Common Myths About Skin Lesion Removal Debunked

Health |

2026-05-25 14:14:21

PW Consulting’s new Submarine AIP System Market report (base year 2025, historical 2020–2025, forecast 2026–2032) translates evolving technology, supply-chain fragility and rising geopolitical demand into an actionable decision framework for defense leaders and marine industrialists. The market we track has grown from the low hundreds of millions (USD, million-unit reporting) in 2020 to an estimated USD 392.21 million in 2025, and our scenario-driven modelling projects continued expansion through the forecast window — approaching a half‑billion dollars by the end of 2032 at a mid-single-digit compound annual growth rate (CAGR ~3.8% for the 2026–2032 forecast period). Crucially for 2026 procurement cycles, this is a market that is consolidating in capability even as it fragments in supplier and technological approaches — and the strategic choices made this year will shape platform competitiveness for a decade.

Submarine Aip System Market

From procurement timing to technology lock‑in: our analysis isolates the inflection points where selecting a specific AIP technology or supplier imposes multi‑year constraints on platform maintenance, logistics and exportability.

Submarine Aip System Market

Cost‑to-operate realism: we translate prototype and demonstration cost claims into program-level lifecycle scenarios that reflect raw‑material volatility (notably hydrogen storage and oxygen supply systems) and sanctions‑driven material upstream risks.

Submarine Aip System Market

Strategic interoperability: for navies balancing domestic sovereignty with allied interoperability, we map the tradeoffs between indigenous AIP integration and off‑the‑shelf systems, with practical timelines for refits, crew training, and supply‑chain development.

M&A and partnership plays: the market concentration metrics show a sector where the top three players account for a majority share and the top five approach deep industry concentration. That structure generates specific opportunities — and barriers — for new entrants, tier‑2 suppliers and cross‑sector technology licensors.

Executive decision matrix: a procurement-focused playbook that aligns mission profiles (endurance vs stealth vs maintainability) with AIP technology families and supplier archetypes.

Scenario cost models: three lifecycle cost scenarios per platform type (conservative, baseline, accelerated adoption) that incorporate capital expenditure, mid-life refit windows and projected raw material swings.

Technology readiness and risk heatmaps: evaluated across integration complexity, maintainability, safety envelope and export control exposure for every major technology pathway.

Supplier diligence toolkit: a standardized scorecard for capability, financial strength, intellectual property stance and export compliance — calibrated for defense acquisition authorities.

Operational integration playbooks: timelines and resource estimates for new-build integration, retrofits and phased fleet upgrades, including crew training and shore support requirements.

Policy and geopolitics annex: impact assessment of trade restrictions, sanctions and national industrial policy programs — with mitigation options

Opportunity maps: prioritized M&A, JV and technology licensing opportunities for primes, subsystem suppliers and investors — ranked by strategic fit and time to revenue.

The sector is being shaped by three converging forces. First, operational demand: navies continue to emphasize submerged endurance and acoustic discretion, sustaining demand for AIP upgrades as a relatively lower‑cost way to extend patrol effectiveness without moving immediately to full‑battery or air‑independent hybrid solutions. Second, supply‑side consolidation: our concentration analysis indicates a materially concentrated supplier base — the top three firms capture a majority share, and the top five account for nearly seven out of ten market units — which favors established primes in program wins but also creates counterparty risk for buyers seeking diversified supply. Third, raw materials and regulatory noise: the combined effects of sanctions, specialized material requirements (e.g., high‑performance metals, hydrogen storage media) and evolving domestic defense industrial policies are increasing both unit production cost and delivery uncertainty — a critical input when modeling acquisition timelines in 2026.

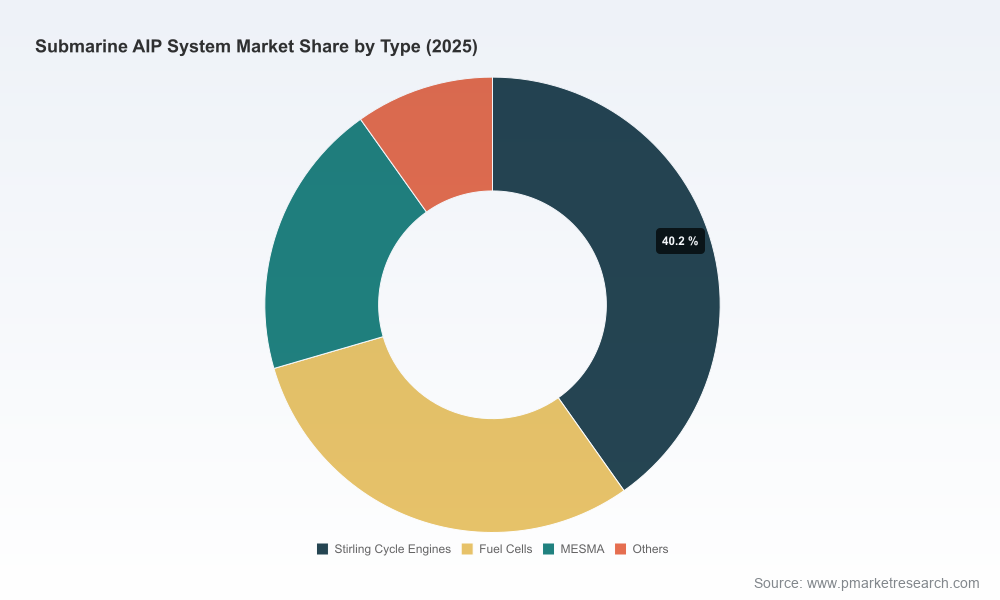

Saab AB (Kockums): a recognized leader in Stirling‑based AIP, prized for low acoustic signature and mature integration on specific classes. Their value proposition in 2026 is proven quiet endurance and platform integration experience — strengths that matter where stealth trumps absolute endurance.

thyssenkrupp Marine Systems (TKMS) and Siemens AG: TKMS, frequently partnered with Siemens for PEM fuel cells, offers a pragmatic pathway for navies seeking modular, scalable fuel‑cell AIP with established industrial support networks. Recent program awards underscore continued demand for PEM‑based approaches.

Naval Group: advancing both MESMA and second‑generation fuel‑cell concepts alongside onboard hydrogen production (diesel reforming). Their multi‑track strategy hedges risk and appeals to programs prioritizing sovereign manufacturing and alternative fuel logistics.

Hanwha Ocean: an emerging force integrating hybrid AIP architectures into new platforms. Their export design approvals and recent launches signal competitive ambitions in regional markets, particularly where shipbuilders bundle platform and AIP capabilities.

Navantia: pursuing bioethanol‑based processing routes, offering a distinctive solution for countries seeking less complex hydrogen logistics at the cost of additional processing subsystems.

China Shipbuilding Industry Corporation (CSIC): domestically focused, CSIC continues to field indigenous AIP variants and remains a major factor in regional capability dynamics.

Recent program moves are instructive. 2025–2026 announcements — including new hull launches with hybrid AIP, export design approvals and integration milestones for indigenous systems — show that both prime systems and national programs are moving from pilot phases into formal fleet adoption and refit cycles. For 2026 planning, this raises two practical imperatives: (1) anticipate accelerated port availability pressure as refit windows open, and (2) embed supplier contingency plans where single‑source dependencies exist.

Supply‑chain shocks: sanctions and export controls can create sudden shortages of critical metals and specialized components. Mitigation: dual‑source component strategies, verified alternate material specifications, and early contracting for long‑lead items.

Technology lock‑in: committing to a single AIP family without integration flexibility can result in rapid obsolescence as fuel‑cell and storage tech evolve. Mitigation: modular interfaces, open architecture contracts, and staged capability blocks allowing upgrades.

Operational training shortfall: AIP systems alter submarine logistics and shore support needs. Mitigation: invest in shore‑based simulators and bilateral training partnerships timed to refit milestones.

Lifecycle cost escalation: hydrogen storage and oxygen handling impose recurring technical and regulatory costs. Mitigation: insist on whole‑life costing in vendor proposals and reserve funding lines for mid‑life system replacements.

Start procurement with a modular architecture requirement: specify mechanical and electronic interfaces to permit phased fuel‑cell or Stirling replacements without full‑hull redesign.

Require supplier roadmaps and transition plans: demand clarity on upgrade paths, obsolescence risk and spare‑parts depth for at least 10 years post‑delivery.

Lock in raw‑material options early: include contract clauses for alternate material acceptance and price‑escalation caps for key inputs such as hydrogen storage media.

Structure deals for industrial collaboration: where sovereign capability is strategic, favor technology transfer, licencing or local manufacture clauses tied to performance milestones.

Insist on multi‑scenario cost modeling in bids: require vendors to submit conservative, baseline and accelerated lifetime cost projections, stress‑tested for supply shocks and refit delays.

Plan maintenance hubs: co‑locate AIP maintenance capacity in allied ports to reduce logistic tails and to support export maintenance requirements for partner navies.

The Submarine AIP market in 2026 is not a binary bet. The modest but steady growth we project — rising from approximately USD 392 million in 2025 to a materially larger market by 2032 at a 3.8% CAGR — reflects steady naval demand paired with incremental technology shifts. The smart strategic posture for procurement authorities and platform designers is to prioritize optionality: design for multiple AIP technologies, require transparent lifecycle economics, and build industrial partnerships that spread risk while preserving sovereignty where necessary.

PW Consulting’s full report provides the underlying datasets, granular supplier scoring, contract templates, and the scenario models needed to operationalize these recommendations. To access the detailed segmentation, country‑level procurement timelines and the supplier scorecards that we intentionally summarized here, please consult the full Submarine AIP System Market report and supporting annexes on our publication page.

For detailed analysis of this topic, please visit the official page:Submarine Aip System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com