How Industrial MRO Supplies Help Reduce Equipment Downtime

Other |

2026-06-18 07:55:03

As organizations race to embed intelligence outside the cloud, edge computing chips have emerged as a decisive battleground for performance, latency, power efficiency, and sovereignty. PW Consulting’s new market research brief—based on a 2020–2025 historical base and a 2026–2032 forecast—synthesizes commercial, technical, regulatory, and supply-chain forces that will shape procurement, architecture, and M&A decisions through 2026 and beyond.

Edge Computing Chips Market

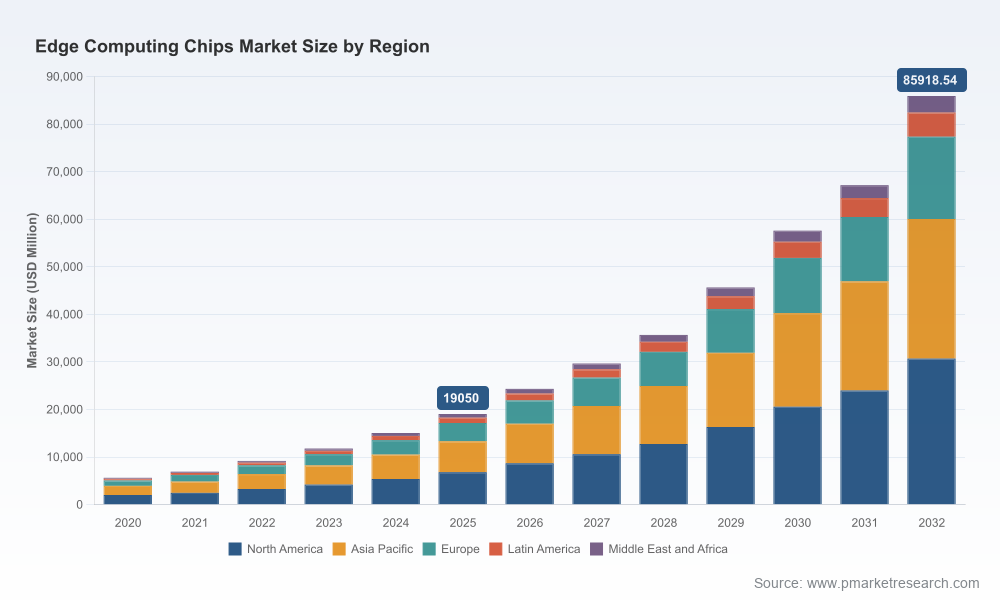

Our analysis finds the edge computing chips market reached a multi-billion-dollar scale by 2025 and is poised for rapid expansion in 2026 and the following years. The forecast baseline uses 2025 as a reference point and projects a compound annual growth rate (CAGR) of approximately 24.0% across the 2026–2032 window. This trajectory reflects compounded adoption across industrial automation, automotive systems, consumer devices, healthcare, and smart infrastructure where latency, privacy, and cost of connectivity favor on-device processing.

Edge Computing Chips Market

For corporate strategists, the headline implications are clear: engineering roadmaps and procurement calendars that assume incremental, linear growth will be outpaced by reality. Buyers must plan for step-changes in performance availability and concomitant pricing dynamics that will materially affect total cost of ownership (TCO) calculations, lifecycle support commitments, and retrofit strategies for installed bases.

Edge Computing Chips Market

These forces converge to make 2026 the year when strategy shifts from “evaluate” to “execute” for many enterprises. PW Consulting’s report synthesizes actionable pathways to align product roadmaps, procurement terms, and regulatory compliance to that execution window.

Our competitive analysis profiles incumbent silicon leaders and focused edge specialists. Global platform vendors continue to push integrated solutions that blend NPUs, GPUs, and platform services, while a set of focused startups and semiconductor design houses compete on ultra-low-power specialty processors and neuromorphic approaches.

Recent product and corporate moves through late 2025 and early 2026 illustrate how the battlefront is shifting. Notable developments include new edge-vision SoC launches optimized for multi‑stream video, capital raises and demonstrations of neuromorphic product families for ultra-low-power applications, and expanded IoT processor lines focused on secure, on-device inference. PW Consulting’s vendor scorecards evaluate each provider across performance, software ecosystem, roadmap cadence, and supply resilience—metrics that matter when negotiating platform lock-ins and long-term support agreements.

Regulatory adjustments—particularly changes to export control review policy affecting advanced computing chips—introduce a new layer of complexity for multinational sourcing. Starting in early 2026, case-by-case licensing and enhanced due diligence obligations for certain exports require procurement and legal teams to embed compliance checks into RFPs and partner contracts. Organizations must also consider the downstream impact on channel partners and software distributors who may become subject to the same regulatory frameworks.

Standards evolution is another critical axis. ISO 23247 and related frameworks for digital twins and industrial interoperability are accelerating edge adoption in manufacturing by enabling localized data processing and deterministic analytics. For technology and operations leaders, aligning edge compute choices with standards roadmaps reduces integration cost and protects against stranded assets.

On the supply side, advanced packaging and High-Bandwidth Memory capacity are the primary bottlenecks that are already constraining delivery of the highest-performance edge components. This dynamic favors architectural strategies that prioritize scalable compute at the mid-tier performance points and modular upgrade paths for flagship deployments.

PW Consulting’s full report is structured to be immediately operational for CIOs, CTOs, procurement heads, and corporate development teams. Key deliverables include:

To uphold the “preview” principle, the report intentionally withholds granular segment tables and proprietary split-level datapoints in this public summary. Full segmentation, vendor-specific benchmarking figures, and downloadable models are available through our client portal.

PW Consulting models three practical scenarios that organizations must triangulate against strategic choices:

Our proprietary scenario model quantifies revenue and procurement impacts under each path and maps recommended tactics for program managers, procurement, and corporate development teams.

The edge computing chips market in 2026 presents both an opportunity and a governance challenge. With a multi-billion-dollar base and a high-teens-to-mid-twenties CAGR in the near term, investments made in the next 12 months will disproportionately influence product roadmaps, partner ecosystems, and competitive positioning through the rest of the decade.

PW Consulting’s full report provides the granular segmentation, vendor benchmarking, and financial models required to convert this strategic preview into executable plans. For procurement teams, engineering leaders, and corporate strategists seeking to reduce risk, accelerate time-to-market, and optimize TCO, the report is designed as a working tool—complete with calculators, contract language, and rapid-deployment checklists.

To access the complete dataset, vendor-level benchmarks, and downloadable scenario models, visit the official PW Consulting publication page. Our analysts are available for briefings and bespoke advisory engagements to translate the findings into procurement RFPs, product roadmap decisions, and M&A diligence packages.

Disclaimer: This preview highlights high-level market dynamics and selected competitive developments. Detailed segment-level tables, confidential vendor scores, and downloadable forecasting models are reserved for report purchasers and subscribers.

For detailed analysis of this topic, please visit the official page:Edge Computing Chips Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com