Flare Monitoring Market Overview: Key Drivers and Challenges

Other |

2026-04-15 04:58:46

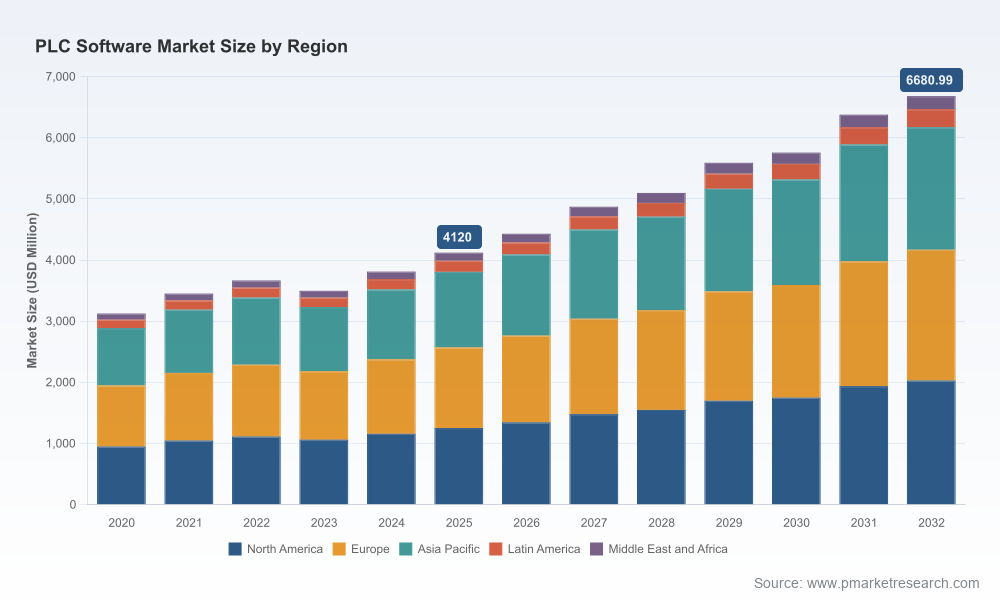

PW Consulting today publishes an executive preview of its forthcoming Plc Software Market research report, prepared to inform boardroom and executive-level decisions throughout 2026. Built on a five‑year historical baseline (2020–2025) and a seven‑year forecast window (2026–2032), the study synthesizes commercial, technical, regulatory, and security dynamics shaping programmable logic controller (PLC) software and associated engineering ecosystems. The global market reached approximately USD 4,120 Million in our base year (2025) and is forecast to grow at a compound annual growth rate (CAGR) of 7.15% across 2026–2032, reflecting sustained modernization and software‑led productivity initiatives across industrial sectors.

Plc Software Market

Strategic timing — Automation roadmaps and capital planning cycles in many enterprises kick off in Q1 and Q2 of each fiscal year. This report is designed to influence budget allocation, platform rationalization, and partner selection as organizations set priorities for 2026.

Plc Software Market

Decision fidelity — Our approach combines primary interviews with engineering and OT leaders, vendor product mapping, and scenario stress‑testing. The result: recommendations that bridge engineering tradeoffs and C‑suite imperatives without abstruse academic models.

Plc Software Market

Risk‑aware growth — Growth prospects are robust, but they sit alongside heightened regulatory scrutiny and OT cyber risk. The report quantifies these tensions and provides pragmatic mitigations executives can operationalize.

Market sizing and high‑level trend arcs: concise macro figures and an interpretive narrative to anchor strategic planning.

Vendor landscape and competitive positioning: qualitative profiles, product strengths, engineering differentiators, and tactical implications for procurement and partnership strategies.

Technology value maps: trade‑off matrices for cloud vs. on‑prem engineering, PC‑based control vs. dedicated controllers, and the role of GenAI‑assisted engineering tools.

Security and regulatory playbooks: compliance checkpoints, technology controls, and organizational measures to satisfy new data and automated‑decision regulations while protecting OT assets.

Actionable procurement frameworks: RFP templates, evaluation scorecards, and total cost of ownership (TCO) models tailored to both greenfield and brownfield modernization.

Executive‑level scenario planning: upside/baseline/downside cases with sensitivity to innovation adoption rates, regulatory changes, and major cyber incidents.

Operational toolkits: migration roadmaps, pilot design briefs, and KPIs for measuring engineering productivity, uptime, and security posture.

Enterprise leaders typically grapple with three interdependent questions: where to invest to generate measurable operational value, how to protect increasingly software‑defined control systems, and who to partner with for long‑term resilience. Our analysis transforms these questions into executable choices.

CIOs and CTOs gain a prioritized set of platform bets — for example, where GenAI‑assisted code generation and integrated engineering suites can reduce cycle times and where legacy lock‑in should be avoided to preserve flexibility.

COOs and plant directors get migration playbooks that align modernization with production windows and quality gates, minimizing both disruption and hidden costs in brownfield sites.

CISOs receive a mapped set of controls and procurement clauses to make OT vendors contractually accountable for vulnerability management, secure build pipelines, and incident reporting obligations that reflect recent regulatory trends.

Corporate development and investors obtain a defensible view of consolidation dynamics, including where software‑first entrants and platform players could create acquisition opportunities or competitive threats.

The PLC software arena is characterized by a mix of long‑established industrial software suites, platform players enabling multi‑vendor ecosystems, and fast‑moving software innovators. The market displays notable concentration at the top, with the leading vendors commanding a majority share — a dynamic that favors deep integration but also creates whitespace for niche and software‑centric challengers.

Legacy industrial integrators and engineering suites continue to dominate where customers demand end‑to‑end automation stacks and proven industrial support. Their strengths include integrated simulation, motion control, and extensive vendor ecosystems.

Platform and software‑centric players (including open IDE providers and PC‑based control suppliers) are expanding through interoperability and developer‑friendly tooling, enabling faster prototyping and lower barriers for software‑led automation projects.

New entrants emphasize modularity, security, and AI‑assisted engineering — features that accelerate engineering velocity but require disciplined lifecycle governance to deliver sustained value.

Notable vendor characteristics summarized for executive consideration:

Siemens — Integrated engineering platform with a breadth of controller support and emerging GenAI assistance; compelling for enterprises committing to vendor‑level digitalization strategies.

Rockwell Automation — North America‑centric strengths in ecosystem networking and tightly integrated software/hardware stacks; advantageous where EtherNet/IP and facility‑level integration matter.

Schneider Electric — Strong alignment with energy management and IEC‑centric programming; valuable for customers with combined automation and energy optimization objectives.

Mitsubishi Electric — High‑performance control focus, relevant for precision manufacturing and semiconductor/automotive lines where cycle time and determinism are critical.

Beckhoff — PC‑based control and next‑generation runtime innovation that appeals to organizations pursuing software‑defined automation and consolidated compute platforms.

ABB and CODESYS — Flexible, standards‑aligned development environments that facilitate multi‑vendor deployments and reduce hardware lock‑in.

Two regulatory developments and an intensifying threat landscape are altering vendor selection and architecture choices. New rules addressing automated decision‑making and obligations for handling bulk sensitive data have raised the compliance bar for automation software providers and their customers. Concurrently, high‑impact PLC vulnerabilities and OT breaches have made vulnerability management and secure engineering a non‑negotiable requirement.

Compliance: Enterprises must now consider privacy and algorithmic accountability obligations in their procurement and deployment of engineering tools that incorporate automated decision logic.

Security: Product roadmaps and SLAs must incorporate continuous vulnerability scanning, secure update pipelines, and verifiable incident response commitments for PLC ecosystems.

Third‑party risk: Suppliers of auxiliary engineering tools (version control, simulation, AI assistants) should be subjected to the same diligence as core control‑system vendors.

AI‑first engineering tool launches demonstrate vendor investment in developer productivity features, such as code analysis, security gates, and automated test scaffolding — all of which change the cost profile of automation projects.

Open and multi‑vendor updates emphasize lifecycle management and remote operations capabilities, reflecting the need for scalable field maintenance and reduced mean time to repair.

Vendor milestones and product anniversaries underscore maturation of PC‑based runtimes and the transition of control logic from proprietary stacks toward more software‑centric architectures.

Initiate an executive briefing: align C‑suite priorities around automation outcomes, TCO horizons, and acceptable security risk thresholds.

Map your installed base: create an asset and software inventory that includes firmware versions, supported toolchains, and third‑party components.

Prioritize modernization use cases: select 1–2 high‑impact pilot sites that capture productivity gains and lower operational risk.

Embed security and compliance gates into procurement: require vulnerability disclosure timelines, secure update mechanisms, and compliance attestations.

Vet AI and automation assistants carefully: pilot for productivity gains but demand explainability, version control, and rollback capability.

Establish a vendor‑agnostic integration layer: reduce lock‑in by standardizing on interoperable protocols and runtime APIs where possible.

Use M&A and partnership scouting selectively: target capabilities that shorten time‑to‑value (e.g., lifecycle management, secure build pipelines, simulation‑as‑a‑service).

Measure outcomes rigorously: track engineering cycle time, deployment frequency, OT incident rate, and cost per control‑loop as primary KPIs.

This preview is intentionally selective. The full Plc Software Market report contains the detailed segmentation, downloadable financial models, vendor scorecards, and scenario analyses that enterprise teams require to execute with confidence. PW Consulting’s full report expands each of the strategic levers summarized above into executable work streams, including a configurable RFP template and a vendor evaluation toolset tailored to your operational and regulatory context.

To schedule a tailored briefing, request a sample chapter, or license the full report and model packages, contact PW Consulting. The full analysis is the definitive resource for boards, CTOs, CISOs, and automation executives preparing capital and technology plans for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Plc Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com