Why Is Bakery Premixes Market Gaining Popularity Among Commercial Bakers and Home Consumers?

Networking |

2026-06-04 10:11:22

As organizations across pharmaceuticals, electronics, automotive, aerospace, and specialized industrial testing increase investment in controlled‑environment validation, the walk in humidity chambers market is entering a phase of steady, measurable expansion. Our latest market study — grounded in data from 2020–2025 and forward‑looking through 2032 — confirms that the industry is no longer niche: the global market size reached approximately USD 566.5 Million in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of roughly 6.3% through the 2026–2032 horizon, approaching the high‑eights in annual revenue by 2032.

Walk In Humidity Chambers Market

This PW Consulting market brief is crafted as a strategic “preview trailer” for corporate leaders, R&D heads, procurement officers, and private equity teams who must make near‑term capital and technology choices with multi‑year implications. It surfaces the essential directional signals — technology trajectories, regulatory pressures, supply vulnerabilities, and competitive moves — while preserving the report’s detailed segmentation tables and proprietary forecasts behind our research portal for clients and subscribers.

Walk In Humidity Chambers Market

Capital cycles: Many end users who delayed lab and test‑facility upgrades during the prior economic cycle will enter replacement and expansion programs in 2026, turning equipment choices from tactical procurements into strategic platform decisions.

Walk In Humidity Chambers Market

Regulatory tightening: Evolving expectations for pharmaceutical and medical device stability testing, coupled with stringent accreditation requirements (FDA, GMP, ISO 17025, ICH guidelines), are driving demand for higher‑fidelity, auditable environmental control systems.

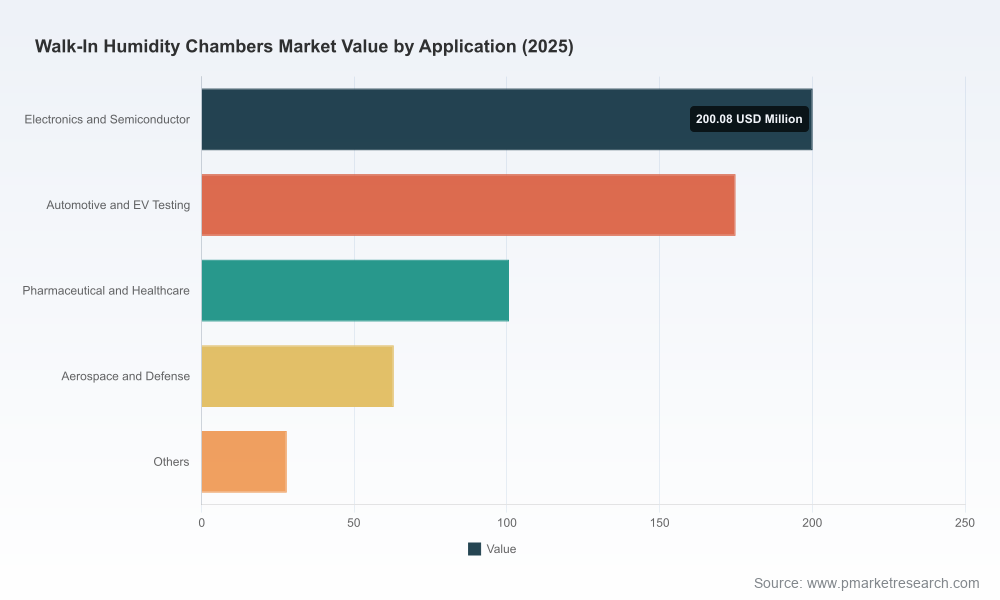

Cross‑sector demand drivers: Long‑duration battery testing for EVs, reliability testing for electronics and semiconductors, and mission‑critical aerospace qualification all require larger, more energy‑efficient walk in solutions — creating sustained, multi‑industry pull beyond single vertical booms.

The market’s mid‑single‑digit CAGR masks uneven, opportunity‑rich pockets: technological upgrades, service ecosystems, and customization capability are creating outsized margins for suppliers who can bundle lifecycle services with equipment sales. Our top‑level projection: from an estimated USD 566.5 Million in 2025, the market is set to expand to a projected USD 868.9 Million by 2032 under a baseline 6.3% CAGR scenario. This pace reflects both continued capital spending in core industries and incremental growth driven by energy efficiency retrofits and aftermarket services.

Concentration metrics indicate a moderately fragmented landscape — the largest three and five players together control a meaningful but not dominant share of revenue, leaving clear room for regional specialists, OEMs with deep application know‑how, and new entrants offering differentiated value propositions (e.g., low‑carbon operation, rapid‑deployment modular chambers, or SaaS‑integrated monitoring).

Regulatory compliance and validation: Pharmaceutical stability testing dictated by ICH protocols and broader regulatory expectations is a stable, highly specific demand source requiring reproducible temperature and humidity performance and traceable data logging.

Cross‑industry reliability testing: Electronics, semiconductors, batteries, and automotive components increasingly rely on large‑format, repeatable environmental testing. These sectors prioritize modularity, test repeatability, and the ability to simulate extended duty cycles.

Energy efficiency pressure: Energy costs and sustainability targets push buyers toward high‑efficiency system designs and retrofits — a source of differentiation for vendors that can quantify life‑cycle cost savings.

Supply‑chain fragility: Critical inputs — stainless steel interiors, specialized insulation, high‑performance compressors, and precision humidity sensors — are concentrated in specific supplier clusters, creating procurement risk that can delay lead times or inflate costs unless actively mitigated.

Service and aftermarket opportunity: With equipment lifecycles measured in decades, service contracts, calibration, and retrofits represent recurring revenue streams that can materially lift supplier margins.

The vendor pool is a mix of long‑established European engineering houses, North American specialty fabricators, and Asia‑based OEMs with global reach. Our analysis highlights several archetypes and actionable indicators for vendor selection and M&A scouting:

BINDER GmbH (Tuttlingen, Germany): A strong ICH‑focused offering, enhanced in 2025 by its acquisition of a well‑known humidity‑room specialist. This move signals consolidation within the ICH/stability segment and provides BINDER with an expanded portfolio and access to complementary go‑to‑market channels.

Russells Technical Products (Holland, MI): Known for modular, heavy‑duty construction — suited to labs and OEM testing facilities that require custom layouts or drive‑in capability. Their strength lies in engineering flexibility.

Weiss Technik North America (including CSZ brand): A broad, customizable catalog and geographic expansion plans (facility increase in 2026) position them to capitalize on large institutional tenders and multi‑site rollouts.

Associated Environmental Systems (AES): Recent expansion of manufacturing capacity reflects demand scaling; AES offers both removable‑panel and permanent structural builds, an advantage for customers with diverse site constraints.

Darwin Chambers and Parameter Generation & Control (A BINDER company): Both emphasize pharmaceutical GMP and stability applications; Darwin stresses energy efficiency and GMP storage, while the recently integrated Parameter brand emphasizes fast‑delivery standard rooms and ICH compliance.

Testron Group and Wewon (China): Competitive cost structures combined with growing international support networks make these manufacturers an option for customers seeking rapid customization and competitive pricing, especially for large‑format chambers.

Recent strategic moves — notably BINDER’s July 2025 acquisition of a specialized humidity‑room maker, AES’s headquarter expansion in late‑2025, and Weiss Technik North America’s facility ramp in 2026 — signal two concurrent trends: consolidation around regulated pharma capabilities, and capacity expansion to meet broader industrial demand. For buyers, these moves are a cue to re‑evaluate supplier stability, lead‑time risk, and the total cost of ownership offered by vendor portfolios.

Our comprehensive report is structured for immediate operational application rather than academic reading. Key components include:

Proven procurement playbook: step‑by‑step guidance for RFP design, performance specifications (including sensor accuracy, dew‑point control, and environmental uniformity metrics), bid evaluation templates, and supplier scorecards.

CapEx vs. life‑cycle cost models: customizable calculators that let procurement and finance teams model purchase price, installation, energy consumption, maintenance, calibration, and decommissioning costs over 10–15 years.

Risk register and mitigation toolkit: practical actions to reduce raw‑material exposure, diversify compressor and sensor sourcing, and design contracts to protect delivery schedules and warranty enforcement.

Regulatory compliance matrix: mapping of ICH, FDA, GMP, ISO 17025 and CE requirements to specification checklists and validation protocols — invaluable for pharma, biotech, and medical device customers.

Aftermarket and services playbook: revenue models for vendors and a service‑procurement guide for buyers covering calibration intervals, remote monitoring services, and retrofit pathways to improve energy efficiency.

Scenario‑based forecasts: three demand scenarios (baseline, upside, downside) that allow strategists to stress‑test capacity plans, pricing strategies, and M&A timing through 2032.

For manufacturers and OEMs: prioritize modular designs and fast‑delivery product lines to capture replacement cycles and short‑lead institutional bids; invest in sensor supply security and software integration to upsell monitoring services.

For laboratory owners and procurement teams: adopt lifecycle cost assessment in specifications; include energy‑efficiency and remote monitoring requirements as pass/fail criteria to avoid short‑term capital price competition that increases long‑term operating costs.

For investors and M&A teams: target firms that combine regulatory depth (pharma/GMP competency) with service‑oriented aftermarket offerings — recent consolidation events validate this premium. Be skeptical of players heavily leveraged on commoditized product lines without service ecosystems.

For regulators and standards bodies: anticipate that the next wave of product innovation will blend hardware with data services; consider guidance that addresses digital traceability and cyber‑secure remote monitoring of environmental test assets.

Walk in humidity chambers are transitioning from equipment purchases to strategic platform investments. The market’s steady growth trajectory through 2032 presents both predictable demand and meaningful shifts: consolidation around regulated niches, expansion of manufacturing footprints, and a clearer split between commodity suppliers and high‑value platform providers. In 2026, decisions made by buyers and investors will determine who captures the recurring revenue of aftermarket services and who remains in one‑off equipment sales.

PW Consulting’s full Walk In Humidity Chambers Market report translates these dynamics into executable strategies, validated models, and vendor‑level intelligence. Access to the report provides the granular segmentation, financial models, and vendor scorecards needed to convert the directional insight above into procurement specifications, capital allocation, and M&A roadmaps.

For detailed analysis of this topic, please visit the official page:Walk In Humidity Chambers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com