Automotive Transfer Case Market: Trends and Growth Opportunities

Other |

2026-04-01 11:17:21

PW Consulting’s latest industry briefing on the Fruit Jam, Jelly and Preserves market synthesizes five years of historical performance with a seven‑year outlook to arm executives with the foresight necessary for high‑stakes 2026 decisions. Built on a 2025 base year and a forecast horizon through 2032, the report combines a granular view of commercial dynamics with actionable growth and cost‑containment playbooks — while reserving detailed segment and regional datasets for the full report.

Fruit Jam Jelly And Preserves Market

The global market has demonstrated steady expansion through the early 2020s, with PW Consulting’s topline model estimating the overall market at USD 9,530 Million in 2025. Under a central scenario the category is projected to grow at a compound annual growth rate (CAGR) of 3.2% over the 2026–2032 forecast period, reaching approximately USD 11,880 Million by 2032.

Fruit Jam Jelly And Preserves Market

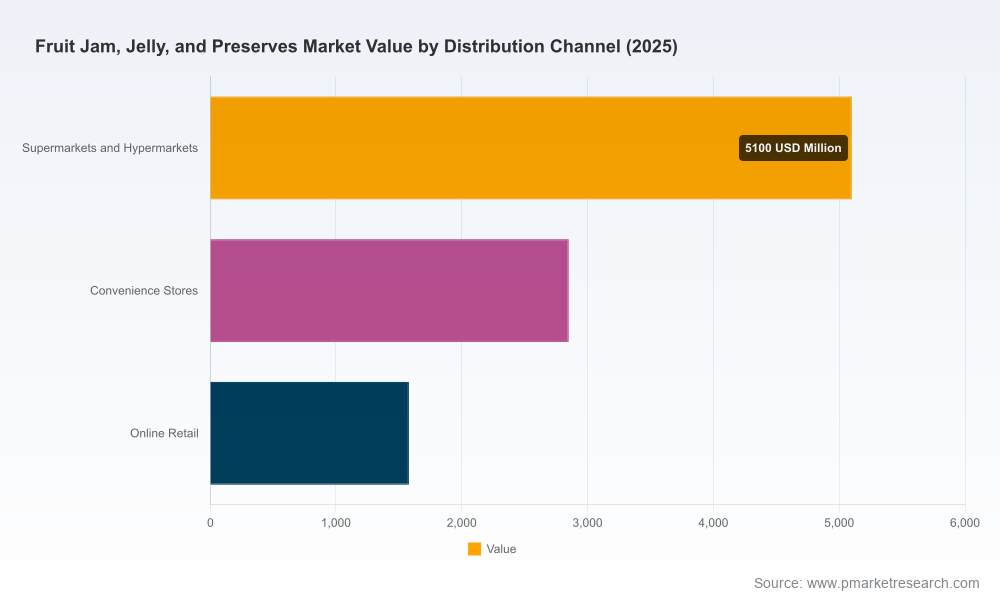

That trajectory masks heterogeneity by channel, formulation and geography: premium and reduced‑sugar innovations are accelerating faster than legacy mainstream SKUs; convenience formats and e‑commerce continue to outpace slower traditional grocery channels; and volatility in ingredient costs is compressing margins for firms that lack integrated procurement or hedging strategies. For 2026 planning horizons, this combination of modest topline growth and heightened margin pressure makes portfolio optimization and operating resilience the highest‑priority levers.

Fruit Jam Jelly And Preserves Market

Each of the above is backed by scenario models covering historical years 2020–2025 and forward projections to 2032, enabling planners to stress‑test budgets and capital allocation under alternative macro and commodity pathways.

The category exhibits moderate concentration: our market share analysis shows the top three players account for a meaningful but not dominant portion of global sales, with the five‑player concentration reflecting a landscape where national champions and premium specialists coexist. From a corporate strategy perspective, this structure favors both differentiated brand plays and consolidation aimed at scale economics.

Recent corporate developments further illustrate the strategic themes shaping 2026 choices:

PW Consulting’s competitive chapter synthesizes these moves into a playbook that helps buyers, sellers and incumbents evaluate valuation premia, integration risks and the operating matrices necessary to extract synergies post‑transaction.

Raw material dynamics are central to 2026 planning. Producer price indexes for canned fruit and preserve inputs and contemporaneous industry data point to notable cost pressure through 2025 and into 2026 — our models reference a marked uptick in indexed input costs in the spring of 2026 that materially affected producer margins. Independent industry measures indicate production cost inflation that has approached double‑digit levels year‑over‑year in the most challenged geographies, driven by fruit yields, sugar price swings and logistics constraints.

Two operational implications follow:

On the regulatory front, evolving label and standards discussions — including debate around standards of identity for sweetened and artificially‑sweetened spreads — create both risk and opportunity. Labels that enable nutrient content claims can unlock new consumer segments, but require careful nutritional strategy and claims substantiation if brands are to avoid trade and retail complications.

Three innovation themes dominate near‑term product success:

PW Consulting’s product playbook maps each innovation theme to go‑to‑market templates, expected promotional loads, margin sensitivities and manufacturing adjustments required to scale.

Beyond headline numbers, the report is structured to deliver executable outputs for 2026 leadership cycles:

To preserve commercial value and ensure candid analyst recommendations for executive clients, detailed segment and regional datasets (including cell‑level forecasts by type, distribution channel and geography) are available exclusively in the full PW Consulting report and data package.

The Fruit Jam, Jelly and Preserves market is at an inflection point: steady aggregate growth masks shifting demand patterns, rising input cost volatility, and an innovation race centered on health‑forward claims and convenience formats. For leaders planning 2026 budgets and strategic moves, the imperative is clear — protect margins through procurement and formulation agility, capture growth via targeted innovation and channel playbooks, and use M&A selectively to secure capabilities and consolidate scale.

PW Consulting’s full report equips management teams with the market models, operational templates and deal playbooks required to execute those choices with confidence. For a complete breakdown of segment projections, regional performance and the detailed data tables that underpin our recommendations, please access the full report and downloadable datasets via the PW Consulting report page.

For detailed analysis of this topic, please visit the official page:Fruit Jam Jelly And Preserves Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com