Global Expansion Strategies in Pharmaceutical Product Tester Market Research

Other |

2026-04-03 08:37:36

As pimple patches transition from niche dermatological aids to mainstream skincare essentials, PW Consulting’s latest market study offers a concise, strategy-first briefing to inform boardroom choices in 2026. This preview distills the report’s most consequential, decision-ready insights while preserving the proprietary segment detail that we hold for subscribers. Below you will find the macro trajectory, competitive cues, regulatory inflection points and a prioritized playbook for executives planning product, manufacturing and channel moves over the next 12–24 months.

Pimple Patches Market

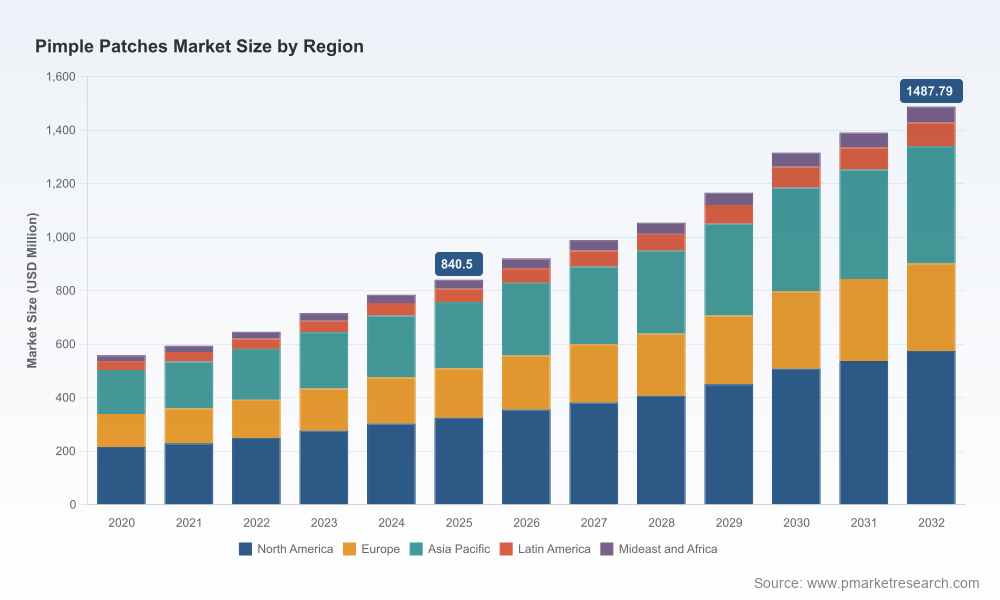

Historical and base-year framing: Our analysis covers 2020–2025 with 2025 as the base year for planning. The pimple patches market expanded steadily through the historical period, reflecting broadening consumer acceptance, improved product formats and faster route-to-consumer via digital channels.

Pimple Patches Market

Scale and growth: The market recorded a mid‑single‑digit to high‑single‑digit expansion during the historical window and enters the forecast cycle (2026–2032) with an expected compound annual growth rate (CAGR) of approximately 8.5%. On an absolute basis, the market crossed the high‑hundreds of millions (USD) mark in our base year and is forecast to approach the low‑single‑billion range by the end of the 2032 horizon.

Pimple Patches Market

Near‑term inflection: The first forecast year (2026) in our model shows measurable uplift versus base year demand, driven by product innovation (microarray/microneedle variants), expanded private‑label manufacturing capacity and the continuing digitalization of distribution.

Timing and posture: 2026 will be a make‑or‑refine year for players positioning to capture the next phase of scale. With an ~8.5% CAGR baked into our base forecast, companies must choose between investing to grow share or optimizing margins as market dynamics shift.

Actionability: The report is oriented to executable choices rather than descriptive benchmarking. We provide scenario‑based financial models, product launch scorecards, contract manufacturer evaluation templates and go‑to‑market playbooks that translate market momentum into prioritized investments.

Regulatory and operational must‑haves: Practical checklists on device vs. cosmetic classifications, manufacturing registration, labelling language and claim substantiation are integrated into each strategic pathway — enabling teams to move from strategy to compliant implementation without rework.

Proprietary forecast model: Top‑line and product family scenarios across 2026–2032 (flexible inputs, downloadable). The model is stress‑tested across adoption, pricing and channel mix assumptions so leadership can run rapid sensitivity analyses for M&A, portfolio or capacity decisions.

Go‑to‑market playbooks: Channel segmentation playbooks tailored to direct‑to‑consumer, pure e‑commerce partnerships, specialty retail and private label. Each playbook pairs spend levers with expected ROI timeframes and tactical KPIs.

Manufacturing & sourcing toolkit: OEM/ODM evaluation matrix, sample RFP language, short‑list methodology and unit‑cost benchmarking to aid near‑term sourcing swaps and multi‑sourcing designs that mitigate hydrocolloid raw‑material risk.

Regulatory roadmaps: Country‑level decision trees that differentiate cosmetic vs. medical device pathways, registration timelines, and capability gaps to address for product claims or active ingredients.

Innovation radar & IP yardstick: Technology briefings on microneedles, multi‑phase antibacterial arrays and advanced absorptive matrices — with an assessment of commercial readiness, likely pricing bands and white‑space opportunities.

Consumer incumbents: Hero Cosmetics and COSRX continue to anchor consumer awareness with recognizable formats and distribution footprints. Their strength is in brand trust and retail placement, making them primary comparators for any product aiming at mass FMCG channels.

Brand differentiation through design: Starface has shown the marketing power of design‑forward positioning, turning treatment patches into a visible brand expression. For marketing teams, Starface underscores the value of category‑stretching creativity to extend price realization and earned media.

Science‑led providers: ZitSticka illustrates how technology‑first positioning (microneedle and targeted applications) commands premium shelf space and can change usage patterns. Technology differentiation remains a sustainable route to higher ASPs and specialty distribution.

Clean and clinical positioning: Rael, Peace Out and dermatology line extensions from brands such as Peter Thomas Roth occupy adjacent premium and dermatologist‑recommended channels. Their playbook is useful for firms seeking to trade up consumers or enter clinical pathways.

Manufacturing backbone: OEM/ODM specialists (DERMATECH, Lessonia and similar regional manufacturers) remain strategic partners for rapid scale. Recent announcements show capacity investments and geographic specialization that shorten lead times and enable private label growth.

Product innovation: Academic advances toward dual‑phase antibacterial and anti‑inflammatory microarrays indicate that technological differentiation will accelerate product lifecycle turnover — creating windows for first‑mover premium capture in core markets.

Manufacturing capacity shifts: European producers are expanding high‑spec hydrocolloid lines while OEMs are showcasing customizable patch platforms at trade events — both signs that supply options are improving for brands that need private‑label agility.

Regulatory clarity: Where treatment claims are made, patches are increasingly being processed under medical device registration regimes. This affects go‑to‑market timing and cost for players seeking to position products as therapeutic rather than purely cosmetic.

Regulatory gating: Companies that plan to market medicated patches must anticipate facility registration and device listing processes under applicable regulatory frameworks. Treat claim language and clinical evidence generation as early investment items.

Raw material concentration: Hydrocolloid films and adhesive systems are core inputs. Buyers should model inventory buffers and dual‑sourcing to insulate launches from episodic supply shocks.

Sustainability pressures: Consumer preference is favoring biodegradable matrices and recyclable packaging; brands that retrofit designs to improve end‑of‑life characteristics can unlock distribution wins with sustainability‑focused retailers.

Channel friction: Online channels continue to compress the time from launch to scale, but profitable customer acquisition requires disciplined unit economics and retention playbooks.

Competitive fragmentation: The category displays moderate concentration — several national and international brands hold meaningful shares, but there remains ample space for differentiated entrants and private label growth.

Decide product posture: Define whether you compete on mass convenience, clinical efficacy or design‑led differentiation. Each posture drives different R&D, pricing and channel needs.

Advance regulatory readiness now: If you intend to make therapeutic claims, initiate device registration and facility audits immediately. The lead time for compliant manufacturing and labelling updates can erode launch windows if started late.

Lock in supply options: Negotiate minimum‑viable contracts with OEMs for scale flexibility, include raw‑material pass‑through scenarios and secure dual‑sourcing where possible.

Invest selectively in tech differentiation: Target one innovation vector (e.g., microneedle delivery or antibacterial arrays) and align marketing and pricing strategies to protect margin while proving consumer willingness to pay.

Operationalize sustainability: Set measurable packaging and material targets for 2027 launches; secure supplier commitments to support claims and retailer approvals.

Use acquisition as an accelerator: Prioritize tuck‑ins that provide manufacturing capacity, IP around delivery technology or regional distribution access — not just incremental revenue.

Custom modelling: We will configure the full 2026–2032 forecast model to reflect your SKU economics, channel mix and market-entry timing so you can evaluate capex and working capital implications instantly.

Due diligence & buy‑side advisory: Rapid vendor scorecards for OEM/ODM partners, IP landscape scans and regulatory gap analysis to shorten negotiation cycles.

Go‑to‑market execution support: From pilot playbooks for DTC launches to retail listing negotiation tactics and trade spend optimization.

To maintain the integrity and commercial value of our analysis, this preview omits the granular regional, material and channel split tables and the full vendor scorecards. Subscribers to the full PW Consulting Pimple Patches Market Report receive downloadable Excel models, segmented five‑year forecasts, SKU‑level pricing matrices and an annotated list of supplier contacts. Visit our report page to access the complete dataset, scenario tools and implementation templates that will convert the 2026 opportunity into measurable growth.

For detailed analysis of this topic, please visit the official page:Pimple Patches Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com