainty for brands but raises the bar for documentation, batch-level traceability, and supplier certifications — especially for export-oriented manufacturers.

Forward-looking market model: A transparent, auditable revenue and volume model spanning 2020–2032 with baseline and alternative macro scenarios, allowing users to stress-test assumptions (raw material prices, energy, product substitution rates, and end-market elasticity).

Price-sensitivity and margin maps: Granular margin decompositions by manufacturing archetype and sensitivity tables tied to sodium silicate, energy, and labor inputs — designed for procurement and FP&A teams to build hedges and contractual protections.

Go-to-market playbooks: Tactical guidance for manufacturers and ingredient suppliers on product positioning (e.g., mattification vs. exfoliation), sample-to-scale timelines, and qualification checklists tailored to OEMs and brands in premium, mass, and oral-care segments.

Regulatory and compliance toolkit: Batch-level documentation templates, EU and ISO alignment checkpoints, and a safety-assessment primer that maps to common cosmetic regulatory submissions.

Supplier due-diligence and M&A framework: Playbooks for evaluating acquisition targets and JV partners, including a five-step diligence on production footprint, instrumentation for particle-size control, environmental performance, and customer concentration risk.

Competitive intelligence appendices: Company profiles, strategic positioning maps, recent product launches and compliance updates, and a short-list of potential strategic partners by capability.

Evonik Industries (Essen, Germany) — A technology-led incumbent offering specialty hydrated silica grades designed for mattifying, oil absorption, and soft-focus performance. Their portfolio is aligned to high-specification demands from prestige cosmetics and offers a ready blueprint for partnerships where formulation performance and regulatory assurance are decisive. Strategy tip: collaborate on co-development for proprietary surface modifications to secure exclusive supply agreements.

Fuji Silysia Chemical Ltd. (Kasugai City, Japan) — Known for tightly controlled particle-sizing and absorption properties in synthetic silica powders, making them a logical partner for formulators seeking reproducible texture and stability. Strategy tip: licensing or preferred-supplier arrangements for APAC-based formulation centers can accelerate time-to-market while hedging against regional supply disruptions.

Shanghai Co-Fun Biotech Co., Ltd. (Shanghai, China) — Recently launched a new grade emphasizing high silica content and broad dispersibility across water, polyol and oil phases. The move signals intensified competition from Chinese specialty producers on performance parity and cost. Strategy tip: evaluate pilot collaborations on cost-effective specialty grades and lock-in technical support as a market-entry wedge.

Jinsha Precipitated Silica Manufacturing Co., Ltd. (China) — Publicly emphasized compliance upgrades and adherence to ISO and EU cosmetic safety standards late in 2025, reinforcing their export credentials. Strategy tip: global brands seeking multi-sourcing options should prioritize suppliers that can demonstrate up-to-date compliance and environmental credentials to minimize non-tariff barriers.

Henan Xunyu Chemical Co., Ltd. (Zhengzhou, China) — A fumed silica specialist whose products often complement precipitated grades in formulations. Strategy tip: identify blended silica solutions (fumed + hydrated) that achieve targeted rheology or aesthetic effects with cost efficiency.

Alfa Chemistry (United States) — A supplier oriented to high-purity, high-dispersibility grades. The company is an option for brands that need rapid technical service and sample turnaround in North America. Strategy tip: leverage short lead-time suppliers for localized innovation sprints and limited-run launches.

PPG Industries (Pittsburgh, USA) — A major producer whose scale and distribution networks make it a strategic counterparty for large-volume requirements. Strategy tip: consider volume-based contracting with indexed pricing mechanisms tied to sodium silicate benchmarks to secure supply while sharing price risk.

Huber Engineered Materials (Atlanta, USA) — Provider of high-purity precipitated hydrated silica used across oral care and cosmetic formulations. Strategy tip: prioritize suppliers with deep oral-care track records if targeting multi-category launches.

Compliance emphasis: One regional producer finalized manufacturing documentation and certifications aligning to ISO and EU cosmetic safety frameworks in late 2025 — a trend that will influence global OEM sourcing policies in 2026.

New product introductions: A notable supplier launched a >97% silica content hydrated silica grade with a broad dispersibility profile in mid-2025, reflecting an industry-wide move toward higher-purity, multi-phase-compatible grades that simplify formulation workflows.

Raw material pricing signals: Across Q4 2025 and into early 2026, sodium silicate pricing displayed regional variance and short-term softness in select markets. Procurement teams must translate these signals into layered buying strategies, blending spot, forward and contract purchases.

Procurement: Reassess contracts with indexed pricing clauses tied to sodium silicate and energy benchmarks; secure optionality through secondary suppliers to mitigate single-source risk.

R&D: Run two parallel formulation tracks — one that leverages existing commodity grades for cost-optimized SKUs, and a second that co-develops specialty grades with suppliers for premium launches.

Regulatory & QA: Update supplier qualification checklists to include the latest batch-traceability and safety-assessment documentation; prioritize suppliers that can demonstrate export-ready compliance.

Commercial: Segment customers by sensitivity to texture and optical benefits versus price, and align commercial offers (sample packs, co-marketing, exclusivity pilots) accordingly.

M&A and partnerships: Use the report’s diligence framework to shortlist targets for capability fill-ins (particle engineering, surface modification or regional manufacturing footprints).

For executives who need a defensible view of strategic options in 2026, the right next step is an evidence-based synthesis that aligns sourcing, R&D and commercial workstreams to the market’s medium-term trajectory. Our full PW Consulting market report contains the complete forecast tables, segmented analytics, supplier scorecards and executable playbooks that will materially reduce execution risk and accelerate time-to-revenue for new formulations and sourcing strategies. This preview provides the directional thesis; the full dataset and appendices provide the operational levers.

To access the full market model, supplier appendices, and a tailored briefing for your organization, please consult the PW Consulting report landing page referenced in your proprietary distribution channels.

For detailed analysis of this topic, please visit the official page:Cosmetic Grade Hydrated Silica Granule Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com