Light Commercial Vehicle Transmission Market: Strategic Imperatives for 2026

PW Consulting’s latest market research on the Light Commercial Vehicle (LCV) Transmission market synthesizes market dynamics, competitive positioning, and executable strategies that matter for boardrooms and product teams in 2026. Built on a rigorous historical base (2020–2025) and a forward-looking forecast horizon (2026–2032), this briefing translates our full report’s quantitative modeling and qualitative intelligence into clear decisions: where to deploy capital, which partnerships to pursue, and how to future-proof product portfolios. As a concise preview, this release highlights the analytical depth and the strategic levers embedded in the full study while intentionally withholding detailed segment-level figures reserved for the complete report.

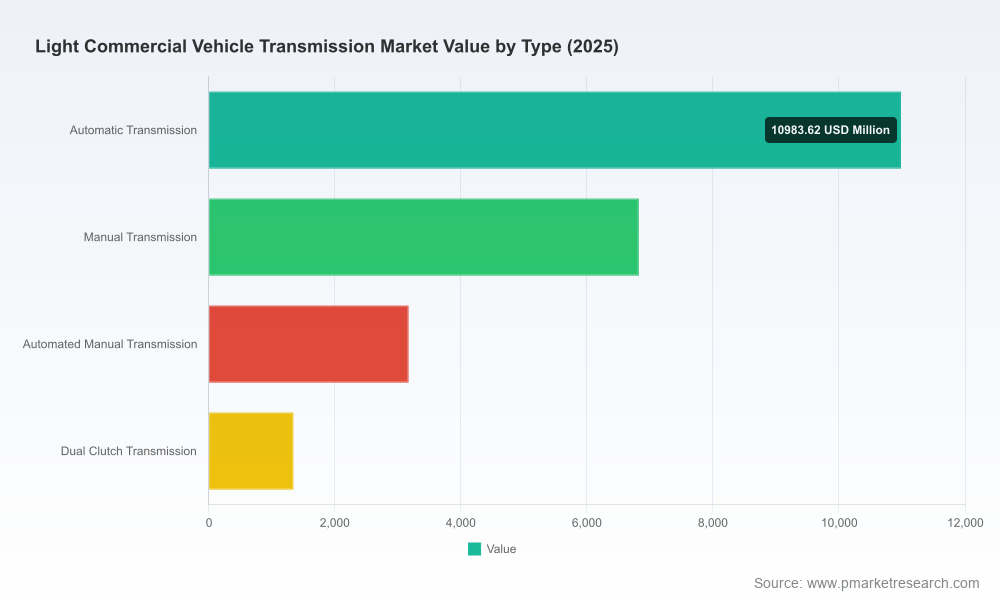

Light Commercial Vehicle Transmission Market

Macro view: growth trajectory and structural features

The global LCV transmission market stands on a steady growth path. Using 2025 as the base year, PW Consulting’s model forecasts a compound annual growth rate of 5.71% over the 2026–2032 period. The market has expanded from the low end of the 2020s to exceed USD 22 billion (Million-USD basis) in 2025, with projected expansion through 2032 that reflects the combined effects of fleet renewal cycles, fuel-economy driven product upgrades, and the gradual introduction of electrified transmission architectures.

Light Commercial Vehicle Transmission Market

Market concentration is moderate and trending toward selective consolidation: the top three suppliers account for approximately 38.5% of market revenues, and the top five approach a majority share at 52.7%. This structure creates two concurrent strategic realities: established OEMs retain pricing power and influence over standards, while mid-size and specialized suppliers can capture high-margin niches by aligning with vehicle OEMs seeking differentiation (electrified drivetrains, DCT for efficiency, or ruggedized automatics for vocational use).

Light Commercial Vehicle Transmission Market

Why PW Consulting’s 2026 intelligence matters

- Timing investment decisions: the market’s mid-single-digit CAGR signals predictable growth but high variation across technology cohorts. Execution windows for new architectures (e.g., compact e-transmissions or DCTs tailored to LCV weight classes) are finite—acting within the next 18–36 months will materially affect go-to-market advantage.

- Portfolio prioritization: regulatory pressure on fuel consumption and emissions is accelerating the replacement of legacy 3–5 speed architectures with multi-speed automatics and electrified modules. Companies must prioritize R&D and validation cycles that align with 2027–2029 product ramps to capture OEM program slots.

- Supply-side resilience: raw material volatility and trade policy shifts are non-trivial cost and timing risks. Procurement and manufacturing strategies that ignore price and tariff tailwinds risk margin erosion or program delays.

What’s in the full report (practical, not academic)

Our study is designed for executives who need immediately actionable outputs, not just descriptive statistics. Core deliverables include:

- Market-sizing model (2020–2032) with downloadable worksheets enabling custom scenario adjustments for fuel prices, electrification uptake, and regulatory tightening.

- Segment-level demand drivers and technology roadmaps covering automatic, manual, automated-manual, dual-clutch, and electrified transmission families—paired with product maturity curves and OEM adoption estimates.

- Supplier benchmarking and playbooks: go-to-market matrices that align supplier capabilities with OEM buying criteria by vehicle class and use-case (last-mile delivery, freight, construction, etc.).

- Cost and margin templates: component-level bill-of-material (BOM) sensitivity to steel/aluminum price swings and assembly labor models suitable for country-level offshoring/nearshoring analysis.

- Regulatory and tariff impact assessments with mitigation options—ranging from local content strategies to tariff-evasion engineering choices consistent with compliance.

- Strategic M&A roadmaps—valuation primers for bolt-on buys in electrified modules, power electronics integration, and specialized gearbox manufacturing.

To preserve the competitive value of the study we are providing a guided overview here; detailed split tables, regional/application percentages, and granular revenue by segment are available in the full PW Consulting report and the companion data pack.

Competitive landscape — the players shaping 2026 programs

The market’s shape is being influenced by a core group of equipment suppliers that are investing in product breadth and electrified options. Key competitive positions to watch:

- ZF Friedrichshafen AG (Friedrichshafen, Germany): ZF continues to push multi-speed automatics into medium and heavier LCV classes with its PowerLine family. Recent product launches in 2026 demonstrate ZF’s commitment to combining higher-speed counts with durability targets for vocational applications.

- Aisin Corporation (Kariya, Japan): Aisin’s portfolio blends traditional automatics with compact dual-clutch and EV-targeted transmissions—positioning the firm as a supplier to OEMs seeking packaging efficiency alongside electrification readiness.

- Allison Transmission Holdings, Inc. (Indianapolis, USA): Allison remains a reference in heavy-duty automatics scaled for lighter platforms; its series are frequently specified where durability under urban repeated-stop cycles is a key procurement metric.

- Eaton Corporation (Dublin, Ireland): Eaton’s automated manual and dual-clutch solutions are geared toward balancing efficiency gains with cost sensitivity in LCV and bus applications—its recent Advantor-6 introduction exemplifies this strategy.

- BorgWarner Inc. (Auburn Hills, USA): BorgWarner’s moves into hybrid and electrified modules signal a deliberate pivot to powertrain electrification components and integrated module supply for OEMs seeking single-source suppliers.

- Dana Incorporated (Maumee, USA) and Magna International Inc. (Aurora, Canada): Both firms extend transmission-related competencies into e-drives and component integration—making them attractive partners for vehicle programs that demand seamless e-axle integration.

Recent vendor activity underscores the competitive theme: ZF’s 8-speed PowerLine entry into medium-duty truck platforms (announced March 2026) and Eaton’s mid-2025 Advantor-6 automated-manual launch show incumbent suppliers are accelerating product introductions to secure program wins. Aisin’s announcement of a compact DCT for EV/light-truck applications also signals the race to offer compact, electrification-ready transmissions.

Three strategic scenarios for 2026 planning

PW Consulting’s scenario framework helps leaders map decisions to outcomes. We summarize three plausible market trajectories and the corresponding strategic imperatives:

- Base scenario (moderate electrification): Continued roll-out of multi-speed automatics and gradual electrified module adoption. Priority: balance CAPEX between conventional transmission upgrades and modular electrified designs; secure OEM program slots through targeted investment in validation and supplier partnerships.

- Accelerated electrification scenario: Faster-than-expected policy-driven electrification of last-mile and light-duty fleets. Priority: reallocate R&D to e-transmission and integrated e-axle systems, accelerate partnerships with power electronics suppliers, and de-risk battery–drive integration via pilot programs.

- Protectionist/regionalization scenario: Trade barriers and component tariffs force localization of supply chains. Priority: modularize manufacturing footprints, adopt nearshoring for high-tariff components, and redesign BOMs for local content compliance while preserving global engineering synergies.

Supply chain, raw materials, and policy levers

Transmission manufacturing remains metal-intensive, and volatility in steel and aluminum markets directly hits margins. Active procurement strategies—long-term strategic agreements, hedging, and demand pooling with OEM partners—are non-negotiable for margin protection. Additionally, policy shifts such as the November 2025 tariff actions on certain imported vehicle parts create an immediate need for scenario planning: suppliers should quantify tariff exposure, consider local assembly or subassembly strategies, and evaluate partial vertical integration for high-value components.

Recommended 2026 playbook (practical moves)

- Fast-track electrified module pilot projects with a manufacturing partner to shorten time-to-market by 12–18 months versus a greenfield approach.

- Negotiate multi-year commodity contracts tied to indexation clauses to reduce margin volatility from metal price movements.

- Prioritize program wins in last-mile and vocational fleets where repeatable cycles and scale can quickly amortize development costs.

- Build modular architectures to enable rapid derisking of OEM integrations—standardize interfaces for e-motor, inverter, and gearbox sub-systems.

- Prepare a regionalization contingency plan: identify two to three low-cost production nodes and model the incremental cost of local content compliance under tariff scenarios.

Conclusion — the strategic value of PW Consulting’s full study

For decision-makers planning 2026 capital and product initiatives, the full PW Consulting report converts market-size trajectories, competitive intelligence, and regulatory foresight into executable strategies. Our modeling is transparent, auditable, and designed for immediate embedding into investment memos, product roadmaps, and procurement negotiations. To preserve commercial confidentiality and competitive advantage, this preview omits the detailed segmented revenue tables and region/application percentage breakdowns that underpin program-level decisions; those datasets, plus the actionable playbooks and downloadable models, are available in the complete report.

Contact PW Consulting to access the full Light Commercial Vehicle Transmission Market report and the companion data pack—enable your team to convert the 2026 market position into a sustainable advantage.

For detailed analysis of this topic, please visit the official page:Light Commercial Vehicle Transmission Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com