Biosimilar Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-08 12:02:43

As organizations reset capital and supply-chain priorities for 2026, the vertical rotary surface grinders market provides a clear case where disciplined strategy translates directly into margin and time-to-market advantages. PW Consulting’s latest market study — built on a 2020–2025 historical base and a 2026–2032 forecast horizon — shows a market that has grown from roughly USD 1.9 billion in 2020 to about USD 2.58 billion in 2025, and that is projected to expand at a compound annual growth rate (CAGR) of 5.59% through 2032. By 2032 the market is expected to approach roughly USD 3.78 billion under the base scenario.

Vertical Rotary Surface Grinders Market

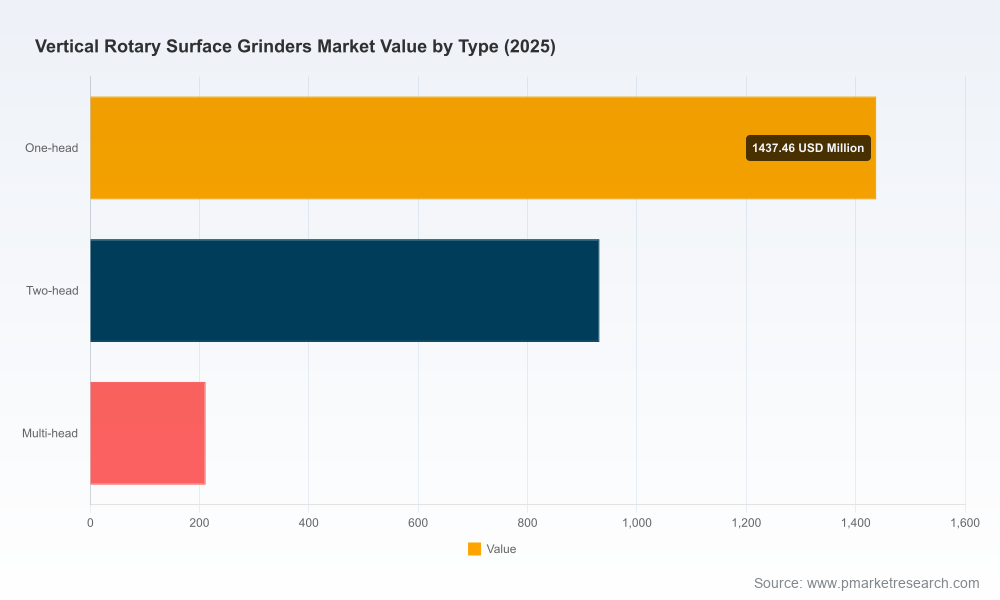

This briefing pulls forward the parts of the research that matter most to executives making 2026 budget, sourcing, and product decisions. It highlights the strategic implications of the market trajectory, competitive positioning of key OEMs, and the near-term risks tied to raw material and trade policy. We deliberately stop short of publishing the granular segment tables and regional splits here: that data lives in the full report and is available via the PW Consulting portal for decision teams that need the underlying drivers and numerical detail.

Vertical Rotary Surface Grinders Market

Growth profile: The market’s steady mid-single-digit CAGR masks important structural shifts — quality- and productivity-led replacements in aerospace and toolmaking, capacity additions to support reshoring in critical industries, and increasing aftermarket/service revenue opportunities as machine owners seek to extend asset life.

Vertical Rotary Surface Grinders Market

Timing for 2026 decisions: With momentum established through 2025 and predictable growth through 2032, 2026 is a pivotal year for capital allocation. Decisions made this year about machine purchases, remanufacturing partnerships, and digital retrofit pilots will determine competitive position across the next replacement cycle.

Margin levers: Supplier selection, contract terms for steel and specialty materials, and service model design (warranty, predictive maintenance, rebuilds) will have outsized impacts on total cost of ownership (TCO) and aftermarket margins. Executives who reorganize procurement and aftermarket into coordinated profit centers will capture disproportionate value.

PW Consulting’s Vertical Rotary Surface Grinders Market report is built for hands-on use by strategy, procurement, and operations teams. Key deliverables include:

Transparent market sizing and growth scenarios: methodology, assumptions, and sensitivity tests that let you map outcomes to your internal forecasts.

Demand driver analysis: end-market adoption patterns (industrial, tool & die, aerospace), technical requirements, and cycle-timing that guide procurement windows and product roadmaps.

Supplier benchmarking framework: qualitative and quantitative scoring across product breadth, capacity, quality, aftermarket capability, and delivery performance — structured so you can run an RFP with comparable metrics.

Technology and product matrix: comparative evaluation of vertical spindle architectures, hydrostatic turntables, spindle-power trade-offs, and automation readiness — with recommended architectures for three buyer archetypes (high-throughput, high-precision, cost-conscious).

Cost build-up and scenario modeling: bill-of-materials sensitivity (including steel and precision components), freight and tariff implications, and unit economics for new vs remanufactured machines.

Aftermarket and service playbook: service-pack design, pricing elasticity models, and KPIs to track ARPU and lifetime value of installed machines.

Risk heatmap and mitigation playbook: supply-chain, regulatory, and commodity shocks mapped to practical mitigation steps and monitoring triggers.

Each section contains templates, checklists, and negotiation playbooks you can operationalize immediately — while the core segment tables and regional allocations are provided in protected appendices for clients needing the full numeric granularity.

The sector is moderately concentrated. The top three suppliers account for a meaningful share of the market, and the top five amplify that concentration. This concentration creates a supplier dynamic where scale, aftermarket reach, and service networks are decisive.

Bourn & Koch, Inc. (Rockford, Illinois) — A legacy OEM with a strong reputation for heavy-capacity Blanchard-style vertical rotary grinders. Their emphasis on heavy stock removal and large-diameter chucks makes them a natural partner for customers where throughput and durability are mission-critical. Expect continued demand for new and remanufactured Blanchard models among shops expanding capacity.

DCM Tech (Winona, Minnesota) — Focused on American-made rotary grinders across a wide capacity range. Their positioning resonates with buyers prioritizing domestic content and fast aftermarket support; they remain a logical supplier for aerospace and precision-heavy industrial users.

Chevalier Machinery (Taiwan / USA) — Notable for hydrostatic turntable platforms and an emphasis on rigidity. Chevalier’s product innovations (including recent FRG series introductions) make them a compelling option for high-precision customers evaluating the performance upside of hydrostatic systems.

Okamoto Corporation (Japan) — Known for high-accuracy rotary tables and powerful spindles. Okamoto’s strength lies in precision rotary models that appeal to toolmakers and manufacturers of tight-tolerance components.

Tong Yi / Dowell and Indian OEMs (Alex Machine Tools, Synergy, ABL) — These manufacturers deliver a breadth of cost-competitive options and have become increasingly active in regional trade shows and targeted markets. Their evolving product quality and local service networks are reducing historical barriers for buyers in cost-sensitive segments.

Kent USA — Positioned for niche use-cases (hard/brittle materials, molds), Kent’s machines are chosen where robustness and a specialized construction approach outweigh lower-cost alternatives.

Recent market moves underscore three dynamics: (1) OEMs are expanding show-floor visibility and regional support (e.g., trade-show participation and installations), (2) product upgrades emphasizing hydrostatics and higher spindle power are increasingly used to differentiate, and (3) demand for remanufacturing and installed-base monetization continues to rise as owners seek lower TCO.

Raw materials: Steel coil costs climbed materially in 2025, with industry reporting increases in the mid-single to low-double-digit percentage range. This single factor compresses margins for machine builders that have not adjusted pricing or hedging strategies.

Trade policy: Ongoing national security investigations into machine tool imports and the potential for significant tariffs on steel and specialty materials create a meaningful procurement risk. Several markets have seen proposed or implemented tariff measures that can materially change landed cost calculations overnight.

Operational impact: These inputs increase the economic attractiveness of local sourcing and remanufacturing. Organizations that proactively redesign sourcing strategies, employ forward contracts, or accelerate localization can protect margins and lead times.

For executives planning capital and supply decisions in 2026, PW Consulting recommends a focused set of actions:

Run a TCO rebasing exercise: Update your cost models for machine purchases to include realistic steel-price and tariff scenarios; treat 2026 procurement as a rolling negotiation rather than a fixed-price event.

Segment procurement by use-case: Define separate procurement strategies for high-throughput, high-precision, and cost-sensitive lines. Match supplier capabilities (hydrostatic tables, high HP spindles, remanufacture offerings) to these buckets.

Lock in aftermarket and service terms: Negotiate multi-year service agreements and rebuild windows that align incentives between OEMs and owners; quantify the value of guaranteed uptime and quicker spares delivery.

Pursue selective local partnerships: Where tariffs and supply risk are material, prioritize partnerships or licensing relationships with local producers to shorten lead times and reduce landed risk.

Pilot digital retrofits: Deploy condition monitoring and predictive maintenance pilots on a subset of the installed base to immediately reduce downtime and gather operating data for broader rollouts.

Use the market concentration dynamics: For buyers, the presence of a few scale players creates leverage—use competitive RFQs and bundled aftermarket opportunities to extract better commercial terms.

This briefing is designed to be a practicable trailer: it outlines the strategic shape of the vertical rotary surface grinders market and provides the playbook you need to start acting in 2026. The full PW Consulting report contains the underlying segment tables, regional allocations, supplier scorecards, and downloadable templates that empower procurement, product, and M&A teams to execute against the recommendations above.

For teams preparing 2026 budgets and strategic plans, accessing the full dataset and model is essential. Visit the PW Consulting report page to obtain the complete study and the editable scenario models that accompany it.

— PW Consulting, Senior Strategic Advisor & Chief Industry Analyst

For detailed analysis of this topic, please visit the official page:Vertical Rotary Surface Grinders Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com