Cenospheres Market Industry Evolution

Other |

2026-06-17 09:37:08

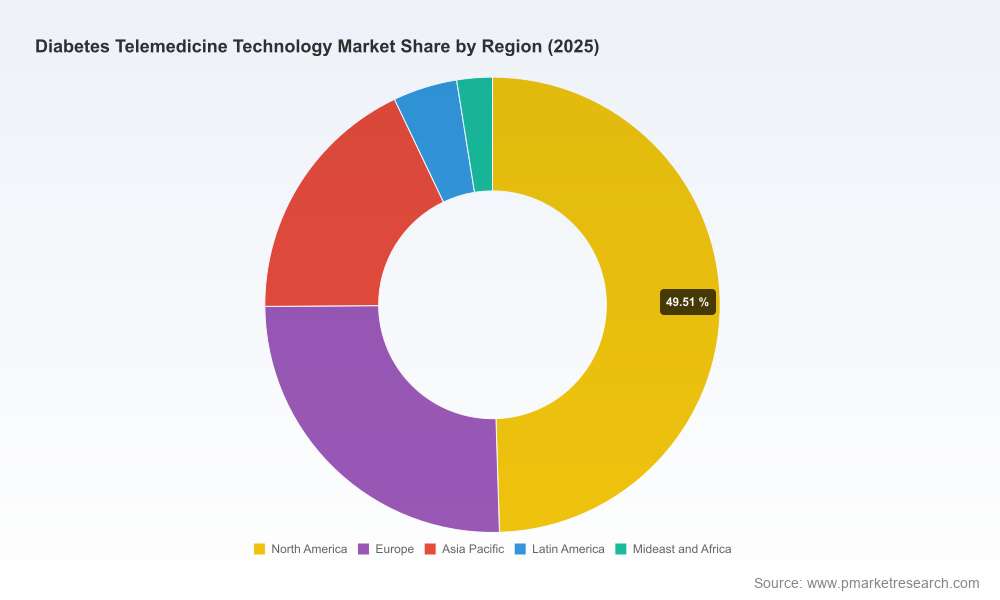

PW Consulting’s latest market study on Diabetes Telemedicine Technology outlines why 2026 is a make-or-break year for commercial strategy in a market expanding at a sustained double‑digit pace. The global market grew from roughly USD 3.0 billion in 2020 to about USD 5.65 billion in 2025 and—driven by accelerated device connectivity, payor policy shifts, and growing home‑based care—enters the forecast period with a compound annual growth rate (CAGR) of 13.5%. Our baseline shows the market crossing the USD 6.8 billion threshold in 2026 and continuing to expand toward the low double‑digit billions by the early 2030s.

Diabetes Telemedicine Technology Market

Policy momentum: Recent policy updates from CMS—in particular new RPM codes and extended telehealth flexibilities implemented in early 2026—materially change the economics of remote diabetes management. These changes create near‑term pathways to reimbursement for shorter monitoring intervals and broaden the set of billable remote diabetes self‑management services.

Diabetes Telemedicine Technology Market

Technology convergence: Continuous glucose monitoring (CGM), connected insulin delivery systems, and remote monitoring platforms are converging into integrated care pathways. Device manufacturers and software platforms that master interoperability will capture disproportionate share of the clinically valuable data flow.

Diabetes Telemedicine Technology Market

Shifting care settings: Growth in home healthcare and virtual chronic care models is forcing traditional hospital and clinic players to rethink delivery and contracting models—presenting opportunity for vendors to embed into care teams and payor value‑based arrangements.

Concentration and consolidation: Market concentration is meaningful—our analysis shows the top three players control a majority share and the top five capture well over two‑thirds of commercial value—making partnerships, co‑development, and selective M&A key strategic levers.

Actionable market sizing and scenario models calibrated to 2026 policy pathways. We provide management‑grade demand curves and sensitivity analyses that let commercial teams stress‑test investment cases under alternate reimbursement and adoption scenarios.

A reimbursement playbook: mapping of new RPM codes, telehealth flexibilities, and Medicare program changes into product design and billing workflows—plus step‑by‑step templates for pilot reimbursement capture.

Interoperability and integration framework: a prioritized list of integration use cases (EHRs, CGMs, pumps, and remote monitoring platforms) and an engineering cost/benefit matrix for API strategy and regulatory readiness.

Clinical evidence and outcomes roadmap: protocols for RWE studies and payer pilots that demonstrate cost‑avoidance (hospitalization and complication reduction), with sample statistical power calculations and time‑to‑evidence timelines tied to reimbursement milestones.

Commercial playbooks for payor and provider engagement: negotiating templates, KPIs for value‑based contracting, and a pilot design library (90–180 day pilots optimized for fast evaluation).

Competitive due diligence: vendor capability matrices, integration appetite assessments, and a short list of acquisition targets by capability (digital therapeutics, RPM analytics, peripheral diagnostics)—with the granular financial and revenue‑split data available in the full report.

The provider ecosystem is diverse and increasingly interdependent. Key strategic observations from our company analysis:

Glooko — Strength: platform‑level interoperability and device agnosticism. Implication: vendors should evaluate partnership models that leverage Glooko’s integrations to accelerate device support and EHR connectivity in payer pilots.

Teladoc Health (Livongo) — Strength: large consumer engagement footprint and coaching services. Implication: expect continued emphasis on integrated coaching + device bundles; enterprise buyers should negotiate data‑sharing and outcomes guarantees in any joint programs.

Podimetrics — Strength: differentiated RPM for foot‑care risk mitigation. Recent product expansion broadened remote monitoring to temperature, weight and balance (SmartMat+), opening cross‑sell opportunities with chronic wound and home‑care providers.

Virta Health — Strength: structured remote care programs focused on metabolic reversal. Implication: chronic care vendors should consider modular partnerships with DTx players like Virta to integrate nutrition and telecoaching components into bundled offerings.

Dexcom, Abbott, Medtronic — Strength: device incumbency with deep clinical validation. Notably, there was recent regulatory activity enabling tighter CGM–pump integration; these device firms are moving from pure hardware vendors to platform players with cloud data services—making them prime targets for strategic alliances or competitive disruption depending on your go‑to‑market strategy.

Regulatory and reimbursement milestones (e.g., continued CMS guidance, RPM code utilization patterns): these directly influence unit economics—companies should build dashboards to track indexed RPM claim volumes and PFS updates weekly through 2026.

Device interoperability approvals and commercial integrations (device × pump × platform): each announced integration materially reduces friction for telemedicine deployments and accelerates adoption.

Payer pilot outcomes and published RWE: early wins demonstrating reduced facility utilization are the most potent accelerants for national coverage decisions and value‑based contracts.

Design for reimbursement first: rework product features and monitoring windows to align with new RPM codes and DSMT opportunities. Billing complexity should be treated as a core product requirement.

Invest in rapid‑evidence generation: fund short, pragmatic trials with clearly staged outcomes tied to cost offsets; use these to negotiate shared‑savings pilots with risk‑bearing payers and health systems.

Prioritize integration over proprietary lock‑in: API‑first approaches and certified EHR connectors shorten sales cycles and increase the addressable market in enterprise deals.

Build flexible commercial structures: create modular pricing and outcome‑based clauses that allow for tiered rollouts (pilot → regional scale → national deployment).

Targeted M&A and partnerships: prioritize targets that close capability gaps—analytics to drive predictive insights, behavioral health integration, and home‑monitoring peripherals for complication prevention.

Operationalize privacy and cybersecurity: regulatory scrutiny on health data intensifies as devices proliferate; compliance is not a checkbox but a market differentiator.

Clients engaging PW Consulting receive a combination of strategic counsel and execution support:

Executive briefings that translate the report’s scenario models into board‑level investment decisions and 12–24 month operating plans.

Custom financial models that embed client cost structures, anticipated RPM reimbursement capture, and pilot‑to‑scale conversion rates—enabling transparent ROI timelines.

Vendor selection and negotiation support: RFP templates, SLA checklists, and recommended commercial terms tailored to telemedicine and device integration projects.

Implementation playbooks for payer pilots, provider integrations, and regulatory filings—designed to reduce time‑to‑revenue and surface early value metrics.

2026 is not merely another year on the calendar for diabetes telemedicine—it is when policy, product, and provider models converge to create durable commercial pathways. With the market growing at a 13.5% CAGR and clear early winners consolidating scale, the strategic choices made in 2026 will determine who captures the high‑margin, recurring value that accrues to integrated digital‑device‑care platforms.

To explore the full quantitative analysis, company profiles, and segmented demand models (including the granular revenue and share breakdowns that underpin our recommendations), access the PW Consulting report page or contact our advisory team for a tailored executive briefing.

For detailed analysis of this topic, please visit the official page:Diabetes Telemedicine Technology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com