3D Dental Scanners Market Outlook 2031: Growth Drivers, Opportunities, and Competitive Landscape

Health |

2026-03-18 13:41:07

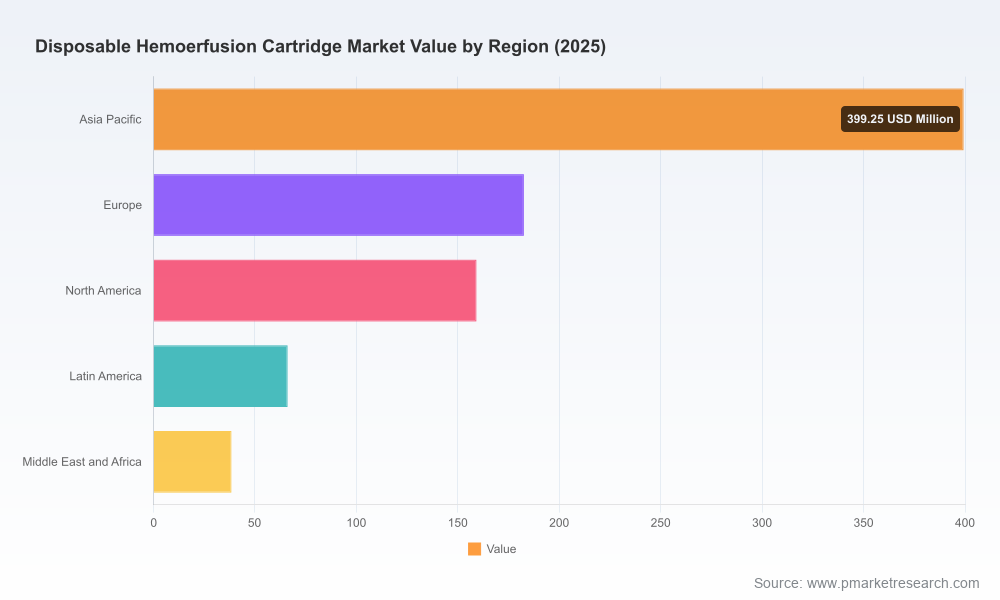

PW Consulting’s latest market study on the Disposable Hemoperfusion Cartridge Market delivers a decision-grade intelligence package aimed at executive teams, corporate development groups, and investor boards planning for 2026 and beyond. The global market, valued at USD 845.5 Million in our base year (2025), is projected to expand at a compound annual growth rate (CAGR) of 9.02% through the 2026–2032 forecast window, reaching approximately USD 1,547.6 Million by 2032. This growth trajectory reflects accelerating clinical adoption across critical care, renal therapy adjacencies, and acute toxicology use cases, plus intensifying activity among established and emerging suppliers.

Disposable Hemoerfusion Cartridge Market

Timing is strategic: 2026 is a watershed year for product registrations and commercial access strategies. Our full analysis pinpoints the regulatory inflection points and clinical evidence milestones that will determine who captures early-adopter share in hospital networks.

Disposable Hemoerfusion Cartridge Market

Scaling versus differentiation trade-offs: Manufacturers face a classic build-or-borrow choice. The market’s structure—moderately concentrated at the top (CR3 ~58.4%, CR5 ~72.15%)—means scale advantages exist but specialized technologic differentiation and channel execution can win sustainable niches.

Disposable Hemoerfusion Cartridge Market

Revenue and investment planning: With market size and growth clearly upward, corporate planning must align R&D, regulatory, manufacturing, and commercial investments on a common timeline. Our report converts the macro forecast into practical decision triggers for 12–36 month investments.

Regulatory-first commercial strategies will accelerate market access. Recent regulatory movements and device-class conversations mean companies that lock down robust regulatory pathways and engage early with authorities will shorten time-to-revenue.

Clinical evidence now shapes procurement. Beyond nominal approvals, hospital formularies and critical care programs are demanding targeted outcome data (e.g., cytokine modulation, toxin removal, perioperative antithrombotic safety). Investment in pragmatic trials and registries pays off in purchasing committees.

Manufacturing capacity is a competitive moat—but not an absolute barrier. Large-scale automated production lines confer cost and lead-time advantages; however, contract manufacturing and regional production partnerships remain effective options to address near-term demand spikes.

Channel and bundling models matter: bundling cartridges with compatible circuits, disposables and service contracts increases switching costs for hospitals and improves lifetime revenue per patient.

Consolidated market sizing and three adoption scenarios (base, accelerated, constrained) with sensitivity analyses keyed to regulatory outcomes, clinical trial readouts, and reimbursement dynamics.

Competitive intelligence dossiers on leading suppliers, including manufacturing footprints, product technology stacks, clinical positioning, distribution models, and commercial playbooks.

Clinical evidence map and gap analysis that aligns indications, study designs, and key opinion leader (KOL) networks with payer and hospital procurement requirements.

Regulatory playbook by geography that prescribes submission strategies, expected timelines, and risk mitigations for De Novo, PMA, and special controls pathways.

Commercial go-to-market modules: channel prioritization, pricing architecture templates, tender and GPO negotiation tactics, and hospital adoption accelerators.

Manufacturing and supply-chain toolkit highlighting capacity planning, quality systems alignment (ISO/cleanroom guidance), supplier diversification, and cost-to-serve modelling.

M&A and partnering playbook with screening criteria for bolt-on technologies, licensing targets, and distribution partnerships—plus financial model templates for diligence.

The market exhibits a mix of large, well-capitalized players and nimble specialist manufacturers. The dominant incumbents combine clinically validated platform products with established production capabilities and distribution networks. Key strategic profiles in the market include:

Jafron Biomedical — A technology-anchored incumbent known for its HA series resin-based cartridges and substantial automated production capability. Jafron’s emphasis on tailored pore distributions for targeted adsorption and a documented large annual manufacturing throughput position it strongly for volume and global tender opportunities. Recent regulatory wins for select products in international markets further de-risk export strategies.

Foshan Biosun — Focused on sterile, single-use cartridges for cytokine and middle-molecule adsorption. Product sterility claims and single-use positioning support hospital infection-control narratives and make Biosun a credible partner for renal and critical-care programs in markets prioritizing disposables.

Baihe Medical — Plays to renal therapy integrations, positioning hemoperfusion as a complementary therapy with hemodialysis to enhance toxin clearance. Clinical collaborations and dialysis channel access are primary advantages.

Asahi Kasei / Toray-related entities — These organizations bring polymer science and endotoxin-focused solutions (e.g., polymyxin B immobilized fibers) that align with sepsis and septic shock treatment pathways where endotoxin adsorption is a clinical priority.

CytoSorbents Corporation — A case study in platform propagation and clinical adoption; the CytoSorb polystyrene-divinylbenzene cartridge is widely used in critical care and perfusion contexts with significant cumulative device use. Recent corporate activity in 2025–2026—product innovations enabling multi-cartridge workflows, renewed distribution deals in Europe, and active regulatory engagement with the FDA for novel De Novo applications—signals an aggressive global commercialization phase and a focus on perioperative and antithrombotic-use cases.

Other players — Kaneka, Toray Medical, Baxter, and regional manufacturers such as DiaCare provide a mix of legacy charcoal technologies, polymer platforms, and localized supply models. Their presence increases competitive options for hospital buyers and creates opportunities for alliances or white-label supply agreements.

Regulatory engagements by platform companies and regulators’ historical inclination to reclassify sorbent devices suggest a near-term window where regulatory clarity will materially affect commercialization paths. Companies should accelerate regulatory planning to align with likely special control frameworks where applicable.

Clinical and partnership updates from major suppliers—product lifecycle expansions, multi-cartridge workflow solutions, and targeted pre-submission meetings with regulators—highlight that clinical positioning and device interoperability are now primary competitive battlegrounds.

Manufacturing footprints and capacity statements announced by large suppliers reinforce that supply reliability and lead times will be decisive in formulary inclusion during procurement cycles.

0–12 months (Quick wins): Finalize regulatory submission strategy for prioritized markets; secure distribution pilots in 3–5 hospital systems; launch targeted real-world evidence registries for the most commercially relevant indications.

12–24 months (Scale): Ramp manufacturing (in-house or CMOs) tied to forecasted hospital adoption; negotiate GPO/tender inclusion; integrate cartridges into bundled therapy offerings with consumables and services.

24–36 months (Consolidate): Pursue strategic partnerships or M&A to acquire complementary technologies (e.g., advanced sorbents, extracorporeal organ perfusion interfaces), and expand payer engagement with cost-effectiveness dossiers supported by registry and trial data.

Regulatory headwinds — mitigate with early authority engagement, parallel submissions where possible, and modular clinical programs that allow staged claims.

Clinical adoption uncertainty — mitigate through KOL networks, targeted pragmatic studies, and inclusion in multidisciplinary care pathways (ICU, cardiac surgery, nephrology).

Supply interruptions — diversify manufacturing and develop contingency stocking agreements with hospital partners for critical-use cartridges.

For companies planning capital allocation and market entry strategies in 2026, the disposable hemoperfusion cartridge market offers meaningful growth and differentiation upside—but only for those who align regulatory execution, clinical evidence generation, and scalable manufacturing. Our study translates macro market momentum (USD 845.5 Million in 2025; ~9.02% CAGR through 2032 with a projected market of roughly USD 1.55 Billion by 2032) into discrete operational choices: who to partner with, what evidence to generate first, and where to invest in capacity. The competitive and regulatory environment rewards focused playbooks and penalizes scattered investments.

PW Consulting’s full report contains the proprietary segmentation tables, regional and application-level forecasts, financial model templates, and downloadable commercial toolkits referenced above. For organizations preparing capital plans, M&A diligence, or market-entry playbooks for 2026, access to the complete dataset and operational annexes is essential. Visit our report page to request the full Disposable Hemoperfusion Cartridge Market report and to schedule a strategy workshop tailored to your business objectives.

For detailed analysis of this topic, please visit the official page:Disposable Hemoerfusion Cartridge Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com