Non‑Alcoholic Beverage Flavoring System Market — Strategic Outlook for 2026 Decision‑Makers

PW Consulting’s latest market research report on the Non‑Alcoholic Beverage Flavoring System market provides a rigorous, decision‑oriented roadmap for beverage companies, ingredient suppliers, and investors preparing for 2026. Built on a comprehensive 2020–2025 historical base and an analytically robust 2026–2032 forecast, the study decodes growth drivers, competitive positioning and tactical moves that will determine winners in an increasingly health‑ and sustainability‑focused landscape.

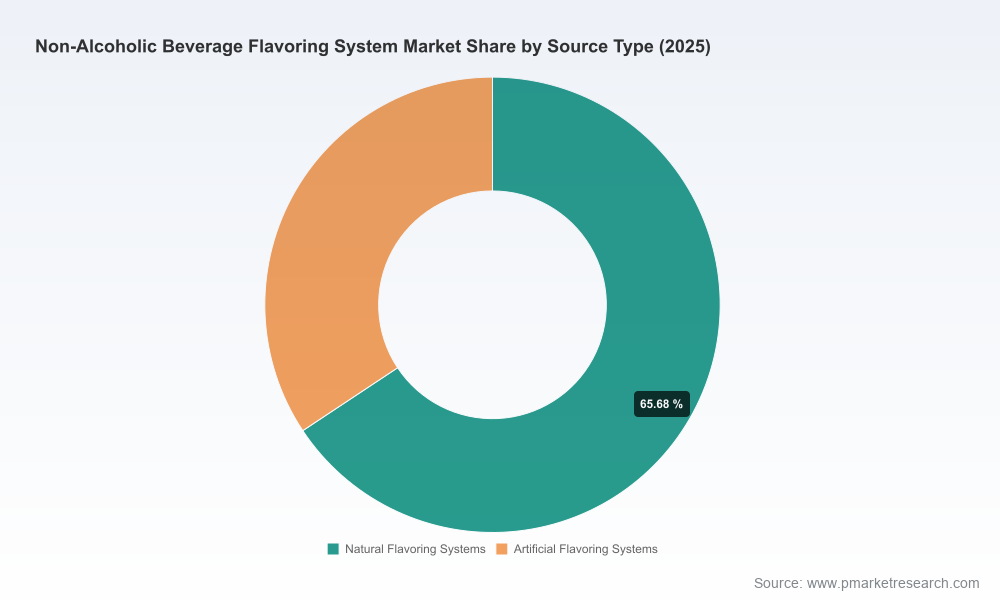

Non Alcoholic Beverage Flavoring System Market

High‑level market trajectory: what the numbers tell us

After recovering from pandemic‑era disruption, the global market for non‑alcoholic beverage flavoring systems reached approximately USD 5,241.15 Million in the 2025 base year and is projected to continue expanding through the 2026–2032 forecast window. Our modeled compound annual growth rate (CAGR) for the forecast period is 5.82%, and baseline scenario projections show the market approaching roughly USD 7,787.55 Million by 2032 (all figures in USD Million unless otherwise noted). These macro dynamics reflect a market maturing toward premiumization, ingredient transparency, and formulation innovation rather than rapid commoditization.

Non Alcoholic Beverage Flavoring System Market

Concentration metrics further contextualize strategic options: the top three suppliers account for a material but not overwhelming share of the market (CR3 ~38.5%), while the top five push that concentration to just over half (CR5 ~54.2%). In practice, that creates a competitive environment in which scale and global reach matter, but nimble innovation and targeted partnerships can differentiate smaller players.

Non Alcoholic Beverage Flavoring System Market

Why this report matters for 2026 decisions

- Timing of investment: 2026 will be the inflection year for converting R&D pilots into commercially scaled offerings as formulators respond to regulatory pressure on sugar and labeling mandates tied to health claims. Our scenario analyses identify the points at which investment in encapsulation, delivery systems and taste modulation achieves payback under conservative demand assumptions.

- Supplier selection under constrained inputs: Raw material volatility—including price and availability for key citrus and botanical extracts—necessitates rigorous supplier risk scoring. The report provides procurement playbooks and stress‑test templates designed for 2026 contracting cycles.

- Portfolio prioritization: We offer a practical decision matrix to prioritize SKU rationalization versus innovation launches, balancing margin targets with required CAPEX and time‑to‑market considerations.

Core actionable intelligence included in the report

- Proprietary demand model and sensitivity testing that translates ingredient cost and consumer adoption scenarios into P&L impacts for beverage manufacturers.

- Granular innovation blueprints: formulations and delivery system archetypes for clean‑label, reduced‑sugar and functional beverages—aligned to manufacturability and shelf‑life constraints.

- A procurement risk matrix and dual‑sourcing playbook that integrates supplier financial health, geographic footprint and extract supply chains.

- Regulatory and labeling heatmap covering major markets and forecasted changes through 2032, with implications for ingredient declarations, “natural” claims and health‑adjacent claims.

- M&A and partnership screening criteria calibrated to the market’s mid‑consolidation phase—tailored to either scale up R&D capability or to secure specialty botanical sources.

- Commercial go‑to‑market templates for successful trial conversion, including trade sampling cadence, co‑branding approaches with ingredient suppliers, and ROI metrics for pilot investments.

Competitive landscape: who’s shaping the ecosystem

The competitive set spans multinational flavor houses, agricultural ingredient integrators, and specialized natural‑ingredient boutiques. Large flavor companies maintain advantages in global distribution, scale of R&D, and regulatory expertise—making them natural partners for beverage majors seeking rapid product launches. Mid‑sized and specialty players, by contrast, are competing on agility, botanical expertise and proprietary delivery formats.

- Givaudan (Vernier, Switzerland) — Positioned as a market leader with deep capabilities in natural and sustainable flavor systems. Their strategy emphasizes clean‑label solutions and advanced delivery systems that enable premium, health‑oriented beverages to meet consumer taste expectations.

- International Flavors & Fragrances (IFF, New York) — Offers broad beverage flavoring capabilities, including taste modulation and encapsulation. Their portfolio is well suited to manufacturers balancing reformulation (sugar reduction) and shelf stability.

- Symrise (Holzminden, Germany) — Strong R&D focus on natural ingredients and functional flavor solutions, well positioned to support botanical and wellness trends.

- Kerry Group (Tralee, Ireland) — Known for clean‑label and functional flavor systems, with strengths in integrating taste and nutritional optimization.

- Sensient Technologies (Milwaukee) — Emphasizes vibrant natural profiles and advanced delivery mechanisms, often working with premium beverage brands.

- dsm‑firmenich (Kaiseraugst, Switzerland) — Combines sustainability credentials with performance‑driven flavor innovations—strategically relevant where ESG claims matter.

- ADM and Cargill (Chicago/Minneapolis) — Large ingredient integrators offering carrier systems, emulsions and scale advantages, attractive for beverage players targeting cost‑efficient reformulations.

- Tate & Lyle, Takasago, MANE, Döhler, Robertet — Each of these players brings specialized capabilities: sweetener‑flavor integration, botanical expertise, compound and syrup systems, or premium natural extracts aimed at differentiated beverage concepts.

Recent corporate moves underline strategic priorities across the ecosystem. For example, Döhler’s capacity expansion in early 2025 signals supplier readiness to meet higher demand for liquid and compound systems; Robertet’s 2024 “Futuring Naturals” platform formalizes a bet on premium botanical extracts; and smaller innovators are releasing plant‑based flavor lines that specifically target vegan and clean‑label beverage segments. These developments create both opportunities and sourcing risks for beverage manufacturers planning 2026 launches.

Market dynamics shaping strategy

- Consumer preferences: There is strong demand for complex, botanical‑inspired flavor profiles—elderflower, yuzu, lemongrass and lavender are cited by category watchers as accelerating. This consumer pull favors suppliers with botanical extraction capabilities and creative flavor R&D.

- Health and regulation: Sugar reduction, functional ingredient fortification, and stricter labeling mandates are forcing formulators to adopt taste‑modulating systems and to justify claims with verifiable ingredient provenance.

- Raw material context: Citrus and botanical extracts remain foundational inputs; separate market intelligence projects the global citrus‑flavors subsector at an elevated valuation in 2026, indicating both demand strength and potential pricing pressures.

- Supply chain and sustainability: Traceability and sustainable sourcing are no longer optional—buyers will need supplier audits, chain‑of‑custody documentation, and contingency plans by 2026 to satisfy customers and regulators alike.

Strategic playbook for 2026

For C‑suite and product leaders, the following high‑impact moves can be executed in 2026 to capture market share and protect margins:

- Prioritize platform technologies: Select one or two delivery technologies (e.g., encapsulation, emulsions) to industrialize across your portfolio. Concentrating CAPEX accelerates time to market and reduces unit development cost.

- Dual‑track sourcing: Combine incumbent global suppliers for scale with niche botanical houses for differentiation. Use contract flexibility (volume bands, lead‑time SLAs) to manage raw material volatility.

- Accelerate reformulation squads: Create cross‑functional teams (R&D, procurement, regulatory, commercial) focused on sugar reduction and functionalization, with clear sprint milestones and go/no‑go decision gates aligned to 2026 retail windows.

- Monetize sustainability: Translate sustainable sourcing and clean‑label provenance into premium positioning with supported claims and co‑marketing with ingredient suppliers.

- Use M&A selectively: Target bolt‑on acquisitions that add unique botanical portfolios or delivery IP rather than chasing scale alone—given the current CR3/CR5 structure, strategically chosen acquisitions can materially improve differentiation without requiring market domination.

Report structure and methodological transparency

Our report is designed for rapid applicability. It includes a transparent methodology section, data sources, and the full modelling logic used to produce forecasts. Readers will find:

- Scenario‑based forecasts (base, upside, downside) and sensitivity tables;

- Supplier scorecards and competitive SWOT assessments;

- Commercialization timelines and cost‑of‑goods modeling templates;

- Regulatory roadmaps and labeling checklists by jurisdiction;

- Industry case studies and playbooks you can operationalize in 90–180 days.

To preserve the integrity of competitive advantage and to comply with our “trailer” approach, we intentionally withhold certain granular segment and regional breakdowns from this press release. The full report contains the detailed segmentations, contractual templates and Excel models that executives will use to finalize budgets and supplier agreements for 2026 initiatives.

Next steps for executives

If your 2026 planning cycle includes new beverage launches, major reformulations, or supplier renegotiations, PW Consulting recommends commissioning a targeted advisory engagement to translate report insights into a bespoke implementation plan. Typical engagements prioritize one of three tracks: product innovation and scale‑up, procurement and supply‑risk management, or M&A and strategic partnerships. Each engagement begins with a 2‑week diagnostic that benchmarks your capabilities against the market and delivers a prioritized action plan.

For a complete copy of the report, the embedded models, and to request a briefing with our lead analysts, please visit the full report page. The downloadable assets include the forecast workbooks and decision‑making tools you will need to operationalize your 2026 strategy.

For detailed analysis of this topic, please visit the official page:Non Alcoholic Beverage Flavoring System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com