Revolutionizing Machine Learning Workflows The Rise of AI Model Directories

Technology |

2026-04-20 13:43:45

As fleets, OEMs, charge point operators (CPOs) and energy retailers recalibrate strategies for the next tranche of EV deployments, the EV charging card market has evolved from a convenience accessory into a strategic layer of access, billing and data capture. PW Consulting’s latest market study shows that the global EV charging card market is entering a phase of accelerated scaling: overall market value climbs from USD 1,345.5 Million in 2025 to USD 4,347.4 Million by 2032, reflecting a compound annual growth rate of 18.24% over the 2026–2032 forecast window. That trajectory creates both near-term commercial opportunities and medium-term strategic risks for incumbents and new entrants alike.

Ev Charging Card Market

Regulatory momentum converges with infrastructure build-out. Policy actions such as the EU AFIR requirements and refreshed U.S. guidance under the NEVI Formula Program are materially increasing public fast-charger coverage and—critically—demanding interoperable access methods. This elevates charging cards from a localized product to a cross-border interoperability enabler.

Ev Charging Card Market

Network densification and hardware scale change the economics of access. In markets where operators are adding thousands of DC fast ports year-on-year, the marginal value of seamless authentication, frictionless payments and roaming agreements rises sharply; charging cards are often the lowest-friction instrument to monetize that value for heterogeneous user populations.

Ev Charging Card Market

Supply chain and cost pressures are reshaping platform choices. Tariffs and onshoring incentives are altering procurement and deployment economics for stations and back-end hardware, which in turn affect how providers prioritize card versus app-based authentication strategies.

The headline market expansion — roughly tripling in size from a mid‑market base in 2025 to multi‑billion levels by 2032 — is not uniform, but it is structurally supported by three persistent forces: rapid EV fleet electrification, public fast-charging proliferation, and the migration of fleet and commercial customers to contract-based billing. For strategy teams, the implication is straightforward: product roadmaps and commercial models that assume slow, incremental uptake risk missing a compressed window of high-margin opportunity.

Interoperability mandates and roaming economics: Standardization pressures are increasing the value of multi-network access instruments. Whether via RFID, smart cards or tokenized credentials, the ability to present a single corporate or consumer credential across networks is becoming a procurement criterion for large fleets and mobility-as-a-service (MaaS) buyers.

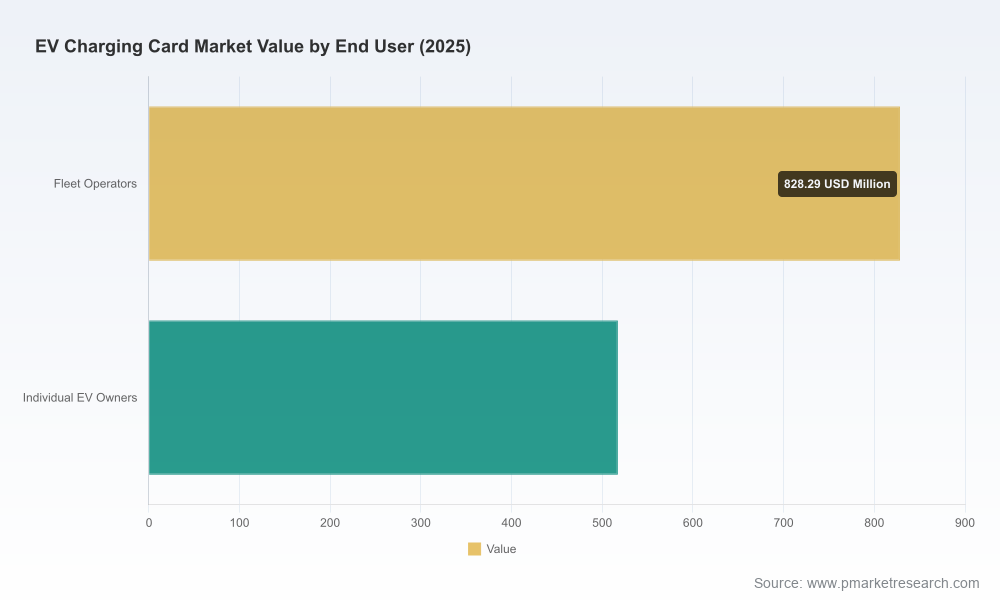

Fleet monetization and operational telemetry: Fleet operators are shifting from simple access cards to integrated solutions that combine authentication with detailed session telemetry, driver-level billing and automated reconciliation. The commercial premium for that integration is growing faster than the consumer card business.

Price and installation dynamics: High variability in station build costs—especially for high-power DC sites—means that operators are emphasizing utilization and predictable revenue streams. Charging cards that enable subscriptions, roaming margins or bundled billing are therefore strategically attractive.

Channel convergence between hardware and software providers: As charge-point hardware vendors deepen software stacks, the competitive boundary between issuing cards and delivering cloud billing/authentication services is blurring. Strategic partners and acquisitions will determine who captures recurring revenue.

The market exhibits moderate concentration: five leading players account for just over half of current commercial activity, a structure that supports both consolidated roaming agreements and room for regional specialists. The competitive set can be understood as a mix of platform incumbents, energy retailers, mobility-focused challengers and infrastructure OEMs. Each archetype exhibits different strategic advantages:

Platform incumbents (e.g., ChargePoint, EVgo, Blink Charging) — strengths are scale of network, established B2B relationships and payment flows. These players benefit from integrated backend systems that make card issuance and reconciliation straightforward at scale.

OEM-integrated players (e.g., Tesla) — control over a proprietary network and integration with vehicle UX enables a differentiated, often higher-margin experience. The trade-off is limited openness to non-proprietary roaming unless commercial arrangements are struck.

Energy and retail brands (e.g., Shell Recharge, Octopus Energy, Fortum) — command over retail sites and brand trust creates opportunities to bundle energy plans, loyalty and charging access into card products that drive repeat usage.

Infrastructure OEMs (e.g., ABB, Siemens) — hardware platform compatibility and enterprise-grade security are their leverage points; they are well positioned to sell card-enabled systems as part of turnkey deployments.

Regional aggregators and enablers (e.g., Radius, E-Flux, Tata Power) — specialize in multi-network billing and regional roaming; their value is in stitching together fragmented networks, particularly where roaming standards are still coalescing.

Network protocol expansion and connector standard transitions: Recent operator pilots and rollouts to support NACS connectors (notably EVgo’s expanded NACS footprint) are accelerating cross-compatibility for a growing vehicle fleet. This raises the strategic priority of cards that can be mapped to multiple connector ecosystems and billing back-ends.

Product innovations in emerging markets: Regional rollouts such as Tata Power’s RFID-enabled EZ CHARGE card demonstrate how simple, secure tap-and-go credentials can boost utilization in high-growth markets. Fast rollouts in markets with dense OEM fleet growth will set the commercial benchmarks for card adoption.

For CPOs and network operators: Prioritize interoperable credential stacks and open APIs now. Negotiating roaming partnerships and joining clearing houses early will preserve margin and prevent later revenue leakage as large fleets demand consolidated invoicing.

For energy retailers and utilities: Use charging cards as a customer-acquisition and retention lever. Packaging access with tailored energy tariffs, demand response credits and loyalty programs will create defensible recurring revenues.

For hardware vendors and integrators: Embed modular authentication support in chargers (RFID/NFC-capable readers and secure element support) and offer optional managed billing for customers who prefer OPEX over CAPEX buying patterns.

For mobility, fleet and logistics operators: Make multi-network roaming and driver-level reconciliation a procurement requirement. The cost of operational complexity will outweigh the marginal premium for proprietary-only access in markets with heterogeneous networks.

For new entrants and fintechs: Focus on the reconciliation and settlement layer rather than competing on card issuance alone. The highest-margin, defensible product is often the billing and clearing service that sits behind multi-network authentication.

Our full PW Consulting report is built as an operational playbook for 2026. Key elements include:

Transparent market-sizing and methodology — detailed baseline and forecast models covering 2020–2032 with scenario analyses and sensitivity testing for policy, technology and price inputs.

Commercial playbooks — step-by-step guidance for issuing, distributing and monetizing charging cards, including pricing templates, contract archetypes and settlement flows for multi-network reconciliation.

Technology assessment — vendor-neutral evaluation of authentication technologies (RFID, NFC, tokenization, mobile-first) with implementation risk matrices and security checklists for payment compliance.

Regulatory impact analysis — targeted country-by-country briefs on AFIR, NEVI and national procurement rules with recommended commercial responses to accelerate deployments while managing compliance risk.

Competitive benchmarking — strategic profiles of global and regional players, partnership maps, and acquisition/partner fit scorecards to inform M&A and alliance strategies.

Go-to-market templates — partnership frameworks for CPOs, energy retailers, fleet operators and OEMs that translate strategy into 90‑, 180‑ and 365‑day execution plans.

Embed market scenarios into capital planning: Use our high‑, base‑ and low‑take scenarios to stress-test investment in card programs versus app-only strategies, especially where station capex is high.

Re-assess partner economics before RFPs: Require partners to demonstrate roaming reach, settlement latency and reconciliation automation in RFPs. Those metrics materially affect operating margins and customer satisfaction.

Design product modularity now: Offer tiered card products (basic access, fleet telemetry, full reconciliation) that can be upsold as fleet needs evolve — this creates a predictable ARPU ladder.

Prioritize security and compliance: With cards increasingly used for business billing, ensure secure element support and PCI‑equivalent controls are in place before large fleet contracts are signed.

2026 will separate practitioners who treat charging cards as a tactical accessory from strategists who view them as an enduring layer of commerce and data capture in the EV ecosystem. PW Consulting’s full report delivers the granular segment models, partner maps and executable templates you need to convert the market’s headline growth into durable competitive advantage. This preview outlines the structural drivers and the practical choices ahead; the complete analysis contains the split-level data, market-share build-ups and detailed cost curves that are essential for final vendor selection, procurement and M&A diligence.

For executives building 2026 roadmaps: this is the strategic window. PW Consulting’s Ev Charging Card Market report equips you to act with evidence, move faster than competitors, and lock in recurring revenue streams as the market scales. Access the full dataset and implementation appendices on our report page for the detailed segment economics and company-level scorecards that underpin these conclusions.

For detailed analysis of this topic, please visit the official page:Ev Charging Card Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com