Municipal Water Treatment Market 2026: Strategic Insights for Decision-Makers

Executive summary

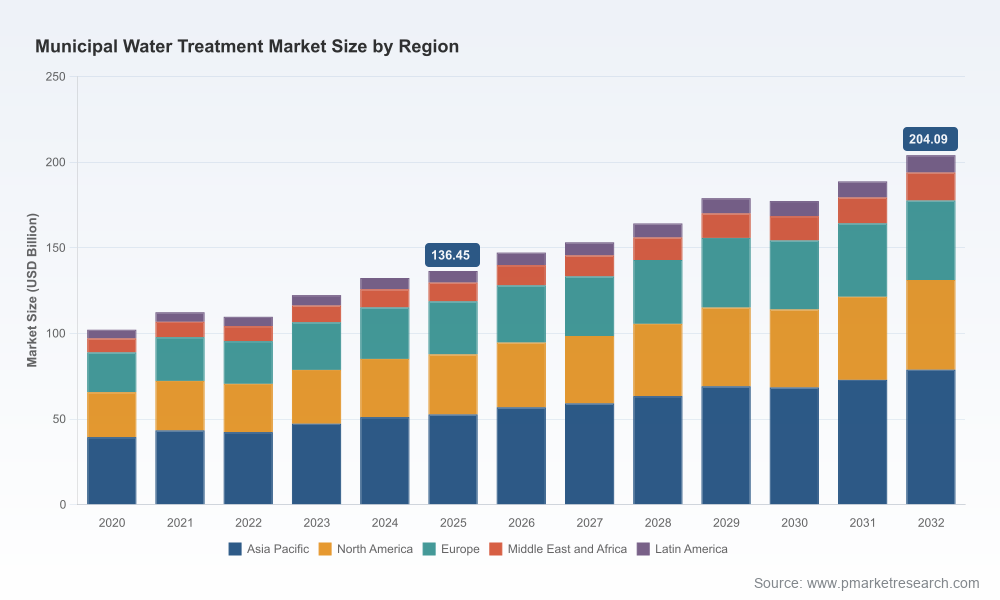

PW Consulting’s latest Municipal Water Treatment Market report positions 2026 as a pivot year for municipal utilities, chemical suppliers, technology providers, and investors. The market reached USD 136.45 Billion in the base year (2025) and is forecast to expand at a 5.92% CAGR over the 2026–2032 forecast horizon, reaching roughly USD 204.09 Billion by 2032. These headline numbers mask a complex interplay of regulatory pushes, raw-material cost swings, technology shifts, and competitive repositioning that will determine winners and laggards in the coming three to five years.

Municipal Water Treatment Market

Why 2026 matters: regulatory and funding inflection points

Two converging regulatory impulses make 2026 uniquely consequential. First, the European Drinking Water Directive recast entered application in January 2026, introducing harmonised PFAS monitoring and tighter limit values for emerging contaminants. Second, U.S. federal guidance for FY 2025–2026 prioritises PFAS reduction, lead pipe replacement and infrastructure upgrades—supported by Bipartisan Infrastructure Law funding streams. Together, these developments shift municipal procurement from discrete projects toward sustained, multi-year programs that combine capital replacement, treatment upgrades, and asset rehabilitation.

Municipal Water Treatment Market

Market structure and strategic implications

The market remains moderately fragmented: the top three players capture a relatively small portion of the market compared with other utility sectors, and the top five still represent just over a quarter of market share—an architecture that sustains both competitive intensity and inorganic consolidation opportunities. For strategic planners this means:

Municipal Water Treatment Market

- Utilities: plan integrated long-range capital programs rather than one-off retrofits. Regulatory timelines and programmatic funding favour bundled solutions (treatment + monitoring + asset replacement).

- Chemical and materials suppliers: prepare for demand volatility driven by raw-material price cycles and substitution pressures as regulations incentivise alternative treatment routes (e.g., adsorption vs. advanced oxidation).

- Technology vendors and integrators: differentiate through lifecycle service models, digital performance guarantees, and modular designs that lower near-term capex while securing recurring opex.

- Investors and M&A strategists: target scale and service capability rather than pure technology bets—assets that can be bundled into recurring revenue streams will command premium valuations.

Recent market activity and what it signals

- Operational scale-ups: In mid-2025 a major operator inaugurated a PFAS removal plant based on granulated activated carbon to treat a sizable municipal population, signalling strong demand for proven end-of-pipe PFAS solutions and the commercial viability of large-scale adsorption facilities.

- M&A and capability acquisition: Late-2025 transactions show established chemical suppliers and specialty-chemical players consolidating domain expertise—examples include acquisitions that add proprietary disinfectant and industrial water portfolios, expanding addressable markets into institutional and municipal niches.

- Strategic roll-ups: acquisitions that broaden municipal and industrial coverage reflect a trend toward integrated service offerings (chemical + digital dosing + monitoring) which reduce customer switching cost and raise lifetime value.

Raw-materials, cost inflation, and procurement risk

Supply-chain and commodity dynamics will materially affect treatment economics. Key inputs experienced notable price movement through 2025: polyaluminium chloride grades traded in an elevated range from China, ferric chloride prices rose in the U.S., and sodium hypochlorite costs increased in Europe. These movements translate directly into utility opex and into vendor margin pressure. Our scenario modules show that even modest feedstock price shocks can widen payback timelines for retrofits and shift the attractiveness of technologies that are chemically intensive versus those that consume electricity or membranes.

Report deliverables: practical tools for 2026 decisions

PW Consulting’s report is designed as an operator’s and investor’s toolkit rather than a purely descriptive market survey. Key actionable deliverables include:

- Regional and global market sizing with topline forecasts (2026–2032) and sensitivity bands tied to funding scenarios and regulation timelines.

- Capex–opex modelling templates for common municipal upgrade paths (PFAS removal, drinking-water compliance upgrades, sludge management), enabling customizable ROI and payback analysis.

- Vendor scorecards and procurement playbooks that assess technology fit, delivery risk, lifecycle cost, and service-readiness for bundled contracts.

- Regulatory impact matrices that map new and pending rules to treatment pathways and compliance milestones—designed to support capital planning and permitting strategies.

- Raw material price-sensitivity analysis and hedging recommendations for chemical-intensive operations, including procurement tactics to reduce exposure to single-source suppliers.

- M&A and partnership maps highlighting bolt-on acquisition targets, integration risks, and value-creation levers for platform buyers.

- Digital and retrofit roadmaps describing staged technology adoption—how sensors, remote O&M and performance contracts can be used to derisk large capital programs.

Competitive landscape: positioning and value propositions

The market’s leading vendors exhibit distinct strategic postures that matter to buyers and partners:

- Global integrators (e.g., legacy multinational operators) are leveraging scale and balance-sheet strength to offer full-service programs: design-build-operate, chemical supply, and long-term performance guarantees. Their strategic play is to capture programmatic utility spend tied to infrastructure upgrade cycles.

- Chemical specialists focus on portfolio depth and technical differentiation—investment in proprietary chemistries, flocculants, coagulants and specialty additives secures stickiness with utilities that prioritise predictable treatment performance and cost stability.

- Equipment and systems vendors differentiate through digital augmentation and modular designs, aiming to reduce onsite complexity and enable faster deployment—an attractive value proposition for utilities managing workforce constraints.

- Regional champions and mid-market players compete on agility, local presence, and tailored service contracts—attributes that become critical in fragmented procurement markets and municipal tendering processes.

Recent notable moves—capacity expansion for PFAS treatment, and acquisitions that bring proprietary disinfectant technologies and complementary industrial water portfolios into the municipal sphere—illustrate two parallel strategies: invest in end-market growth areas (PFAS, lead remediation) and expand solution breadth through M&A to capture cross-sell opportunities.

Risk map and scenario planning

Key downside risks for 2026–2028 include: delayed disbursement of public funds, slower-than-expected technology acceptance for expensive treatment routes, and raw-material price spikes that erode vendor margins. Upside scenarios are driven by accelerated regulatory enforcement, breakthrough cost reductions in advanced oxidation or adsorption media, and successful bundling of long-term service agreements that convert capex into recurring revenue.

How leading organisations should use this report in 2026

- Utilities: use the capex–opex templates and regulatory timelines to align multi-year workplans with anticipated funding windows and to phase interventions to maximise federal and regional grant leverage.

- Chemical suppliers: prioritise R&D and supply-chain resilience investments in chemistries exposed to price volatility, and evaluate bolt-on acquisitions that broaden municipal service lines.

- Technology vendors: focus on modular offerings and digital service layers that reduce integration friction for utilities with limited project management capacity.

- Private equity and strategic acquirers: screen targets using our vendor scorecards and M&A maps to identify assets that improve margins through cross-selling and recurring service revenue.

Next steps and access to the full intelligence

This briefing highlights the strategic contours that will shape municipal water treatment decisions in 2026—regulatory catalysts, raw-material volatility, fragmentation in market structure, and strategic moves by established and specialist players. PW Consulting’s full report contains the detailed regional and application breakdowns, granular segmentation, company financial benchmarks, and downloadable modelling templates that equip teams to operationalise these insights. To evaluate specific scenarios, procure the model kits, or request customised advisory support, please consult the full report on our website.

PW Consulting—translating market complexity into pragmatic strategy for water-sector leaders.

For detailed analysis of this topic, please visit the official page:Municipal Water Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com