Soy Milk Market 2026 Strategic Outlook: A PW Consulting Preview for Executive Decision‑Making

As plant‑based dairy continues its evolution from niche to mainstream, soy milk remains a critical pillar — mature in some markets, rapidly adapting in others. PW Consulting’s new Soy Milk Market study (base year 2025; forecast period 2026–2032) synthesizes five years of historical performance with scenario‑based forecasts to equip senior leaders with the foresight required for confident 2026 strategy-setting. This preview surfaces the strategic implications our analysis reveals while intentionally withholding granular segment tables and region/app percentage breakdowns: consider this a trailer designed to orient decisions and drive you to the full dataset for transaction‑grade detail.

Soy Milk Market

Headline market dynamics — what the numbers tell us

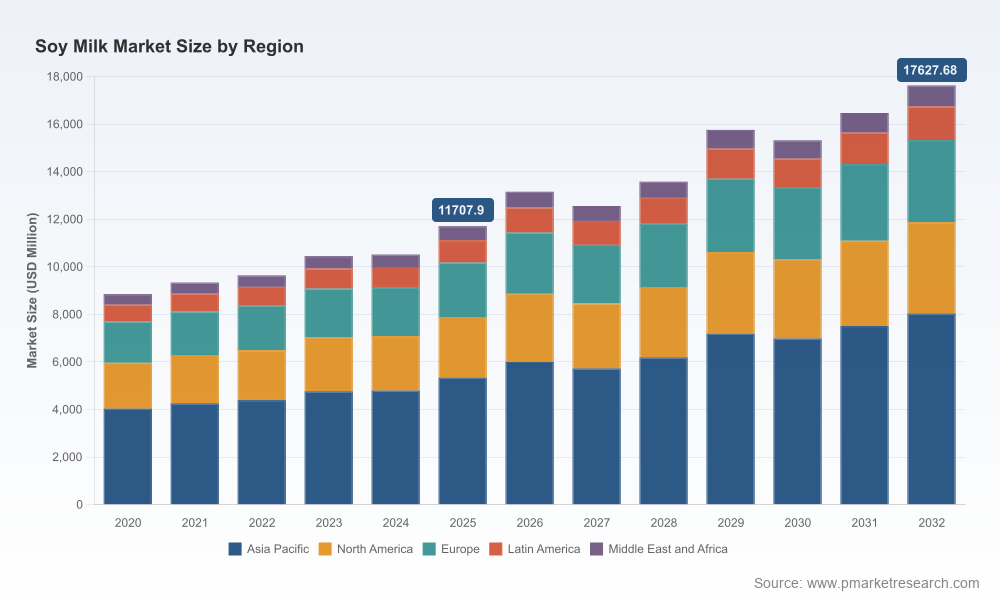

In aggregate terms, the soy milk market has demonstrated resilient growth through 2020–2025 and enters the 2026 planning window on a stronger footing. Our baseline model shows the market expanding from roughly USD 8.85 billion in 2020 to approximately USD 11.71 billion in 2025, and we project a continued compound annual growth rate (CAGR) of ~6.02% over the 2026–2032 forecast horizon. Under the base scenario, the market is on track to exceed USD 17.6 billion by 2032, with intermediate inflection points driven by product innovation, channel shifts and raw‑material price dynamics.

Soy Milk Market

Two structural drivers underlie this trajectory: first, the steady mainstreaming of plant‑based nutrition — where soy’s protein and familiarity keep it relevant — and second, iterative product innovation that spans ultra‑high‑protein formats to minimalist, clean‑label soy variants. These drivers interplay with cyclical supply‑side influences (soybean markets, vegetable oil dynamics) and policy/consumer health narratives, producing a growth curve that is robust but not immune to shocks.

Soy Milk Market

Strategic themes for 2026 planning

- Protein differentiation as a market lever. Recent launches — including refrigerated high‑protein formulations and clean‑label offerings — demonstrate that protein claims and formulation simplicity are primary axes for premiumization and retail space expansion. Expect accelerating SKU bifurcation between high‑protein/refrigerated propositions and staple shelf‑stable SKUs.

- Cost and margin pressure from raw materials. USDA forecasts and industry signals point to a tighter soy complex in recent seasons, with season‑average price revisions and modest global production shifts. These dynamics raise the strategic importance of procurement sophistication: indexed purchasing, forward hedging, and formula redesigns to protect margins without compromising positioning.

- Channel bifurcation: mainstream retail vs. digitally native pathways. Supermarkets and conventional retail continue to anchor volume, but online and DTC formats are accelerating product discovery, premium trial, and direct consumer data capture. Channel playbooks must allocate resources to both conversion‑weighted retail activity and digital brand building.

- Geography remains nuanced. Growth pockets persist where cultural familiarity, urbanization and retail modernization intersect. However, our preview purposefully refrains from publishing regional splits here — the full report contains the granularity you need to prioritize market entries, regional manufacturing footprints and trade flow optimizations.

- Competitive fragmentation offers both risk and M&A opportunity. Market concentration is mid‑range: the leading three and five players account for a meaningful share of market value, but the remainder remains populated by regional specialists and clean‑label challengers. That structure favors targeted roll‑ups, co‑pack alliances, and private‑label scalability plays in 2026.

What the PW Consulting report delivers — operational, transaction and go‑to‑market intelligence

Our full study is structured for immediate operational use and board‑level prioritization. Key deliverables include:

- Proprietary market model with annual revenues and scenario outputs (2020–2032), calibrated against observed sales runs and supply data; model exportable to client dashboards for bespoke sensitivity testing.

- Price‑and‑cost toolkit: raw material exposure analyses, a soybean price shock matrix, and margin preservation playbooks (formulation, pack/size optimization, supply contracts).

- Channel and SKU optimization matrix: frameworks for SKU rationalization, private‑label margin engineering, and a retailer negotiation checklist informed by modern category captains’ behaviors.

- Go‑to‑market blueprints for four strategic archetypes — Global Player Scale‑Up, Regional Champion, DTC Challenger and Private‑Label Manufacturer — with bespoke KPIs and 90‑day execution roadmaps.

- Competitive benchmark pack with strategy heatmaps for the major incumbents and emerging challengers, plus M&A screening filters that combine commercial fit, supply synergies and regulatory exposure.

- Supply‑chain stress test and a near‑term procurement playbook that aligns soy feedstock sourcing with processing capacity, alternative ingredient scenarios and biofuel demand impacts.

- Regulatory & labeling tracker with implications for protein claims, allergen communication and country‑specific plant‑based rules to inform packaging and compliance timelines.

Competitive landscape — actionable read on core players

The sector is characterized by a mix of global branded incumbents, regional champions and clean‑label disruptors. Our analysis centers on strategic posture, capability gaps and likely near‑term moves for the companies that matter:

- Danone S.A. (Silk, Alpro) — A global anchor with deep retail relationships and R&D muscle. Recent product steps into higher‑protein refrigerated formats demonstrate Danone’s push to reframe soy milk as a performance plus pleasure category. Expect continued investment behind premium refrigerated SKUs and brand partnerships to sustain volume growth in developed markets.

- Vitasoy International Holdings — Dominant in Asia, Vitasoy’s strength is distribution density and local product tailoring. Growth strategy will likely focus on new flavor formats and partnerships across foodservice and on‑the‑go channels where cultural adoption is strongest.

- Kikkoman Corporation — Traditionally known for soy sauce, Kikkoman’s food division is leveraging health narratives to expand soy milk relevance, particularly in smaller pack sizes and health‑oriented segments. Expect sustained marketing behind functional positioning and in‑store activations.

- Specialist organic and clean‑label brands (Eden Foods, WestSoy, MALK, Organic Valley, Califia Farms) — These players drive premiumization with minimalist ingredient lists and organic credentials. Califia’s recent entry with an 8g protein, three‑ingredient offering highlights a template incumbents may emulate: high‑clarity labeling coupled with protein messaging.

- Branded co‑packers and ingredient specialists (SunOpta, Pacific Foods, The Hain Celestial Group, American Soy Products) — These companies present flexible supply options for retailers seeking private‑label growth or quick category scale. Their strategic value lies in capacity, certification breadth and cost control.

Recent sector moves underscore these dynamics: high‑profile product launches in early 2026 signal that both innovation (high‑protein, clean label) and portfolio diversification (ready‑to‑consume bars, creamers) are front‑stage. These launches are not isolated; they align with companies’ broader attempts to monetize protein and simplicity narratives.

Supply and regulatory signals you cannot ignore

- Raw material volatility: USDA revisions in 2025/26 soybean price expectations and modest changes in global production introduce measurable input risk. Procurement sophistication and formula resilience will determine whether companies pass costs to consumers or compress margins.

- Vegetable oil and biofuel linkage: movements in global vegetable oil indices underscore a second‑order risk channel — biofuel demand can influence soy oil valuations, which feed through processing economics for soymilk manufacturers.

- Consumer health narratives: targeted promotional activity and in‑store education — a tactic visible in several markets — are lifting sales of unprocessed and protein‑forward soy offerings. Regulatory clarity on plant‑based labeling will affect packaging claims; early alignment with country rules avoids late‑stage repack costs.

2026 priority playbook — five immediate actions for executives

- Implement a two‑track procurement strategy: short‑term hedges for immediate exposure and a medium‑term supplier diversification plan that includes co‑ops, regional crushers and non‑traditional sourcing to reduce concentration risk.

- Define a protein segmentation strategy: identify where high‑protein SKUs can carry price increases and where clean‑label minimalism drives trial. Use pilot markets to validate elasticity before national rollouts.

- Rationalize SKUs and pack sizes: remove low‑velocity SKUs, redeploy space to premium/refrigerated ranges, and align pack architecture with retailer promotional cycles to improve shelf economics.

- Invest in data‑driven channel allocation: reweight promotional spend toward channels showing higher trial conversion (digital and convenience) while protecting heartland retail penetration.

- Prepare M&A and co‑manufacturing playbooks: use market concentration insights to identify tuck‑in targets, contract manufacturing partners and capacity expansion candidates who accelerate time‑to‑market for new formulations.

Why PW Consulting’s Soy Milk Market report matters for 2026

We designed this study to be a decision tool, not just a retrospective. By combining a transparent financial model (2020–2032), a market concentration analysis, procurement stress testing and competitor playbooks, the report converts macro trends into executable choices. The study highlights a market growing at roughly 6.02% CAGR in our base case and provides the scenario sensitivity to quantify upside and downside outcomes central to M&A, pricing and supply strategy in 2026.

For teams preparing annual plans, evaluating acquisitions, or redesigning portfolios, this report delivers the strategic clarity and operational templates required to act quickly while managing downside exposure. To access the full market model, regional breakdowns, SKU‑level forecasts and transaction‑grade annexes, please visit the PW Consulting report page — the complete intelligence package awaits decision makers ready to move from insight to action.

For detailed analysis of this topic, please visit the official page:Soy Milk Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com