North America Inertial Sensing Systems Market Set for Strong Growth Amid Rising Autonomous Technology Adoption

Other |

2026-06-11 13:12:51

PW Consulting today releases a focused industry brief on the Data Center Battery Backup Unit (BBU) market designed to help corporate leaders, procurement heads, and infrastructure architects make high-confidence decisions in 2026. Built on a rigorous historical baseline (2020–2025) and forward-looking scenario modeling to 2032, the study distills the dynamics that will shape resilience, total cost of ownership, and supply-chain risk for mission-critical facilities.

Data Center Battery Backup Unit Market

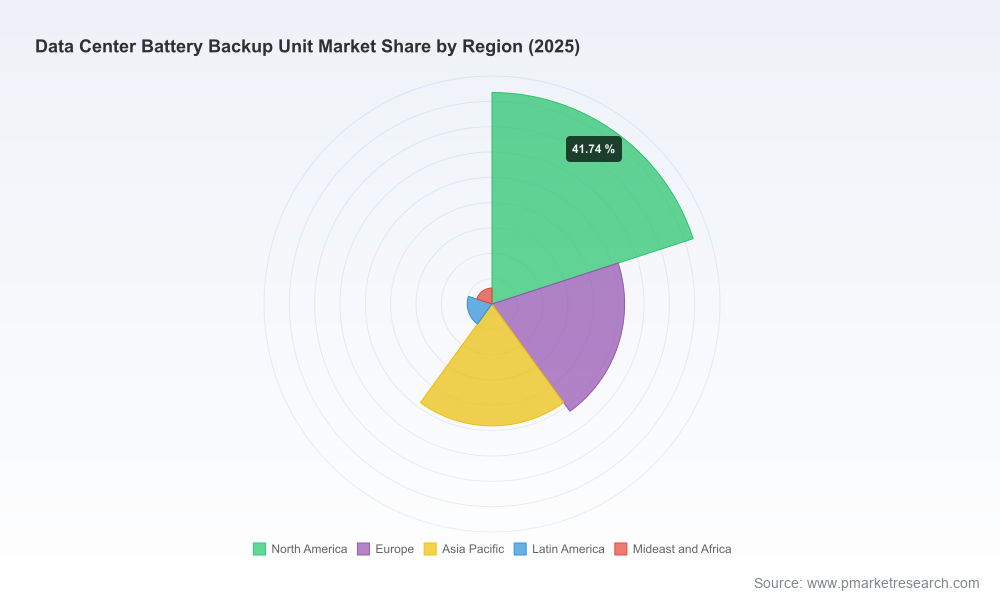

Market trajectory: The data center BBU market has expanded materially over the last five years and is positioned for sustained growth through the forecast window. Our base-year analysis (2025) and long-form projection indicate a multi-year compound annual growth rate (CAGR) in the neighborhood of 8.15% through 2032, reflecting the combined effects of hyperscale capacity additions, edge deployments, and the electrification and decarbonization choices of large enterprises.

Data Center Battery Backup Unit Market

Strategic inflection: Innovations in battery chemistry, modular UPS design, and system-level thermal management are shifting procurement calculus from pure capital cost to lifecycle performance and operational flexibility.

Data Center Battery Backup Unit Market

Concentration and competitive balance: Market share is meaningfully distributed — leading suppliers hold a substantial but not dominant portion of the market, leaving room for technology specialists and new entrants to influence product direction and pricing.

Timing matters. The choices you make in 2026 — about battery chemistry, supplier contracts, and modular vs integrated UPS architectures — will set asset performance and cost profiles for 7–12 years. With procurement lead times, tariff regimes, and raw-material volatility all increasing the margin for execution risk, advance planning becomes essential.

Cost engineering is no longer theoretical. Device-level price improvements coexist with system-level integration costs (installation, cooling, balance-of-plant). Our analysis quantifies these trade-offs and converts them into clear scenario outcomes for CapEx and OpEx across likely deployment paths.

Supply-chain risk is asymmetric. Concentration in upstream cathode and cell manufacturing creates tail risk for organizations that do not proactively hedge their exposure or diversify suppliers and chemistries.

Proven sizing methodology: Transparent, auditable market-sizing that reconciles shipment, installed-capacity, and revenue methods for 2020–2025 and stress-tests them under three adoption scenarios to 2032.

Strategic playbooks: Procurement templates and contract clauses designed to mitigate long lead times and tariff exposure, including recommended warranty structures, performance-based milestones, and inventory buffer strategies.

Technology decision matrices: Comparative lifetime-cost models for lead-acid, lithium-based options, and emerging chemistries — including sensitivity to replacement cycles, energy density, thermal management needs, and end-of-life recycling pathways.

Integration blueprints: Recommended architectures for modular UPS + BBU systems that simplify capacity scaling, improve serviceability, and reduce downtime risk during upgrades or retrofits.

Vendor evaluation tools: Relative positioning frameworks and risk-scorecards that let buyers shortlist suppliers based on performance, service footprint, financial resiliency, and strategic alignment with sustainability goals.

The vendor ecosystem combines legacy battery manufacturers, power-system integrators, and industrial conglomerates. Each cohort brings different strengths — from chemistry and cell manufacturing to UPS system design and global service networks. Key players profiled in the report include:

EnerSys (Reading, PA): A long-standing provider focused on advanced lead-acid solutions tailored for UPS applications and high-temperature operation. EnerSys continues to command leadership in traditional backup deployments and has publicly signaled expanding activity in lithium trials — a strategic move to defend against future displacement and capture hybrid architectures.

C&D Technologies (Columbus, GA): A specialist in VRLA and pure-lead AGM batteries, historically strong in enterprise and colocation segments. Their century-plus experience in lead systems remains a differentiator for buyers prioritizing thermal tolerance and known lifecycle behavior.

Saft (Levallois-Perret, France): Brings turnkey lithium-ion systems and large-scale storage experience, positioning to serve hyperscale projects that require higher energy density and grid-interactive capabilities.

Schneider Electric (Rueil-Malmaison, France): Integrates UPS platforms with modular lithium options and delivers design-for-serviceability advantages that appeal to operators pursuing faster refresh cycles and smaller physical footprints.

Eaton (Dublin, Ireland): Offers high-efficiency UPS systems with flexible battery integration options, competing on system efficiency and lifecycle cost optimization.

Vertiv (Westerville, OH): Combines UPS engineering with strong service operations and is extending its portfolio into liquid-cooled rack solutions tailored for AI workloads via strategic partnerships.

Mitsubishi Electric (Tokyo, Japan) and ABB (Zurich, Switzerland): Each brings global systems integration capability and product lines targeting large-scale, AI-ready installations where modularity and high-power density matter.

Recent market moves — from silicon-carbon anode announcements to vendor collaborations on liquid-cooled UPS modules — signal that competition will be won both at the chemistry level and in system engineering. Buyers should prioritize supplier roadmaps and demonstrated integration capability over headline performance claims.

Upstream concentration: A dominant share of key cathode production and a large share of import flows originate in a narrow set of geographies, creating exposure to geopolitical shifts and trade policy. Organizations should explicitly model component-constrained scenarios in their capacity plans.

Price and installed-cost trends: Benchmarks for 2026 show material variation by cell chemistry and installation complexity. Buyers must account for both cell-level price bands and total installed-system costs when evaluating lifecycle ROI.

Tariffs and trade measures: Elevated tariff regimes on imported battery cells and components in important markets are an active factor in 2026 procurement economics; sourcing strategies and local assembly options can materially alter project IRRs.

Balance-of-plant lead times: Long lead times for critical electrical infrastructure (for example, certain transformer classes) can stretch project schedules by multiple quarters — in some cases years — and should be treated as schedule-critical items during early-stage planning.

Adopt a hybrid procurement stance: Mix long-term framework agreements for core volumes with agile spot-buy capacity to capture price improvements and mitigate single-source risk.

Prioritize lifecycle TCO over upfront cost: Use our provided lifetime-cost templates to compare chemistries under realistic duty cycles, factoring in maintenance, replacement events, and potential grid-services revenue streams.

Validate thermal and modular integration early: Modular, serviceable designs materially reduce mid-life upgrade costs and downtime risk — require supplier proof points in RFPs.

Hedge supply exposure: Where possible, qualify multiple suppliers and consider localized assembly or strategic inventory to blunt tariff and lead-time disruptions.

Institutionalize scenario planning: Build reserve plans that consider component shortages, tariff escalation, and accelerated AI-capacity ramps. Treat these as part of the enterprise risk register rather than ad hoc concerns.

Our report arms 2026 decision-makers with the analytical framework and practical tools needed to navigate a market where technology, supply chains, and regulatory settings are rapidly evolving. The brief above highlights the forces at work and the high-level implications for procurement, engineering, and corporate risk teams. For actionable segmentation, vendor scorecards, detailed cost models, and downloadable scenario spreadsheets that support procurement and board-level decision-making, access the full report on the PW Consulting portal. The detailed datasets and model inputs are intentionally gated — they are the core instruments you will use to convert insight into executable strategy.

For detailed analysis of this topic, please visit the official page:Data Center Battery Backup Unit Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com