MPPO Resin for CCL Market: Strategic Intelligence to Shape 2026 Decisions

As PW Consulting releases its latest market research brief on MPPO (modified polyphenylene oxide) resin for copper-clad laminates (CCL), this executive synopsis highlights the report’s strategic value for corporate leaders planning capacity, procurement, R&D, and go‑to‑market moves in 2026. Our analysis synthesizes supply‑side shifts, end‑market demand from 5G, AI and automotive electronics, and regulatory imperatives to produce pragmatic decision frameworks — while preserving proprietary segmentation detail to drive readers to the full report for executable numbers and granular scenarios.

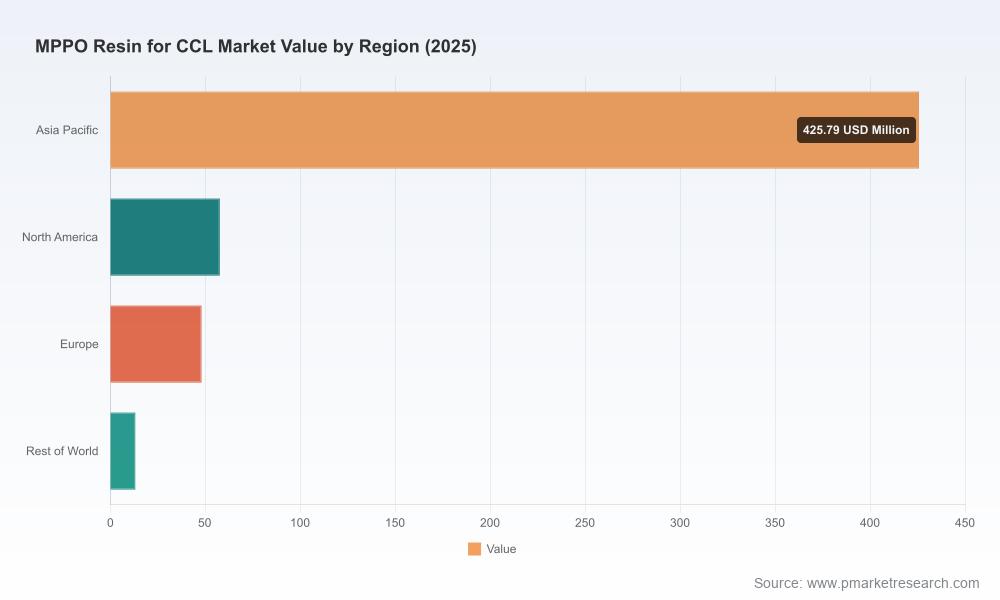

Mppo Resin For Ccl Market

Macro view: growth trajectory and concentration

The MPPO-for-CCL market is in a multi‑year expansion phase. Our modeling shows a robust compound annual growth rate (CAGR) of 12.48% across the 2026–2032 forecast window. That pace translates into a material scale-up in total market value from early‑2020s baselines to a point well above USD 1 billion by 2032, reflecting accelerating demand for low-loss, high-frequency laminates used in advanced communications and compute platforms. Market concentration is notable: the three largest suppliers account for roughly 62% of the market, and the top five for nearly 79%, indicating both scale advantages and meaningful barriers for insurgents.

Mppo Resin For Ccl Market

Why this report matters for 2026 strategic choices

- Capacity and timing: Several industry players have signaled expansions and greenfield projects timed through 2026–2027. Our report maps optimal timing windows for brownfield debottlenecking versus new capacity, balancing lead times, CAPEX intensity and first‑mover pricing leverage.

- Procurement and feedstock risk: With 2,6‑xylenol and related phenolic feedstocks driving a significant fraction of input cost, procurement strategies must move beyond spot buys. The study lays out hedging scenarios, contract structures and near‑term price sensitivity analyses tuned to 2026 budgeting cycles.

- Product & process roadmaps: Customers demand low dielectric loss, dimensional stability and flame retardancy — often simultaneously. We grade technical pathways (oligomer design, end‑capping chemistries, halogen‑free formulations) against TRL and manufacturability to prioritize R&D investments for 2026 milestones.

- Regulatory readiness: REACH and RoHS compliance, plus tightening local VOC and flame‑retardant restrictions, require product certifications and testing roadmaps. The report provides compliance checklists and estimated lead times for certification that align with 2026 product launches.

Key dynamics shaping supplier economics

- End-market pull: The convergence of 5G base stations, high‑speed AI servers and advanced automotive electronics propels demand for MPPO grades optimized for high-frequency and low-loss performance. Our demand model decomposes growth drivers and identifies which application clusters will absorb incremental supply across the 2026–2032 horizon.

- Feedstock volatility: 2,6‑xylenol price swings materially affect margins and price elasticity. We quantify break‑even ranges for different asset configurations and show how feedstock exposure influences preferred commercial models (fixed‑price contracts, passthrough clauses, or joint procurement).

- Premium pricing for differentiated grades: Specialty grades — e.g., halogen‑free, hydroxy‑functional or high‑molecular‑weight variants — command premiums due to higher raw‑material and processing costs. The report outlines margin waterfalls and tolerance thresholds for customers in different end markets.

- Consolidation pressure: High CR3/CR5 concentration suggests incumbent advantage in qualification cycles and customer lock‑in. Yet pockets of opportunity remain for agile specialists and regional players with deep application know‑how.

What the report contains — operational, actionable modules

PW Consulting has structured the study for immediate utility by commercial, operations and corporate development teams. Key components include:

Mppo Resin For Ccl Market

- Market sizing and forecasting methodology — transparent assumptions, sensitivity scenarios and an interactive forecasting model suitable for 2026 planning cycles.

- Demand segmentation framework — end‑market drivers, adoption curves and qualification lead times for critical applications (detailed segmentation tables are included in the full report).

- Supply chain maps and capacity registry — plant-level profiles, ramp schedules and utilization scenarios that support CAPEX and sourcing decisions.

- Cost‑to‑serve and margin modeling — unit economics for core and specialty grades under varying feedstock and energy price cases.

- Competitive benchmarking — technical and commercial positioning of leading suppliers, with a focus on product portfolios, capacity footprints and go‑to‑market capabilities.

- Regulatory and ESG playbook — compliance requirements, test matrices, and practical timelines for certifying new grades for target markets.

- M&A & partnership screening tool — an action‑oriented rubric to prioritize targets, structure deals, and quantify synergies for 2026‑era transactions.

- Case studies and supplier negotiation scripts — real‑world examples and templated terms to accelerate supplier qualification and long‑term purchase agreements.

Competitive landscape: who matters and why

The report’s competitive analysis goes beyond logos to appraise each player on three axes: technical differentiation, scale of operations, and commercial reach. Highlights include:

- SABIC — leverages NORYL oligomer chemistry for low‑loss, thermoset‑compatible systems. Its announced capacity addition through 2026 is a strategic lever to capture AI/data center demand and support Tier‑1 PCB makers.

- Asahi Kasei — long‑standing expertise in modified PPE chemistries positions it favorably in high‑frequency applications where dielectric performance and dimensional control are decisive.

- Mitsubishi Gas Chemical — known for tailored modified PPO oligomers for telecom and high‑frequency PCBs; benefits from close OEM relationships in key Asian markets.

- Bluestar New Chemical Materials (China National Chemical Corporation) — the principal domestic industrial-scale resin supplier in China, providing a resilient local source for downstream formulators.

- Unifarm Chemical, Kolon Industries, LG Chem — each offers differentiated grades and regional commercial strength; together they exemplify the blend of specialty chemistry and industrial backing shaping the competitive set.

- Emerging domestic projects — projects announced by regional players indicate a growing local supply base; the report evaluates technical readiness, qualification hurdles and realistic ramp timetables for these newcomers.

Strategic implications and recommended 2026 playbook

For executives setting priorities in 2026, the following actions can materially de‑risk growth and create competitive advantage:

- Lock strategic feedstock arrangements. Structure multi‑year agreements with price escalation mechanisms tied to input indices to stabilize margins while preserving upside participation.

- Prioritize product and process modularity. Invest in chemistry platforms that allow rapid customization (low‑loss, halogen‑free, hydroxy‑functional) with minimal scale‑up latency.

- Time capacity investments to customer qualification cycles. Align new capacity commissioning with the typical 9–18 month customer qualification and pilot windows for CCL materials to avoid idle assets.

- Negotiate qualification partnerships with tiered pricing. Use pilot programs and co‑development agreements to shorten qualification times and create switching costs for customers.

- Embed regulatory and ESG milestones in product development. Plan for certification lead times and allocate engineering resources for halogen‑free and low‑VOC formulations early in 2026 R&D roadmaps.

- Use M&A and JV selectively. Target assets that provide technology adjacency (oligomer platforms) or regional production to bypass tariff and logistics friction for fast-growing end‑markets.

How buyers and investors should use the report

- Procurement teams: adopt the supplier scorecards and cost models to redesign sourcing strategies and reduce exposure to feedstock volatility.

- R&D leaders: leverage the technology readiness assessments to prioritize projects that achieve marketable differentiation by late 2026.

- Operations and plant managers: run the capacity utilization scenarios and CAPEX phasing guidance to set realistic commissioning targets and avoid overcapacity.

- Corporate development teams: apply the M&A screening tool and competitive positioning maps to identify consolidation targets and partnership opportunities.

Conclusion — the strategic edge for 2026

As MPPO resin demand accelerates with the rollout of 5G infrastructure, growth in AI compute, and rising electronic content in vehicles, the decisions made in 2026 — on capacity, procurement, product development and partnerships — will set winners apart. PW Consulting’s MPPO for CCL study combines market foresight, supply‑chain realism and actionable playbooks to guide those choices. The public summary above outlines our core conclusions while deliberately omitting granular segmentation and proprietary tables that are essential for transaction‑level decisions; these are available in the full report.

Next steps

For a detailed briefing, interactive model access, and bespoke scenario workshops tailored to your portfolio or procurement pipeline, contact PW Consulting to arrange a demonstration of the full MPPO resin for CCL market study. The full report contains the proprietary segmentation, downloadable models and contract templates required to operationalize a 2026 strategy.

For detailed analysis of this topic, please visit the official page:Mppo Resin For Ccl Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com