Microcars Market: Size, Share, and Future Growth

Other |

2026-06-04 07:14:27

The Short Circuit Fault Current Limiter (FCL) market is entering a decisive growth phase. Our new Short Circuit Fault Current Limiter Market report — built on five years of historical analysis (2020–2025) and forward-looking modeling through 2032 — shows the market expanding from a multi-hundred million USD base in 2025 to well over one billion USD by 2032, reflecting a compound annual growth rate (CAGR) of 8.21% across the 2026–2032 forecast window. For corporate strategists, investors, and grid operators, the period beginning in 2026 represents a narrow window to lock in technology choices, supplier relationships, and deployment pilots that will determine competitive positioning as demand accelerates.

Short Circuit Fault Current Limiter Market

Regulatory alignment crystalizes: Evolving grid codes and renewed emphasis on grid-forming capabilities, fault-ride-through performance, and harmonic/unbalance management are converging on timelines that require tangible vendor engagement and compliance roadmaps by 2026.

Short Circuit Fault Current Limiter Market

Renewables and inverter dominance: As inverter-based resources proliferate, their short-circuit characteristics change how networks respond to faults — turning FCLs from optional contingency devices into core elements of resilient meshed systems.

Short Circuit Fault Current Limiter Market

Commercialization thresholds: Several technology variants — from high-temperature superconducting (HTS) resistive designs to fast-acting solid-state solutions — are crossing validation and pilot thresholds. Validation milestones achieved in late 2024 and early 2025 signal that 2026 will be the year proofs-of-concept mature into repeatable field deployments.

Between 2020 and 2025 the market demonstrated steady expansion, driven by utility modernisation, legacy switchgear protection needs, and initial deployments in renewable-heavy networks. Our base-year analysis anchors 2025 as the commercial launchpad; our scenario modeling then projects consistent growth to 2032 under a central 8.21% CAGR assumption. For boards and business unit heads planning capital allocation and product roadmaps in 2026, three implications follow:

CapEx vs. Opex trade-offs matter: Procurement teams must weigh higher up-front technology premiums (particularly for superconducting and some power-electronic solutions) against lifecycle benefits —downtime reduction, deferred switchgear replacement, and improved interconnection capacity.

Layered procurement strategies mitigate risk: Staggered pilot-to-scale engagements, milestone-based contracting, and modular technology stacks reduce exposure to one-off supplier failures and accelerate learning curves.

Cross-functional readiness is required: Successful rollouts demand synchronized engineering, protection & controls, and asset-management teams — as well as legal/regulatory units to manage code compliance and interconnection agreements.

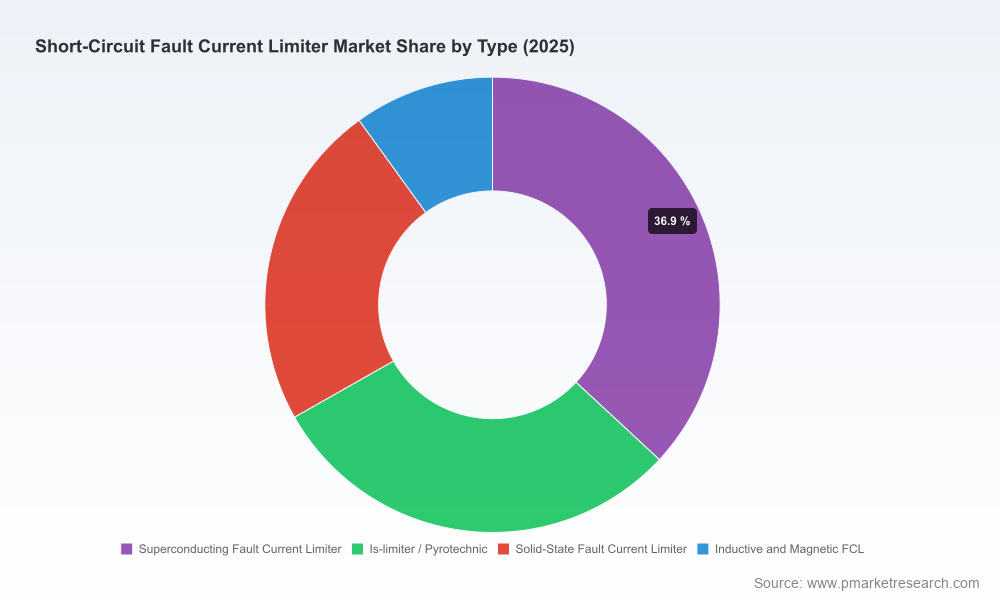

Our technology deep dives evaluate four archetypes of fault current limiting approaches, assessing maturity, deployment complexity, lifecycle economics, and integration risk. Key dynamics highlighted in the report include:

Superconducting FCLs (SFCL): Attractive for distribution and rail projects where compact footprint and high limiting ratios are required. HTS tape costs and cryogenic operation remain principal adoption levers; our sensitivity analysis shows total system economics are highly responsive to reductions in HTS conductor usage and cooling-system optimization.

Power-electronic/solid-state FCLs: Offer fast response and repeatable operation without cryogenics, suitable for applications prioritizing speed and modularity. Cost-per-MW is trending down with semiconductor advances, but complexity in protection coordination can raise engineering costs.

Pyrotechnic/IS-limiter and inductive/magnetic solutions: Proven in niche and legacy contexts for high-reliability interruption and simple mechanical implementations. Their role in mixed inverter–synchronous systems is evolving and often complementary to electronic or superconducting approaches.

Hybrid architectures: The most compelling near-term value propositions combine technologies (e.g., SFCLs paired with DC mechanical breakers for HVDC or offshore renewables), enabling both high limitation performance and improved fault-clearing coordination.

The market is moderately consolidated: the top three firms control a meaningful share of industry revenue, and the top five appear to hold a clear majority. This concentration pattern creates both barriers and strategic opportunities for new entrants and incumbents alike.

Large electromechanical and system integrators (e.g., ABB, Siemens Energy, Schneider Electric, Eaton) bring scale, global service networks, and deep protection-system expertise — critical for utility-scale rollouts and bundled protection-retrofit projects.

Specialist players (e.g., Nexans, AMSC, GridON, G&W) offer focused technology differentiation — notably in superconducting solutions, HTS wire supply chains, and tailored distribution-level devices that accelerate integration into rail, industrial, and private utility networks.

Regional manufacturers and power-electronic innovators (including LS Electric and several China-based suppliers) compete on rapid delivery cycles and cost-competitive designs for large domestic programs and export-focused projects.

The report includes vendor profiles, supplier scorecards, and a strategic partner matrix that maps technological strengths against deployment archetypes (utility, industrial, renewables, data center/marine) to help in shortlisting suppliers and forming strategic alliances.

Regulatory imperatives: Grid-code revisions, particularly those requiring fault-ride-through and controlled fault current contribution from inverter-based resources, elevate FCLs into mandatory deployment discussions for many interconnection projects.

Materials and cost dynamics: HTS tape pricing and availability remain pivotal for SFCL economics. Our report models cost-reduction trajectories for HTS conductor usage through design optimization and LN2-based cooling strategies, estimating break-even scenarios under multiple adoption pathways.

National investment programs: Large-scale transmission investments, notably in ultra-high-voltage (UHV) projects in major markets, create concentrated demand pockets where FCLs can defer switchgear replacement and enable renewables interconnection without costly asset changes.

Recent industry developments underscore the market’s transition from laboratory validation to field-viable solutions. Notable examples covered in the report include technology validation of resistive SFCLs integrated with DC mechanical breakers that demonstrated significant limitation in HVDC tests, and strategic alliances deploying superconducting FCLs in rail networks with self-recovery capabilities. These milestones materially de-risk the technology options for 2026 pilots and early deployments.

Beyond high-level forecasts, the report is built as a practitioner’s toolkit for 2026 decision cycles. Deliverables include:

Actionable market sizing and revenue scenarios (top-line and by broad segmentation buckets), with sensitivity tables for technology adoption, regulatory stringency, and HTS cost trends.

Vendor due-diligence templates and shortlist criteria aligned to procurement policies and O&M realities.

Technical integration checklists covering protection coordination, harmonics, and islanding considerations for renewables-heavy grids.

Investment cases and ROI models tailored to utility, industrial and renewable-integration stakeholders (including payback drivers and TCO assumptions).

Scenario planning and stress tests for supply-chain shocks (e.g., HTS tape availability) and regulatory shifts.

M&A and partnership playbooks for strategic growth — from bolt-on acquisitions of niche technology suppliers to joint R&D frameworks with system integrators.

Procurement leads should adopt a dual-track supplier engagement: secure pilots with specialists while negotiating framework agreements with Tier-1 integrators for scale deployments.

R&D and product teams need to prioritize modularity, interoperability, and reduction in conductor usage (for HTS designs) to expand addressable markets and shorten procurement cycles.

Investors and corporate development functions must treat FCLs as strategic leverages for asset-light grid services, considering both technology plays and service-based offerings (protection-as-a-service).

Regulatory and compliance teams should start mapping local code milestones to project timelines to avoid late-stage design rework and to capture incentive windows.

The FCL market has moved past technical feasibility into selective commercial maturity. While headline growth is compelling, the near-term winners will be those who combine technology insight, procurement discipline, and regulatory foresight. Our market concentration analysis signals meaningful opportunities for both incumbents to defend share and for nimble specialists to expand via focused partnerships. For any organization evaluating capital deployment, technology selection, or M&A options in 2026, this report provides a structured, operationally focused path from pilot to portfolio.

This preview highlights the strategic framing and practical content within our Short Circuit Fault Current Limiter Market report. To access the detailed segmentation tables, vendor scorecards, case-level financial models, and proprietary regional forecasts that underpin the executive recommendations above, please consult the full report available on our website. PW Consulting’s advisory team is available to run a tailored briefing for executive leadership and to co-develop a 12–24 month go-to-market or procurement roadmap.

For detailed analysis of this topic, please visit the official page:Short Circuit Fault Current Limiter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com