Explosion Proof Control Cabinet Market — Strategic Preview for 2026 Decision Makers

PW Consulting’s latest market study on Explosion Proof Control Cabinets delivers a concise, action-oriented preview of the competitive, regulatory and material dynamics that will shape investment and operational choices in 2026. Grounded in a rigorous base year of 2025 and a forecast through 2032, the report quantifies market momentum and translates it into pragmatic levers executives and technical leaders can deploy immediately.

Explosion Proof Control Cabinet Market

Why this briefing matters for 2026

As infrastructure projects, process modernization initiatives and compliance programs accelerate across hazardous industries, procurement and engineering teams face a complex set of trade-offs: certification timelines, material procurement exposure, enclosure architecture (weight, footprint, protection method), and the shifting margin economics of aftermarket services. Our report synthesizes these trade-offs into a prioritized set of strategic options calibrated to the market’s trajectory.

Explosion Proof Control Cabinet Market

- Market scale and trajectory: The global market reached approximately USD 745.2 Million in 2025 and continues on a multi-year expansion path. PW Consulting projects a compound annual growth rate (CAGR) of 6.45% over the 2026–2032 forecast horizon, culminating in a significantly larger market by 2032. This expansion is driven by capex refresh cycles in energy and process industries, rising safety and certification demands, and increasing acceptance of purged/pressurized and IoT-enabled solutions.

- Competitive structure: The market exhibits moderate concentration — the top three firms account for just over 31% of market share, while the top five approach roughly 48% — leaving substantial room for regional specialists, OEM partners and system integrators to capture niche and retrofit opportunities.

- Decision timing is critical: Lead times for certified cabinets, combined with raw material price volatility and certification backlogs in major approval bodies, mean procurement windows opened in 2026 will materially affect delivery schedules and total landed cost through 2027–2028.

What the report delivers — operationally useful content

Designed for C-suite strategists, procurement heads, engineering directors and M&A teams, the full study goes beyond high-level forecasting to provide operationally actionable deliverables, including:

Explosion Proof Control Cabinet Market

- Scenario-based revenue and demand models that link end-user capex cycles (oil & gas, petrochemicals, mining, pharmaceuticals, industrial manufacturing) to enclosure type choices and protection philosophies.

- A certification and regulatory matrix mapping ATEX, IECEx, IEC 60079 series, UL/NEMA pathways and practical timelines for multi-region approvals — with process recommendations to compress sequential approvals into parallel workstreams.

- Materials exposure analysis and procurement playbooks for stainless steel (including AISI 316L), aluminum and powder-coated steels — plus hedging strategies to mitigate input-price-induced margin erosion.

- Vendor evaluation frameworks and an acquisition target shortlist methodology tuned to the market’s moderate concentration profile.

- Technology adoption roadmaps for digital enablement (IoT sensors, condition monitoring, remote diagnostics) and purge/pressurization systems that optimize TCO for large enclosures and control rooms.

- Service and aftermarket monetization models — spare parts, certified retrofit kits, and long-term service contracts — that convert one-time sales into annuity streams.

- Practical implementation checklists for plant engineering teams covering enclosure selection, ingress protection, thermal management, and certification documentation to shorten approval cycles onsite.

Competitive landscape — what to watch in 2026

The market is characterized by a mix of global platform providers, specialized hazardous-area manufacturers and regional OEMs. Key strategic takeaways for 2026:

- Global platform players (e.g., ABB) are leveraging breadth — standardization across geographies, component ecosystems and new IoT-enabled product variants — to offer integrated system solutions and scale-driven pricing. Their recent launches of IoT-enabled explosion-proof control boxes signal a push to capture lifecycle-service revenue and remote-monitoring value.

- Specialized hazardous-area firms such as R. STAHL AG, ROSE Systemtechnik and Expo Technologies differentiate on technical depth: lightweight flameproof innovations, advanced Ex p purge systems, and full-system certifications. These firms are attractive partners for operators pursuing compact, high-performance enclosures or complex retrofit projects.

- Regional OEMs and integrators — including several established manufacturers across Europe and Asia — retain competitive advantage in local compliance, custom-engineering and faster delivery for region-specific projects. Their strength is particularly useful for rapid turnarounds and bespoke build-to-order programs.

- Strategic implications: Partnerships that blend global platform capabilities with local manufacturing footprint and niche technical expertise will be the highest-leverage route for 2026 market entry or expansion. M&A candidates that can fill either a certification gap, local presence, or a digital-service capability are viable value creators.

Regulatory and materials dynamics — a pragmatic lens

Regulation and raw materials form the operational constraints that most frequently derail delivery schedules and margin plans.

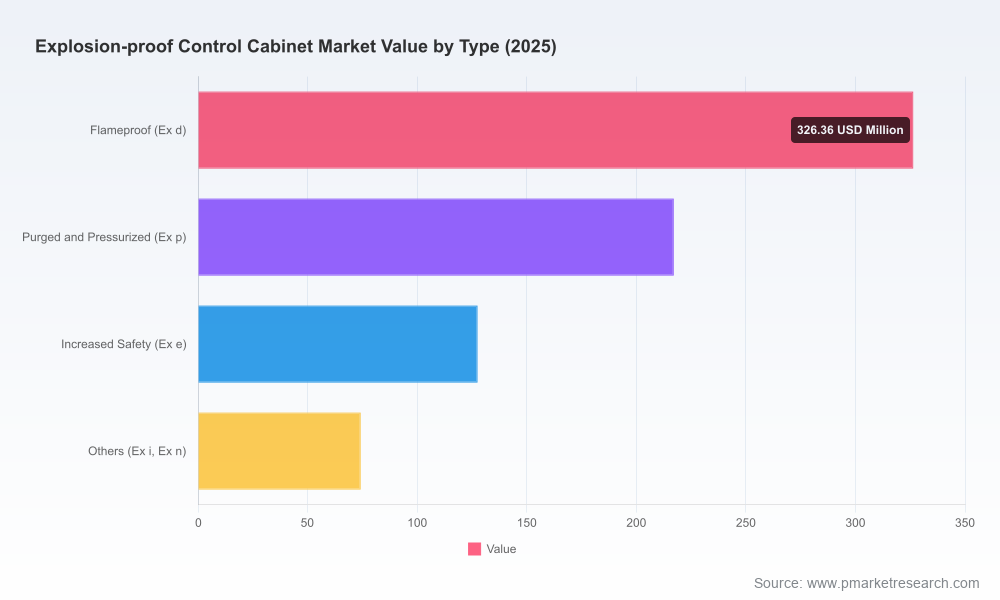

- Certification complexity: ATEX (mandatory in the EU) and IECEx continue to be the primary regulatory frameworks; the IEC 60079 family dictates protection methods such as flameproof (Ex d), increased safety (Ex e) and intrinsic safety (Ex i). Multi-region certification from the design phase reduces sequential testing and shortens time-to-market.

- Material selection and cost exposure: Stainless steel alloys — notably AISI 316L — are the default for corrosive and offshore environments. Price volatility in stainless steel and aluminum directly impacts manufacturing costs; our procurement playbooks recommend staged purchasing, strategic vendor alliances, and locked-price contracts for key projects initiated in 2026.

- Design strategy: Lightweight enclosure technologies and modular architectures (including EXpressure-type solutions and modular pressurized systems) lower transport and installation cost, reduce structural retrofitting need, and enable faster site acceptance, particularly for offshore and brownfield projects.

Technology and service trends to exploit

Several converging technology trends create tangible opportunities for product, service and business-model innovation:

- IoT and condition-based services: With key suppliers introducing IoT-enabled explosion-proof products, operators can monetize predictive maintenance, reduce unscheduled downtime and create service tiers that justify premium pricing.

- Purged and pressurized enclosures: For large control rooms and high-power equipment, Ex p systems are gaining traction as they reduce the need for heavy flameproof construction while maintaining safety — an important value proposition for capital-constrained projects.

- Retrofit kits and certified upgrades: The retrofit market for aging cabinets presents a significant near-term revenue pool. Standardized retrofit packages with clear certification roadmaps will win faster approvals and reduce total cost of ownership for asset owners.

- Aftermarket as an annuity: Spare parts, on-demand certified technicians, and long-term service agreements represent an under-penetrated channel to stabilize margins as product competition intensifies.

Top-line strategic recommendations for 2026

To translate market insights into concrete actions, PW Consulting recommends a prioritized playbook for 2026:

- Lock certification strategy early: Begin parallel certification tracks (ATEX/IECEx/UL where relevant) during the design phase to avoid sequential delays. Consider co-investment in certification testing with partners to share upfront costs and speed approvals.

- Hedge material exposure: Adopt staged procurement and strategic supplier contracts for stainless steel and critical components. Explore alternative material mixes where appropriate to reduce lead times without compromising compliance.

- Pursue modular product lines: Invest in modular, lightweight enclosure platforms and purge systems that reduce on-site installation complexity and appeal to retrofit programs.

- Monetize digital services: Bundle IoT-enabled monitoring and predictive maintenance into tiered service contracts to create recurring revenue streams and stickier customer relationships.

- Evaluate selective M&A and partnerships: Target acquisitions that fill certification gaps, expand local manufacturing in strategic markets, or add digital-service capabilities. Partnerships with specialized hazardous-area firms accelerate time-to-market for complex solutions.

Recent market movements to note

Market activity in 2025–2026 confirms the strategic themes above. Leading suppliers have updated portfolios with intrinsically safe and IoT-enabled offerings while specialist vendors continue to iterate on purge and lightweight Ex d technologies. These moves reinforce the bifurcation between scale players building integrated ecosystems and specialists pushing technical differentiation in niche segments.

How to use the full PW Consulting study

This release is a strategic preview. The full report includes the granular datasets, regional and application segmentation, supplier scorecards, and downloadable Excel models that underpin these conclusions. It also contains detailed methodological notes, risk-scenario simulations and a market-entry toolkit tailored to procurement, engineering and corporate development teams.

Accessing the complete study will enable you to:

- Run bespoke demand simulations for your project pipeline and test sensitivity to input-cost shocks;

- Retrieve vendor-specific capability matrices and certification timelines to support supplier selection;

- Identify high-probability retrofit and upgrade targets by plant age and asset class;

- Download templates for RFPs, certification checklists and procurement schedules keyed to shorten approval and delivery cycles.

Final perspective

For organizations making capital and sourcing decisions in 2026, the Explosion Proof Control Cabinet market presents both growth opportunity and execution risk. Growth is underpinned by long-term safety-driven demand and increasing acceptance of modern enclosure strategies, while execution risk centers on certification complexity and material-price volatility. PW Consulting’s report turns market-scale projections — including a clear CAGR of 6.45% from the 2026 baseline onward — into a tactical roadmap for capturing share and protecting margins. For full segmentation, supplier-level datasets and executable playbooks, please consult the complete report on our website.

For detailed analysis of this topic, please visit the official page:Explosion Proof Control Cabinet Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com