Europe Automotive Battery Thermal Management System Market Size & Growth Trends Report (2026–2033)

Other |

2026-04-30 08:37:44

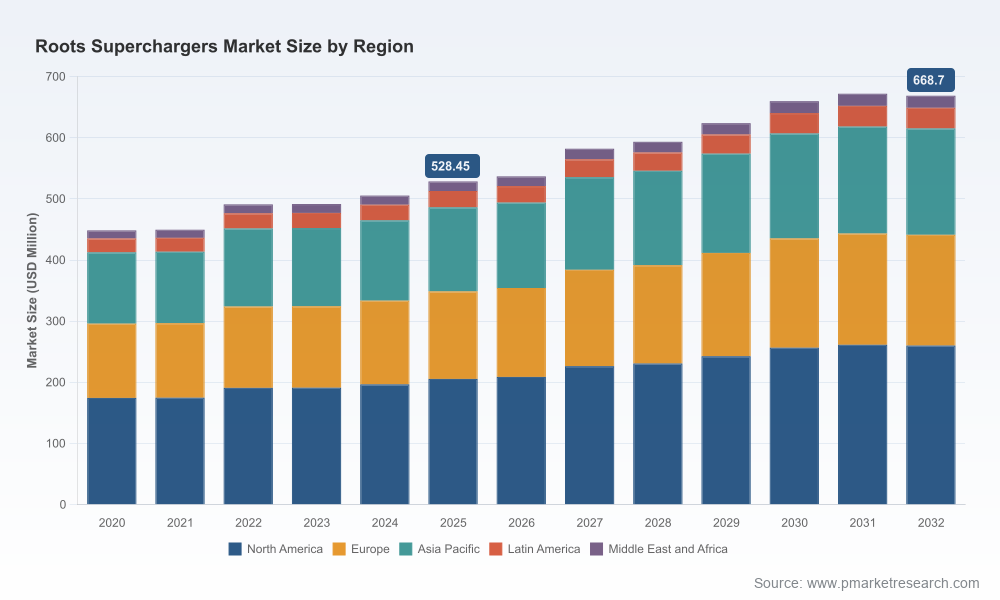

PW Consulting’s latest Roots Superchargers Market report delivers the strategic intelligence senior leaders need to make high‑confidence decisions in 2026. Anchored on a rigorous base year of 2025 and a documented historical window from 2020–2025, the study projects the market through 2032. Our analysis shows the global market expanding from a 2025 revenue base of USD 528.45 Million to an estimated USD 668.70 Million by 2032, reflecting a compound annual growth rate (CAGR) of 3.42% across the forecast horizon. These macro figures frame a market that is mature yet actionable: concentrated among a small set of scale players while offering very specific pockets of technical and aftermarket upside for agile competitors and investors.

Roots Superchargers Market

Clarity in scale and pace: The report translates headline growth into operational targets — capacity plans, product investments, and M&A timing — so that management teams can align 2026 budgets to realistic market trajectories rather than anecdote.

Roots Superchargers Market

Competitive concentration: With the three‑player concentration (CR3) and five‑player concentration (CR5) metrics indicating a market dominated by established manufacturers, the research identifies the competitive levers (volume scale, OEM relationships, performance IP) that determine success.

Roots Superchargers Market

Regulatory and materials lens: The study integrates emerging regulatory pressures (for example, Euro 7 and tightened CAFE requirements) and raw‑material and manufacturing constraints into scenario planning so R&D and compliance teams can prioritize feature sets that deliver both performance and emissions compliance.

Executionable playbooks: Beyond forecasts and trend maps, the report provides practical templates — from product roadmaps to aftermarket channel plays — enabling teams to convert insight into 12–24 month action plans.

The market trajectory we quantify is neither hyper‑growth nor stagnation; it is steady and transitionary. After rising through the historical period, total industry revenue shows continued expansion in the near term before stabilizing towards the end of the forecast window. This pattern speaks to two simultaneous dynamics: continued appetite for performance and torque‑enhancement solutions in targeted vehicle and industrial applications, coupled with mounting efficiency and emissions constraints that temper broad‑based substitution. For strategic planners, this means investment choices must be selective — targeting the high‑probability returns within an otherwise concentrated ecosystem.

Our competitive analysis profiles the spectrum of firms from heritage industrial manufacturers to dedicated aftermarket specialists. Leading legacy names — the original Roots blower manufacturer and large OEM suppliers operating at scale — dominate production volumes and OEM integration pathways. Specialist boutique firms and performance kit vendors maintain strong brand equity in racing and enthusiast channels, while component suppliers (e.g., clutch and precision‑machined parts providers) underpin reliability and compliance achievements.

Scale OEMs: Large suppliers with factory vehicle integration continue to wield advantages in unit economics and access to program awards. Their strategic emphasis is on platform‑level certification, cost optimization and integrated thermal/electronics pairing to meet regulator and OEM cycles.

Specialist performance firms: Companies focused on motorsport and aftermarket kits sustain strong margins through brand, bespoke engineering, and high‑value upgrades — an attractive segment for higher margins despite smaller absolute volumes.

Component specialists and Tier‑partners: Suppliers producing clutch systems, machined rotors, and precision housings are pivotal for durability and emissions testing. Their certification credentials and quality management systems are decisive in OEM selection processes.

Recent product activity underscores these positions. Specialist performance houses have continued to introduce high‑power kits for mainstream trucks and muscle cars, while OEM‑scale suppliers maintain program wins through platform insertions and volume supply agreements. Such dynamics create a two‑track market: volume‑driven OEM supply and premium aftermarket performance — each requiring different go‑to‑market models and investment profiles.

Two external forces shape near‑term strategy: regulation and raw‑material/manufacturing realities. Stringent emissions regimes place a premium on designs that deliver improved thermal efficiency and lower parasitic losses. At the same time, production depends on high‑precision castings and advanced materials to maintain reliability under high RPMs. Industry quality standards and certifications are an operational gating item for OEM programs, and compliance pathways add timelines and cost. Finally, persistent consumer preferences in certain segments — immediate throttle response, distinctive auditory character, and low‑end torque — sustain demand for Roots‑type solutions despite electrification trends in other vehicle classes.

The report is structured to be directly operational for 2026 planning cycles. Highlights include:

Market sizing and top‑line forecasts for 2026–2032, with sensitivity scenarios that reflect alternative regulatory and raw‑material cost paths.

Comprehensive competitive profiles and benchmarked scorecards for leading players and specialized vendors, including capabilities maps and likely program trajectories.

Segment‑level strategic frameworks (product architecture, OEM vs aftermarket GTM, and channel economics) that translate market dynamics into P&L impact models and margin expectations.

Supply‑chain and manufacturing diagnostics — critical path mapping for castings, rotors, gears, and clutch assemblies, plus recommended risk mitigations for single‑source dependencies.

Regulatory impact assessment and roadmap for emissions testing and certification, aligning product roadmaps with Euro 7 and CAFE compliance windows.

M&A and partnership playbooks: screening criteria, integration checklists, and financial sizing templates for bolt‑on versus transformational acquisition strategies.

Commercial tactics for aftermarket and brand channels, including pricing ladders, certification labeling, and dealer network rollouts tailored for 2026 campaigns.

For OEM suppliers: prioritize programs that embed emissions‑appropriate enhancements — pursue modular designs that can be validated across related engine families to maximize ROI on certification spend.

For aftermarket brands: focus investments on compliance documentation and accessory ecosystems (intake, intercooler, ECU calibration) to convert enthusiast demand into rapidly scalable, SOP‑ready packages.

For component suppliers and manufacturers: accelerate investments in precision machining capacity and materials substitutes that preserve performance while reducing weight and improving thermal characteristics.

For investors and M&A teams: target niche engineering houses with deep performance IP or suppliers with certified production processes — the market’s concentration metrics indicate attractive consolidation opportunities, but timing is critical to capture synergies before regulatory costs bite.

Across the board: embed regulatory scenario analysis into product and capital planning cycles. Early certification and co‑funding arrangements with OEMs can shorten time‑to‑market and create durable competitive barriers.

Our methodology combines bottom‑up revenue build, primary interviews across OEMs, performance houses and Tier suppliers, and a validated set of industry inputs on material costs, machining capacity and compliance timelines. We do not publish selective segmentation figures in this release; instead, the report’s full dataset contains the granular regional, product and application splits necessary for target selection, pricing strategy and capacity planning. Those detailed segment tables and company‑level unit economics are accessible through the full report page and are structured to plug directly into financial models and strategic roadmaps.

For organizations making resource allocation decisions in 2026, the Roots superchargers market presents both risk and reward: steady aggregate growth (CAGR 3.42% through 2032) coupled with concentrated competition and increasing regulatory complexity. The strategic challenge is to choose where to compete — high‑volume OEM programs that demand scale and certification, or high‑margin aftermarket and racing channels that demand speed and brand equity — and then to align engineering, manufacturing, and commercial investments to that choice. PW Consulting’s Roots Superchargers Market report is designed to make those tradeoffs transparent and actionable.

To review the full dataset, detailed segment breakouts, and the operational playbooks that support near‑term and medium‑term execution, visit PW Consulting’s report page and download the complete study. The full report contains the granular figures and templates teams need to convert the 2026 planning cycle into measurable market outcomes.

For detailed analysis of this topic, please visit the official page:Roots Superchargers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com