GABA Supplement Market Assessed to Reshape Functional Nutrition as Pure Encapsulations and Vitanica Scale Clean-Label Lines

Food |

2026-06-03 20:38:07

As the synthetic amorphous silica sector transitions from recovery to structurally higher growth, PW Consulting’s latest market research — Fumed Silica And Precipitated Silica Market (Base Year 2025; Forecast 2026–2032) — provides executives with the high-resolution intelligence required to make decisive moves in 2026. Our analysis synthesizes historical performance (2020–2025), a forward-looking CAGR of 5.48% through 2032, and scenario-driven implications across supply, applications and regulation. The result is a compact, strategy-focused toolkit that helps leadership teams prioritize capital allocation, de-risk supply chains, and accelerate sustainable-product roadmaps without drowning in raw segment tables.

Fumed Silica And Precipitated Silica Market

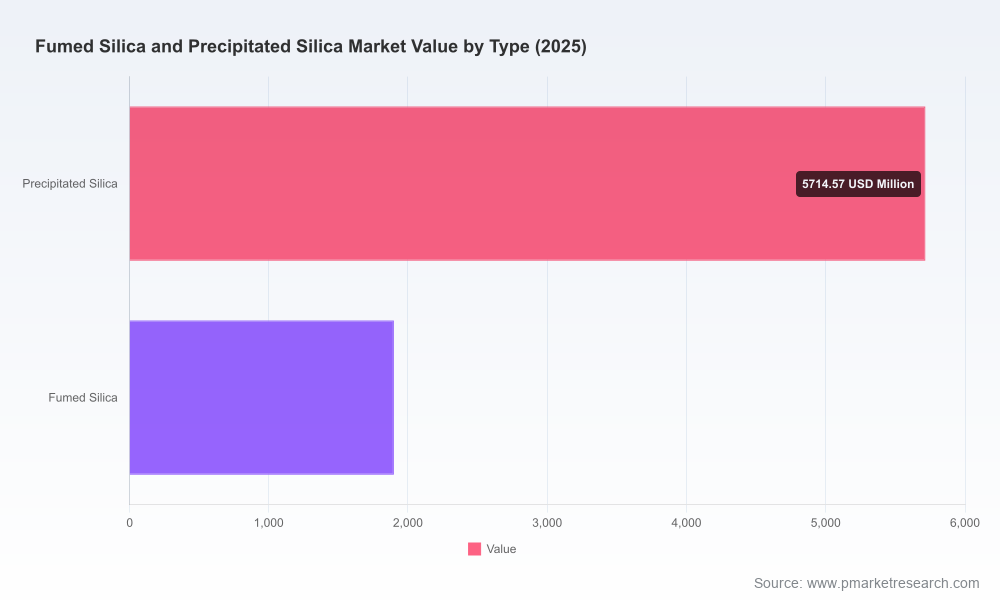

PW Consulting’s topline metric highlights a market that has expanded steadily through the early 2020s and is poised for continued compound growth at approximately 5.48% through the 2026–2032 forecast window. In absolute terms, the market size measured in 2025 serves as the reference point for 2026 planning, and our baseline scenario projects a meaningful expansion by the early 2030s. This trajectory reflects durable demand drivers—rubber reinforcement for tires and industrial elastomers, coatings and specialty additives, as well as growth niches in oral care, food applications and advanced materials (including battery and electronics adjacencies).

Fumed Silica And Precipitated Silica Market

Two structural themes underpin this growth: (1) differential demand intensity between precipitated and fumed silica use-cases, with precipitated grades anchoring tire and rubber reinforcement markets and fumed grades concentrated in high-value specialty applications; and (2) regional shifts in industrial capacity and trade flows driven by new investments, tariff dynamics and raw material price trajectories. PW Consulting’s quantitative model translates these themes into actionable ranges for revenue, utilization and margin under three demand scenarios—conservative, baseline and acceleration—enabling CFOs and business unit leaders to stress-test investments and pricing strategies.

Fumed Silica And Precipitated Silica Market

The competitive map continues to be shaped by integrated global producers, regional champions and specialized manufacturers that target high-value niches. Our qualitative and quantitative benchmarking covers strategy, asset footprints, technology positioning and recent corporate actions. Key takeaways include:

PW Consulting’s dossier profiles the dominant industry participants (from legacy multinationals to emerging regional leaders), evaluates recent strategic moves — capacity buildouts, acquisitions and JV activity — and anticipates how these decisions will reshuffle sourcing options and pricing in 2026. The full report furnishes company-level strategic matrices and playbooks that are deliberately omitted from this brief to preserve client value.

Feedstock and energy inputs were the most frequent drivers of margin compression across our historical analysis. Sodium silicate pricing and silicon tetrachloride dynamics merit particular attention: the former underwrites precipitated silica economics while the latter is a leading indicator for fumed silica supply costs. PW Consulting’s sensitivity models show how a swing in feedstock pricing propagates through EBITDA under multiple contract structures (fixed-price, pass-through and index-linked). Those models are included with the full report.

On regulation, the sector must remain vigilant to labeling and hazard communication updates. While synthetic amorphous silica retains its distinct regulatory treatment from crystalline silica, industry attention around specific hazard classifications can alter handling, product claims and insurance exposures. The report includes a regulatory-readiness checklist and recommended revisions to technical datasheets and SDS templates for 2026 compliance planning.

The published research is not a static PDF; it is an operational kit designed for corporate strategy and commercial teams that includes:

We intentionally withhold the granular regional and application-level breakdowns in this public brief to protect the commercial integrity of the dataset; however, clients who subscribe to the full report receive the complete segmentation tables, interactive excel models and company-level strategic profiles.

Our engagement model is designed to move from intelligence to implementation. Beyond the report, PW Consulting offers: tailored scenario workshops, bespoke M&A diligence, supplier optimization projects and assisted implementation of pricing and feedstock hedging strategies. For management teams that need rapid alignment, we provide executive summaries and board-ready slide decks that translate model outputs into capital allocation decisions and KPI cascades.

For companies making strategic decisions in 2026—whether committing to capacity, pursuing M&A, or refining product roadmaps—this report acts as both a risk filter and an opportunity map. The public snapshot you are reading demonstrates the depth and direction of our analysis; the full report contains the operational detail that senior management and investment committees will use to act with conviction.

To access the complete dataset, company profiles, interactive models and the implementation toolkit, please visit our report page. PW Consulting is also scheduling limited strategy sessions in Q3 2026 to help corporate teams convert the report’s insights into executable roadmaps tailored to their asset base and market position.

Contact PW Consulting’s Silica & Performance Additives practice to arrange a briefing and obtain the full Fumed Silica And Precipitated Silica Market report and associated implementation services.

For detailed analysis of this topic, please visit the official page:Fumed Silica And Precipitated Silica Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com