Europe Workforce Management Market Report: Industry Size, Share, Regional Trends, and Forecast by 2030

Other |

2026-05-28 09:24:22

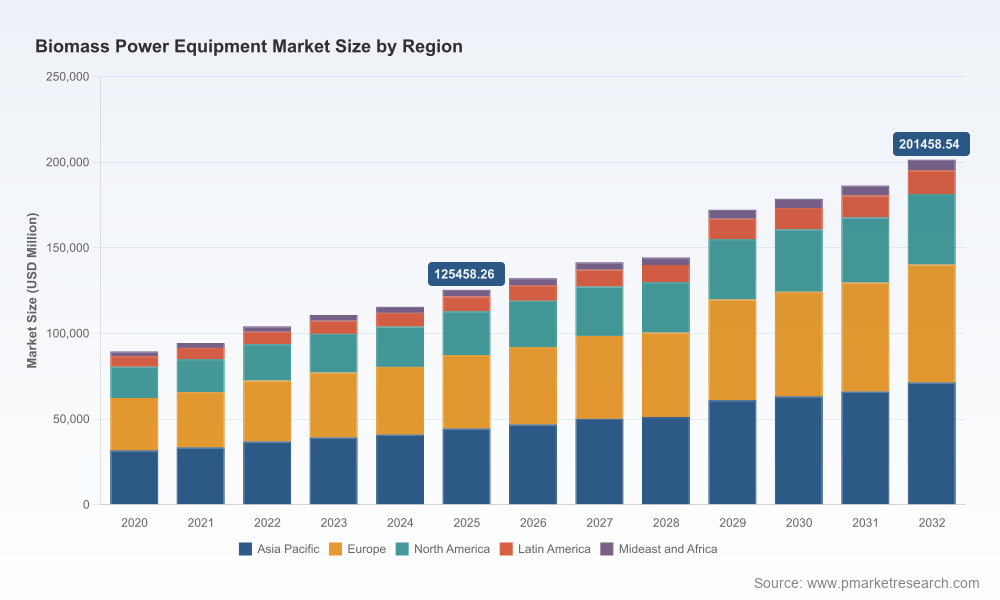

As global energy systems accelerate toward decarbonization, biomass power equipment remains a pragmatic bridge between legacy thermal generation and 100% renewable electricity systems. PW Consulting’s latest market study — based on a 2025 base year and covering historical performance from 2020–2025 with forecasts to 2032 — quantifies this transition and translates it into operational guidance for executives, investors, and project teams. The market stood at USD 125,458.26 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 6.99% through the 2026–2032 forecast window, underscoring a sustained capital cycle and multiple entry points for industry participants.

Biomass Power Equipment Market

Policy acceleration: In several major markets, new regulatory commitments and incentive frameworks are changing project economics. Examples include continent-level renewable targets that raise subsidy visibility and national tax provisions designed to de-risk capital deployment. These levers materially affect underwriting assumptions for projects initiated in 2026.

Biomass Power Equipment Market

Carbon price and arbitrage: Carbon pricing in major markets is materially higher than historical averages, reshaping fuel-choice economics and opening arbitrage opportunities for biomass-based generation, especially where co-firing and fuel-switching are feasible.

Biomass Power Equipment Market

Input-cost volatility: Raw material pricing — including market-referenced benchmarks such as wood pellet prices — and component-level capital costs (notably grate stoker systems and other core plant equipment) are central variables in project-level IRR models. These cost inputs have proven sensitive to logistics and supply-chain disruptions, making 2026 procurement strategies pivotal.

Technology differentiation: Improvements in combustion efficiency and modular gasification systems are altering the value equation between large-scale steam plants, fluidized bed solutions, and smaller gasifier-based installations. 2026 is when many investors will select architectures that balance CAPEX, fuel-flexibility, and future retrofitability.

PW Consulting’s report is designed to move readers from strategic curiosity to transaction execution. It combines detailed market-sizing (top-line market value and multi-year forecasts), qualitative and quantitative vendor assessments, and hands-on decision tools. Key deliverables include:

To maintain the “trailer” principle of this release, the report intentionally withholds granular segment-by-segment figures in this summary; those datasets and the underlying assumptions are available within the full report package.

The market remains moderately fragmented, with measured concentration at the top end of the supply chain — our competitive concentration metrics show a CR3 of 18.5% and a CR5 of 28.4%. That structure creates room for both global OEMs and specialized regional players to capture opportunity niches.

Valmet (Espoo, Finland) — Known for delivering complete biomass combined heat and power (CHP) plants, Valmet’s turnkey capability (boilers, turbines, flue-gas cleaning) positions it strongly in large-scale projects requiring integrated performance guarantees and emissions compliance.

ANDRITZ (Graz, Austria) — Its fluidized bed combustion solutions and history of large-bore biomass boilers make it a go-to for projects seeking high thermal efficiency and fuel flexibility across a range of feedstocks.

Babcock & Wilcox (Akron, Ohio) — With proven grate and hybrid stoker technologies, B&W continues to be a practical choice for plants emphasizing simplicity, robust co-firing capability, and established operations expertise.

Mitsubishi Power (Yokohama, Japan) — Recent efficiency milestones and advanced combustion integration underscore Mitsubishi’s role where marginal efficiency gains translate directly into competitive dispatch economics.

Siemens Energy and GE Vernova — Both supply turbines and generator systems optimized for biomass projects that require high flexibility and sophisticated control systems for variable fuel inputs and grid services.

Kraftwerke Mannheim — A European specialist emphasizing cogeneration and integration with district heating, valuable for projects seeking multi-vector revenue streams.

Zibo Zichai New Energy — A domestic Chinese manufacturer of gasifiers and small-to-medium power equipment, important for decentralized and industrial-hosted installations.

Recent commercial signals validate these dynamics: major commissioning and order activity across Europe and Asia in 2024 and early 2025 illustrate that demand is both global and heterogeneous. These vendor moves are consistent with a market that rewards scale, integration capability, and regional supply-chain optimization.

Design for optionality: Select technologies and contractual structures that preserve fuel flexibility and retrofit paths. Projects sited today should be able to incorporate higher-efficiency cycles or alternate feedstocks as policy and market conditions evolve.

Lock in upstream supply while hedging price risk: Secure long-term feedstock agreements with indexed pricing and contingency clauses, but also design fuel-conversion contingencies and multisource logistics to reduce single-point vulnerability.

Leverage policy stacking: Layer existing incentives (investment tax credits, Renewable Energy Directive mechanisms, local capacity payments) into a robust financing case rather than relying on a single subsidy stream.

Prioritize efficiency and ancillary markets: Higher thermal efficiency and the ability to provide grid-balancing services materially improve plant value, particularly in markets with elevated carbon prices.

Prepare for M&A and partnerships: The mid-market is ripe for consolidation and strategic partnerships between EPCs, fuel suppliers, and utilities. Early alliance-building de-risks execution timelines and can secure preferential feedstock access.

PW Consulting offers tailored advisory services that translate the report’s insights into executable plans:

For corporate strategists, sponsors, and utility planners preparing capital and resource allocations in 2026, the right mix of market intelligence, vendor insight, and practical tools will determine who captures the most value in this growing market. PW Consulting’s Biomass Power Equipment Market report provides that mix — combining top-line market measurements, near-term policy sensitivity, and transaction-ready playbooks.

Leaders preparing to act in 2026 should request the full report package to access the underlying datasets, regional and technology breakdowns, vendor scorecards, and downloadable financial models. The granular tables and scenario work are intentionally reserved for the full report to ensure executives can base decisions on comprehensive, auditable inputs.

Contact PW Consulting to arrange a briefing, obtain the full dataset, or commission a tailored advisory engagement that transforms these insights into funded projects and repeatable operational models.

For detailed analysis of this topic, please visit the official page:Biomass Power Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com