Medical Polymers Market Outlook 2024-2035: Competitive Insights, Revenue Projections & Segment Expansion

Health |

2026-05-12 06:21:11

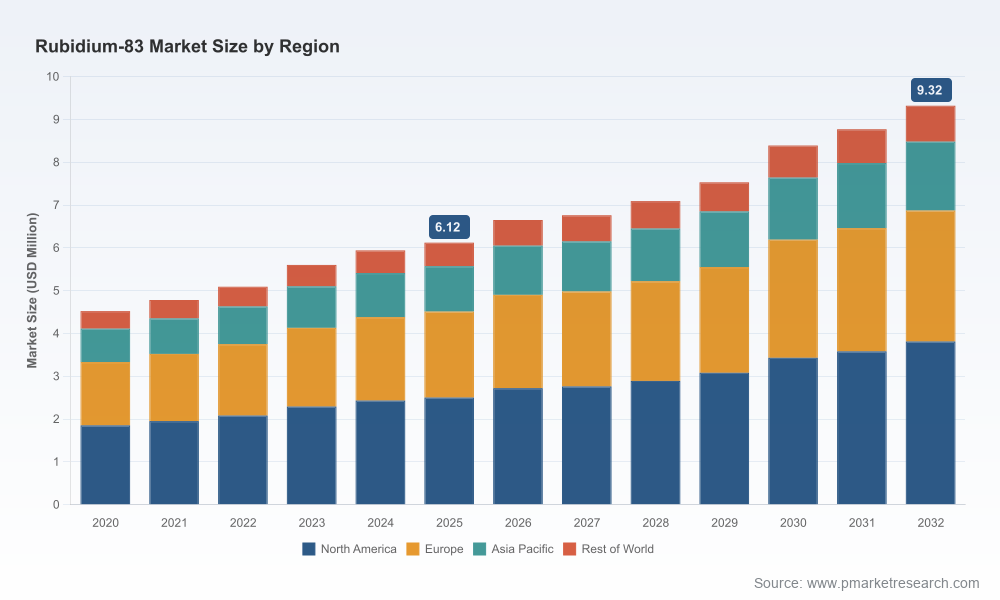

PW Consulting’s latest Rubidium‑83 Market report (base year 2025; historical 2020–2025; forecast 2026–2032) provides a focused, decision‑grade briefing for corporate strategy teams, procurement leaders, and research‑intensive organizations planning commitments in 2026. Our analysis synthesizes market sizing, competitive dynamics, production economics, regulatory constraints, and practical go‑to‑market options into an actionable framework. The headline: the market is small but expanding at a sustained clip — from roughly USD 4.5 million in 2020 to about USD 6.12 million in 2025, with a projected rise to approximately USD 9.32 million by 2032 at a compound annual growth rate (CAGR) of 6.18% — creating concentrated windows of commercial opportunity and supply risk that require nuanced strategic responses.

Rubidium-83 Market

Convergence of science and applied demand: Rubidium‑83’s role as a calibration and tracer isotope in advanced physics experiments, PET tracer development, and high‑precision spectroscopy keeps the molecule highly relevant to both fundamental research and emerging medical applications. Incremental increases in research and preclinical activity are translating into predictable, above‑market growth.

Rubidium-83 Market

Concentrated supply base: Our concentration metrics point to a high level of market consolidation — the top three suppliers control the vast majority of commercial supply, with an even steeper concentration among the top five. That concentration amplifies supply‑side leverage and makes supply diversification a strategic priority for buyers.

Rubidium-83 Market

Supply chain nuances: Production is accelerator‑dependent (proton bombardment of rubidium chloride targets) rather than primary mining. Rubidium itself is typically produced as a byproduct of other mineral processing streams. These characteristics make lead times, production scheduling, and regulatory compliance the dominant operational constraints — not raw ore availability alone.

Rigorous market sizing & trajectory: granular topline time series that trace the market from 2020 through 2032 and a transparent modeling approach that explains how policy shifts, R&D funding trends, and manufacturing investments map to the 6.18% CAGR and the USD 2025–2032 trajectory.

Supply chain forensic: a supplier‑level view of production pathways (accelerator vs. reactor techniques), typical lead times, batch cadences, and the technical chokepoints that create short windows of scarcity during peak research cycles.

Regulatory & quality playbook: practical checklists for compliance and procurement, including radionuclidic purity expectations, shipping and handling controls, and audit protocols that protect downstream users from contamination or non‑conforming material.

Commercial intelligence & contract language: templated contracting language, term‑sheet options, and risk‑allocation clauses calibrated to a concentrated supplier market and to the production realities of special‑order isotopes.

Investment and operational scenarios: scenario planning models for capital deployment (e.g., investment in cyclotron capacity), off‑take structuring, and rental/lease models for isotope generators to reduce on‑balance‑sheet supply risk.

Procurement playbook: a prioritized checklist of short‑, medium‑, and long‑term actions for procurement teams to secure resilient supply while minimizing capital outlays.

Our competitive assessment highlights a mix of government‑affiliated supply, specialist distributors, and materials producers. The National Isotope Development Center (NIDC) and the DOE Isotope Program play an outsized role in ensuring research supply availability in the United States through accelerator‑produced batches offered under special order; their distribution model and strict radionuclidic purity specifications effectively set a technical baseline for research‑grade material. Several private firms — including established specialty materials houses and isotope distributors — operate in parallel, offering catalogue access to rubidium compounds and isotopic variants, and providing logistics support for research and industrial users.

National Isotope Development Center (NIDC) / DOE Isotope Program — Oak Ridge, TN: Serves as a primary U.S. channel for accelerator‑produced Rubidium‑83. Their institutional role and product specifications make them both a supply anchor and a compliance lodestar for users requiring traceable, research‑grade material.

American Elements — Los Angeles, CA: A global supplier of rubidium compounds and stable isotopes, American Elements offers research‑grade materials across materials science and biomedical research ecosystems and is a core commercial node for labs that prefer catalogue procurement.

Trace Sciences International — Ontario (with U.S. operations): Specializes in stable and radioactive isotopes, emphasizing high‑purity products for medical, industrial, and research applications. Their North American presence supports logistical responsiveness for time‑sensitive orders.

AMT Ventures / AMT Isotopes — U.S. distributor with global reach: Acts as a distribution and fulfillment hub for rubidium isotopes used in PET tracer development and research‑oriented imaging workflows, bridging manufacturers and end‑users.

Rubidium‑83 supply is delivered almost exclusively through controlled production pathways and is typically offered under special‑order arrangements that carry strict radionuclidic purity and documentation requirements. These constraints affect lead times, acceptable transport modalities, and QA/QC regimens. For organizations that rely on Rb‑83 for calibration or tracer programs, missteps in validation or compliance can lead to costly program delays — an important consideration when weighing contract tenors and inventory policies.

Price pressure and input variability: Recent market observations show compound‑level price inflation across rubidium products in recent years. For buyers, that creates two implications: hedge with medium‑term offtakes where possible, and prepare procurement processes to evaluate total landed costs including compliance and waste disposition.

Geopolitical concentration of upstream supply: Primary mineral and processing capacities for rubidium are concentrated in a small set of producing countries. While rubidium as an element is not mined on a primary commercial scale, this geopolitical profile informs risk assessments for organizations pursuing near‑term supply guarantees or alternate sourcing strategies.

Technology levers: Cyclotron‑based production remains the most accessible route for research quantities; targeted investments in local accelerator capacity or partnerships with existing facilities can materially reduce supply risk for institutions with sustained demand.

Classify demand by criticality and lead timeframe: Segment internal demand profiles into steady, intermittent, and mission‑critical buckets. For mission‑critical programs, prioritize multi‑year offtakes or reserved capacity arrangements with key suppliers.

Layer procurement tactics: Combine short‑term spot buys for flexibility with medium‑term committed purchases to secure access, and evaluate the economics of co‑investment in production capacity where volumes justify capital.

Negotiate technical KPIs into contracts: Insist on documented radionuclidic purity, traceability, and QC acceptance protocols. Embed penalty and remediation clauses for non‑conforming batches to protect program timelines.

Pursue strategic partnerships: Explore collaborative agreements with accelerator facilities, national isotope programs, or distributors to create preferred access windows — particularly valuable in a market with high supplier concentration.

Institutionalize scenario planning: Adopt a three‑scenario stress‑testing approach (base, constrained, and accelerated adoption) to determine inventory buffers, capex triggers, and R&D pacing for substitutable technologies.

The full report integrates quantitative projections, supplier profiles, procurement templates, and a decision matrix that translates market signals into pragmatic actions for 2026. Clients will find modeled outcomes under alternative assumptions, legal/contractual language modules, and a proprietary supplier risk dashboard designed to inform both tactical purchases and strategic capital allocation. While the public summary here highlights top‑line growth and strategic levers, the report contains the detailed split‑level modeling, supplier scorecards, and contract templates that operational teams require to execute.

For procurement leaders: Use our procurement playbook to structure immediate offtake discussions and to build multi‑tier supplier panels that balance reliability and cost.

For R&D and lab managers: Map your experimental pipelines to our demand classification and assess whether shared accelerator partnerships or internal capacity investments are warranted.

For corporate strategy and investors: Evaluate strategic options including joint ventures with accelerator operators, minority investments in leading distributors, or structured offtake financing to secure supply at scale.

This briefing is a tactical preview designed to inform 2026 decisions. PW Consulting’s full Rubidium‑83 Market report contains the confidential modeling, supplier scorecards, and contractual playbooks necessary for implementation. For access to the complete dataset, scenario models, and the procurement toolkit, contact PW Consulting or visit our report page to request the full deliverable and schedule a briefing with our isotope market specialists.

For detailed analysis of this topic, please visit the official page:Rubidium-83 Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com