Semi Direct Drive Wind Turbine Generator System Market: Strategic Intelligence for 2026 Decision‑Makers

Executive snapshot

PW Consulting’s latest market study on Semi Direct Drive Wind Turbine Generator Systems (WTGS) delivers an operationally focused intelligence package tailored for executive teams planning capital allocation, technology roadmaps, and supply‑chain strategies in 2026. Using a 2025 base year and a comprehensive 2020–2025 historical window, our forecast covers 2026–2032 with a compound annual growth rate of 12.02%. Under the central scenario the market grows from the 2025 base to reach a materially larger industry by 2032, reflecting accelerating offshore rollouts, higher megawatt class adoption, and continued drivetrain innovation.

Semi Direct Drive Wind Turbine Generator System Market

Why this report matters in 2026

- Actionable market sizing calibrated to procurement cycles: developers and OEMs can align multi‑year purchasing commitments and factory ramp plans against a validated top‑line growth trajectory anchored in 2025 baseline data.

- Decision‑grade supplier intelligence: the report translates technology roadmaps and prototype outcomes into practicable supplier selection criteria—useful for CAPEX negotiations, warranty structuring, and partner selection.

- Risk and opportunity maps tied to real project timelines: investors and project developers receive scenario analyses that link material, logistics, and policy risk to expected commissioning windows.

- Technology investment signals: R&D leaders gain prioritized themes—such as medium‑speed drivetrain optimization and rare‑earth reduction—that maximize near‑term performance gains without extending certification timelines.

Core market dynamics shaping 2026 choices

The semi direct drive proposition is increasingly framed as the pragmatic middle path between heavy direct‑drive architectures and high‑speed geared systems. For large‑megawatt offshore applications, semi direct drive architectures are delivering a balance of reliability, transmission efficiency, and total lifecycle cost that is driving accelerated commercial interest. Key dynamics for 2026 include:

Semi Direct Drive Wind Turbine Generator System Market

- Technology convergence: Medium‑speed drivetrains—combining compact gear stages with high‑efficiency permanent magnet generators—are maturing from pilot phases into serial production. These platforms notably reduce permanent magnet material intensity versus full direct‑drive alternatives, improving both supply resilience and unit economics.

- Material and supply‑chain pressure: While permanent magnets remain central to many semi‑direct designs, industry programs to reduce rare‑earth dependence and to re‑engineer magnet usage have moved from theory to implementation. Procurement teams must therefore reconcile short‑term magnet availability with longer‑term material‑reduction initiatives.

- Concentration and competitive dynamics: The supplier landscape is already consolidated at the top end—our market concentration metrics indicate a high level of share owned by a handful of OEMs. This creates asymmetric negotiating leverage for tier‑1 suppliers but also opens windows for specialized component and subassembly players who can demonstrate reliability and integration advantages.

- Certifications and grid integration: Grid‑adaptability features embedded in semi‑direct systems (lower vibration, improved thermal stability, and better fault‑ride‑through characteristics) are shortening the path to certification in key offshore jurisdictions, accelerating project bankability.

Competitive landscape — what to watch from OEMs to subsystem specialists

Our competitive analysis combines public announcements, prototype performance signals, and supplier integration depth to profile strategic postures across the value chain. Leading firms illustrate three distinct plays: holistic platform scale, integrated drivetrain engineering, and component specialization.

Semi Direct Drive Wind Turbine Generator System Market

- Ming Yang Smart Energy Group Co., Ltd. (China) — A platform‑focused leader in semi‑direct offshore WTGS. Ming Yang’s medium‑speed compact drive (MCD) family and typhoon‑resistant models indicate a go‑to market that prioritizes serial manufacturability and site‑resilience. Their recent product unveilings signal an aggressive move into floating concepts and higher‑capacity platforms, which will test supply‑chain elasticity and partner selection strategies in 2026.

- Dongfang Electric Corporation (DEC) (China) — DEC’s trajectory is characterized by fully integrated semi‑direct solutions that bundle shaft systems, gearbox stages, and in‑house permanent magnet generators. Prototype installations of very large machines demonstrate an OEM capability to push unit size while controlling key drivetrain interfaces—an attractive proposition for developers seeking single‑vendor responsibility for major offshore foundations.

- Goldwind Science & Technology Co., Ltd. (China) — Historically focused on permanent magnet direct‑drive variants, Goldwind’s selective incorporation of medium‑speed drivetrains shows a hybrid strategy designed to balance performance with manufacturing cost and logistics. Expect modular portfolio rationalization and selective adoption of semi‑direct platforms for specific offshore projects.

- Yinchuan Weili Transmission Technology Co., Ltd. (China) — A component specialist that supplies semi‑direct speed‑increaser assemblies. Their compact, lightweight designs provide a value‑add to OEMs seeking reduced nacelle mass and improved drivetrain integration. For procurement teams, validated subsystem partners like Weili can be leveraged to de‑risk OEM concentration and to introduce competitive pressure on gearbox integration quality.

Recent prototype launches and installations by major players have confirmed that technical risk is moving into the operations phase—an important inflection for 2026 sourcing strategies. While top‑tier OEMs retain scale advantages, targeted subsystem suppliers and new entrants with differentiated IP represent potential acquisition or partnership targets.

What our report contains (practical deliverables)

This study was designed with practitioner adoption in mind. Core deliverables include:

- Top‑down market sizing and validated forecast model (2026–2032) with scenario toggles for supply disruption, price inflation, and policy acceleration.

- Project‑level demand pipeline intelligence aligned to permit and procurement timelines—designed to feed procurement planning and factory ramp models.

- Supplier scorecards and integration readiness assessments—covering drivetrain, tower, and foundation supplier pools together with commercial terms to expect at various volumes.

- Technology benchmarking and TRL matrix—covering drivetrain architectures, generator designs, and rare‑earth reduction pathways.

- Cost models (CAPEX/OPEX) and LCoE sensitivity tables engineered for investor due diligence.

- Regulatory and certification matrix that links jurisdictional requirements to likely timeline impacts and cost adders.

- Go‑to‑market playbook for OEMs, developers, and investors that outlines partnership structures, JV templates, and M&A target profiles.

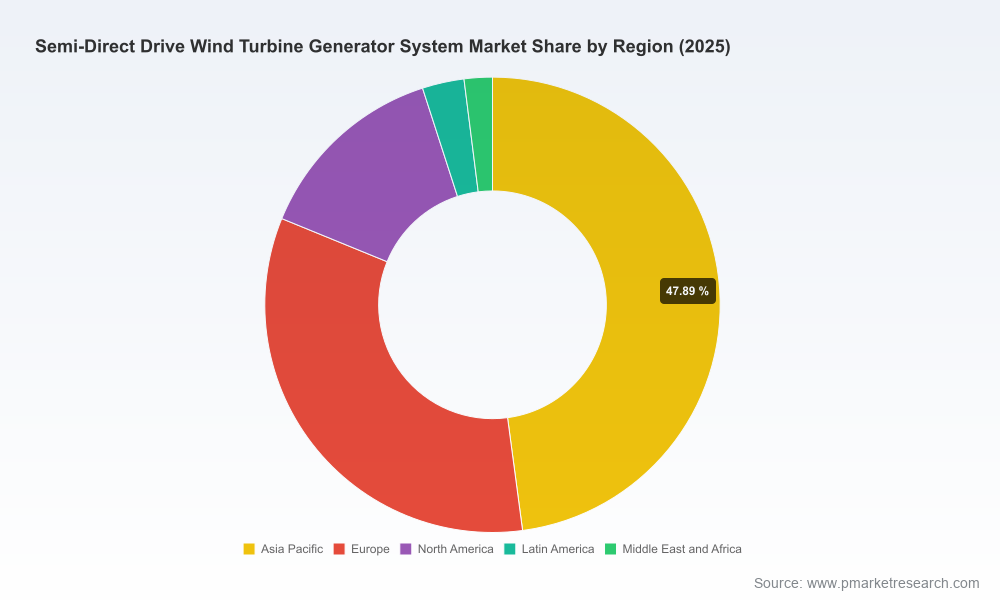

To preserve competitive value and to respect proprietary inputs, we intentionally withhold granular subsegment share tables and region‑level application dollar breakdowns from this public summary. These are available in the full report package and downloadable data workbook.

Strategic recommendations for 2026 decision calendars

- Prioritize supplier agreements that include performance‑based milestones and shared warranty corridors. Given the stage‑gated nature of semi‑direct commercialization, contracting structures should align incentives and defray early‑operational risk.

- Adopt a dual‑track magnet strategy: secure short‑term magnet supply through hedging or offtake while funding medium‑term R&D or co‑development to reduce rare‑earth dependency.

- Evaluate manufacturing footprint choices against a two‑year visibility window—in many cases, nearshore pre‑assembly combined with local installation services will lower logistics risk more than pure low‑cost offshore manufacturing.

- Pursue targeted partnerships with subsystem specialists to retain bargaining power with tier‑1 OEMs. Component‑level partnerships can accelerate certification timelines and provide optionality for repowering strategies.

- Embed flexibility into offtake contracts (indexed ramp, acceptance windows tied to prototype performance) to mitigate the financial impact of potential late‑stage design changes.

How this report supports corporate decisioning in 2026

Executives and strategy teams entering procurement and capex planning cycles in 2026 will need one integrated source that translates technical maturity into commercial outcomes. PW Consulting’s study synthesizes prototype evidence, supplier capabilities, and policy drivers into a single decision framework—mapping when to invest, whom to partner with, and how to structure deals to protect balance sheets while capturing upside from rapid market growth.

Methodology and credibility

Our analysis blends bottom‑up project pipeline aggregation, multi‑year price and cost curves, OEM technical disclosures, and primary interviews with supply‑chain executives. Market concentration metrics in the study quantify the dominance of leading OEMs and identify pockets of supplier opportunity. Where public signals are ambiguous, we triangulate using independent engineering assessments and commissioning timelines to produce scenario ranges that are explicitly documented in the report.

Next steps & where to access the full intelligence

This release is a strategic preview. For complete subsegment data, downloadable financial models, supplier scorecards, and annex tables that support capital planning in 2026, please refer to the full report package and data workbook available on our report page. The public summary purposefully omits the granular breakdowns and company share tables that are included in the paid deliverable—ensuring subscribers receive the actionable detail needed to execute in 2026.

PW Consulting stands ready to support tailored briefings, scenario‑customized models, and transaction due diligence built from the report’s primary datasets. Contact our Semi Direct Drive practice to arrange an advisory engagement or to license the full report and dataset.

For detailed analysis of this topic, please visit the official page:Semi Direct Drive Wind Turbine Generator System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com