FGFR Inhibitor Drug Market: Insights and Competitive Analysis

Other |

2026-04-28 09:34:20

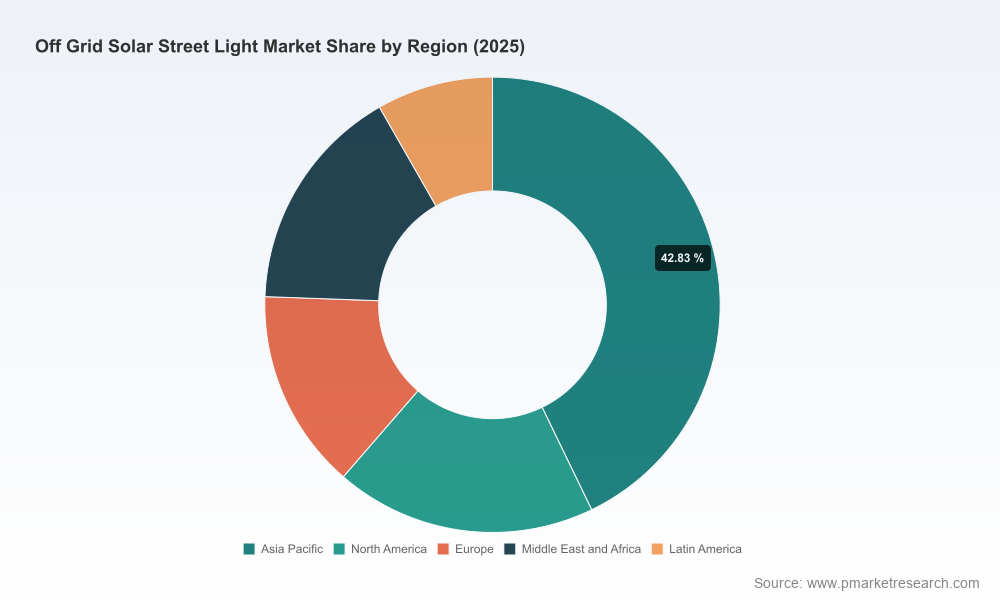

The off-grid solar street light market has moved from niche sustainability projects to a mainstream infrastructure play. Our latest market model (base year 2025; historical window 2020–2025; forecast horizon 2026–2032) shows a clear and sustained expansion: the global market rose from approximately USD 1.67 billion in 2020 to USD 2.45 billion in 2025 and is projected to reach roughly USD 4.19 billion by 2032. This trajectory implies a compound annual growth rate (CAGR) of about 7.95% across the forecast window. For corporate strategists, procurement leads, and investors planning activity in 2026, these broad-market dynamics create both opportunity and risk — and they require disciplined, data-driven responses.

Off-Grid Solar Street Light Market

Policy and incentive inflection points — 2026 is the first full-year after several material changes to US residential and commercial tax incentives for distributed solar. The termination of certain residential credits and the timing requirements tied to commercial investment tax credits (ITC) mean project economics will shift for some buyers and financiers. Organizations that understand how these deadlines affect clustered project cashflows will be advantaged in procurement and financing cycles through 2027.

Off-Grid Solar Street Light Market

Raw-material dynamics — commodity inputs that feed off-grid lighting systems are in flux. Recent price moves in polysilicon and LiFePO4 cathode materials are reducing pressure on module costs while creating short-term volatility in battery stack pricing. For product OEMs and system integrators, this creates a window to re-source balance-of-system components and to re-price competitive offers without undermining margin.

Off-Grid Solar Street Light Market

Unit economics and product evolution — commercial-grade off-grid solar street lights in the current market typically trade in a wide unit-price band depending on specification and battery capacity. That pricing dispersion reflects divergent product architectures (integrated all‑in‑one vs. split systems), lifecycle warranties, and digital/controls features. 2026 will be a year in which buyers increasingly demand total cost of ownership (TCO) guarantees rather than headline unit prices.

This report was built for practitioners who must make or influence procurement, product, manufacturing, or investment decisions in 2026. We intentionally designed the deliverables to be operational and decision-centric, not merely descriptive.

Market sizing & scenario engine — a transparent top‑down and bottom‑up model covering 2020–2032, including alternative scenarios for commodity trajectories, policy outcomes, and feature-adoption rates.

Buyer personas and procurement checklists — granular procurement criteria and evaluation rubrics that accelerate RFP development and vendor due diligence without guesswork.

CapEx/Opex and lifecycle models — configurable TCO templates that allow buyers and project financiers to test warranty terms, replacement cadence, and battery chemistry assumptions.

Supply-chain heat maps — end‑to‑end supply chain visibility highlighting chokepoints, alternative sourcing corridors, and lead‑time sensitivities for cells, batteries, electronics, and poles.

Competitive playbooks — standardized vendor scorecards, go‑to‑market tactics, and pipeline-acceleration ideas tailored to three archetypal provider strategies (premium-integrated OEM, project-focused integrator, and low-cost volume supplier).

Bankability and tender templates — document packs that speed up finance approvals and public-sector procurements, including risk matrices, acceptance tests, and performance-bond frameworks.

Investment and M&A diagnostic — composite valuations, consolidation scenarios, and operational levers that cut through headline multiples to show where value creation can be engineered.

The market remains fragmented, with the top three providers representing under one third of global share and the top five controlling well under half — a structural characteristic that shapes competitive strategy. Fragmentation creates room for both focused scale plays and premium-differentiation strategies.

Fonroche Lighting America (USA) — specializes in resilient all‑in‑one systems with embedded AI-driven power management. Its product-centric R&D focus makes it a go-to for clients prioritizing intelligent autonomy and remote asset management.

SEPCO Solar Electric Power Company (USA) — legacy experience in high‑power, commercial off‑grid systems positions it well for heavy-duty municipal and remote industrial projects where ruggedness and high lumen output are required.

Greenshine New Energy (USA) — a commercial-grade manufacturer whose assets were the subject of an acquisition in early 2026; the deal underscores ongoing consolidation among producers targeting scale and expanded distribution capability.

Solar Lighting International (USA) — known for high-lumen outdoor lights engineered for off‑grid performance, the firm is an example of a play that competes on system efficiency and warranty terms.

Sunna Design (France) — European provider emphasizing advanced energy management and intelligent controls, representing the premium, software-enabled edge of the market.

EnGoPlanet, Streetleaf, ClearWorld, Solar Street Lights USA and HeiSolar — these companies illustrate a range of approaches from US-made sustainability claims to scalable Chinese manufacturing; each pursues slightly different value propositions across reliability, manufacturability and cost.

Notable recent industry moves include new product launches tailored to arterial road applications, strategic asset acquisitions aimed at securing manufacturing continuity, and field deployments demonstrating resilience in tropical environments. These activities signal that vendors are optimizing for performance differentiation, channel expansion, and proof‑point driven sales.

Integrated systems and digital services — suppliers who combine robust hardware with remote management, predictive maintenance, and data monetization options will capture incremental margin and accelerate procurement approvals.

Battery strategy — with recent price adjustments for LiFePO4 cathodes and ongoing debate about long-term chemistries, astute sourcing strategies—such as multi-supplier qualification and forward contracts—will preserve margin and ensure delivery timelines.

Component commoditization and BOM optimization — declining module costs driven by wider polysilicon availability open a margin arbitrage for manufacturers that can reengineer systems to reduce weight, shipping cost and installation complexity.

Procurement sophistication — buyers are moving toward performance-based contracting and lifecycle KPIs. Vendors that can demonstrate bankable performance over multi-year cycles will outcompete low-price bidders in most institutional tenders.

For OEMs and manufacturers: prioritize modularity and digital enablement. Offer clearly tiered warranties and data‑backed performance guarantees. Hedge battery exposure via multi-chemistry sourcing and consider strategic partnerships with local integrators to shorten delivery timelines.

For project developers and municipal buyers: require TCO and bankability tests in RFPs rather than relying on nominal unit pricing. Use the report’s tender templates and acceptance tests to reduce counterparty and operational risk.

For financiers and private investors: focus on consolidation targets that either control distribution in specific geographies or own differentiated IP in energy management. Fragmentation creates multiple roll-up targets, but due diligence must stress lifecycle performance and warranty provisioning.

For suppliers seeking to expand: pursue demonstrable field pilots alongside municipal partners and create clear bundles (hardware + O&M + analytics) that allow predictable recurring revenue streams.

The PW Consulting Off‑Grid Solar Street Light Market report is intentionally tactical. It equips teams with models, checklists and negotiation levers that convert market outlook into executable 2026 plans. We present vetted vendor scorecards, configurable CapEx/Opex models, and scenario analyses that let you stress-test bids against commodity swings and policy shifts. To preserve competitive value for our clients, detailed segment-level matrices and proprietary price schedules are published in the full report and supporting datasets.

If you are shaping procurement strategy, planning product roadmaps, evaluating acquisitions, or underwriting projects this year, the report will shorten your decision cycle and reduce execution risk. Visit the PW Consulting publications page to request access to the full dataset, vendor scorecards, and the interactive scenario engine — these deliverables contain the granular, segment‑level intelligence you will need to finalize 2026 commitments.

For detailed analysis of this topic, please visit the official page:Off-Grid Solar Street Light Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com