Automotive Fuel Vapor Canisters Market: Strategic Imperatives for 2026 Decision-Makers

Executive summary

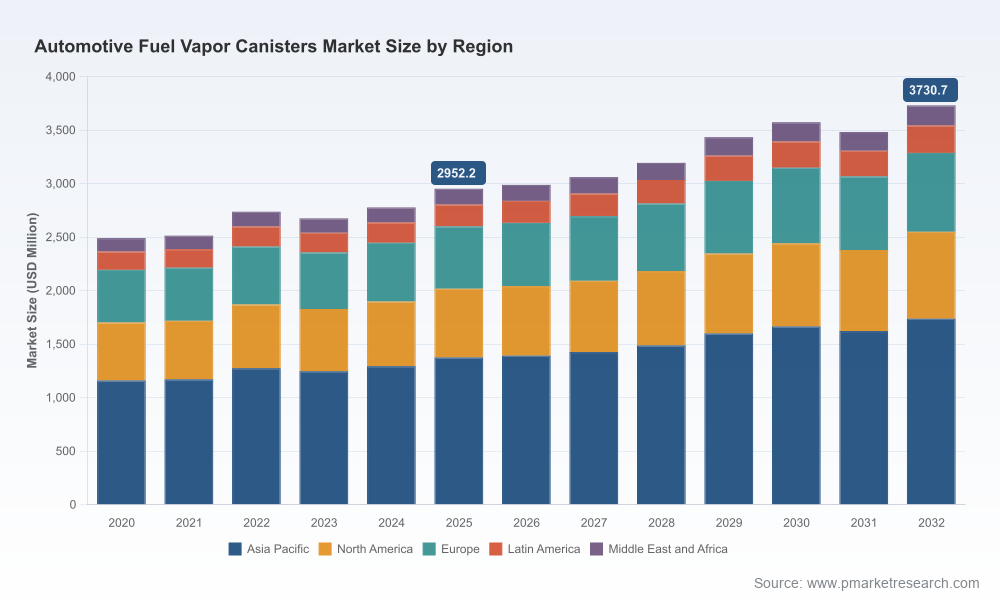

The global market for automotive fuel vapor canisters has entered a phase of steady, regulation-driven renewal. After recovering from near-term volatility, the market reached an estimated USD 2,952.2 Million in our base year (2025) and is projected to expand through the forecast window. PW Consulting’s modeling shows a compound annual growth rate (CAGR) of 3.42% across the 2026–2032 horizon, with the market moving toward roughly USD 3.73 billion by 2032 under the base scenario. For executives setting strategy in 2026, these headline metrics frame an environment where compliance investment, product optimization and supply-chain resilience will determine winners and losers.

Automotive Fuel Vapor Canisters Market

What this report delivers: practical intelligence, not platitudes

- Robust market sizing and forward-looking scenarios — including baseline, accelerated-regulation and fuel-blend disruption pathways — with transparent methodology and sensitivity testing.

- A supplier and competitive playbook: validated profiles, capability matrices, and an actionable scorecard for choosing OEM vs. Tier‑1 partners.

- Regulatory implications mapped to product specifications and validation protocols (e.g., running-loss, hot-soak and butane-loading tests), enabling engineering and compliance teams to prioritize development roadmaps.

- Cost-to-serve and procurement levers: raw-material exposure analysis, contract-structuring templates, and sourcing strategies for activated carbon and plastic/composite materials.

- Aftermarket and remanufacturing opportunity analysis, including coverage expansion tactics and parts-classification economics for late-model vehicles.

- M&A and partnership frameworks: target screening criteria, valuation heuristics and integration playbooks for accelerating technology adoption or capacity expansion.

- A 90-day tactical plan for revenue protection and margin improvement tailored to OEMs, Tier‑1s and independent aftermarket suppliers.

Market dynamics shaping 2026 decisions

Three structural forces dominate the fuel vapor canister landscape and should be the starting point for any boardroom discussion:

Automotive Fuel Vapor Canisters Market

- Regulatory tightening: Rulemaking—most notably advanced evaporative-emission standards—has raised the bar for canister performance and validation. Specific test protocols instituted by leading regulatory bodies require canisters to meet defined working-capacity thresholds and break-through limits under standardized butane-loading cycles. These compliance requirements have a downstream effect on canister sizing, media selection, and validation regimes, and they are fully factored into PW Consulting’s forecasts.

- Technology and product evolution: Design evolution is occurring along two axes. First, adsorbent media (activated carbon) is trending toward higher-capacity, multi-layer constructions validated for sustained performance across diurnal, hot-soak and running-loss stressors. Second, system-level integration — modular canister architectures that incorporate OBD integration, purge management and simplified serviceability — is reducing costs of compliance while opening aftermarket and retrofit opportunities.

- Supply and concentration dynamics: The market exhibits a relatively concentrated supplier landscape, where the top three and top five participants capture a large share of value, creating both stability and strategic sourcing risk. Feedstock variability for activated carbon and downstream media qualification timelines can become chokepoints when regulation accelerates or demand spikes. Our report models these supplier concentration effects and quantifies the potential margin and lead-time impacts under different sourcing scenarios.

Regulatory signals: why 2026 is a pivot year

For many manufacturers and suppliers, 2026 is less a continuation year than a pivot point. Standards finalized earlier in the decade prescribe detailed canister testing and performance criteria—defining working capacity by a standardized breakthrough threshold and mandating stabilization cycles and purge protocols. These technical requirements force earlier-stage choices in media specification and system architecture, and they materially affect validation timelines and capital planning. Companies that align product roadmaps and testing infrastructure now will avoid costly redesigns and market-entry delays as regulatory phases are implemented through the late 2020s.

Automotive Fuel Vapor Canisters Market

Competitive landscape — who moves first wins

Leadership in this market requires synchronizing product, compliance and channel strategies. The competitive field comprises legacy activated-carbon specialists, automotive systems integrators and aftermarket consolidators. Players that combine deep media expertise with systems integration and broad aftermarket channels consistently out-execute peers when standards change or coverage gaps appear.

- PHINIA Inc.: With a multi-decade footprint and modular canister architectures, PHINIA’s strength lies in system configurability and global OEM relationships. Their designs’ compatibility with a range of fuel blends gives them an advantage where ethanol/methanol compatibility is required.

- A. Kayser Automotive Systems GmbH: A market leader in activated-carbon canister systems, their vertically integrated systems approach (including tank isolation valves and purge lines) makes them a first-choice partner for OEMs facing tight emission budgets.

- MAHLE GmbH: Known for integrating canisters into broader fuel management systems, MAHLE’s global engineering scale supports rapid change management when validation protocols evolve.

- Standard Motor Products, Inc. (SMP): SMP’s aggressive aftermarket program expansion—including substantial late-model coverage additions in recent years—illustrates the revenue and resiliency benefits of broad parts catalogs for independent repair channels.

- MotoRad and similar independent manufacturers: These suppliers focus on nimble aftermarket and replacement markets, often winning share by rapid coverage of fleet and light-commercial vehicle applications.

- Ingevity Corporation: A leading producer of hardwood-based activated carbon media, Ingevity’s position on the raw-material axis makes them a strategic supplier for firms prioritizing high-capacity media; supply dynamics at this layer are a critical input to pricing and qualification timing.

Recent commercial moves illustrate how competition is unfolding in practice: aftermarket program expansions and broadened late-model coverage by major aftermarket suppliers have increased replacement-parts availability and shortened service lead times, while regulators’ adoption of tighter test protocols has forced design and testing investments across the board.

Strategic imperatives for 2026 — five priorities

Executives should prioritize actions that protect near-term revenue while positioning for regulatory-driven product demand. PW Consulting recommends five concurrent strategic tracks:

- Secure media supply and qualify alternatives: Lock multi-year feedstock agreements with primary activated-carbon suppliers and qualify at least two alternative media sources to avoid single-point failures during demand surges.

- Fast‑track validation and test capabilities: Invest in lab capacity to replicate regulator-defined cycles (including butane-loading and breakthrough testing) to reduce time-to-market for upgraded canister designs.

- Modular product architectures: Design canisters for modularity and serviceability to lower SKUs, simplify validation across fuel-blend variants, and enable aftermarket refurbish/reman programs.

- Aftermarket coverage as a growth lever: Expand late-model coverage and integrated purge-valve offerings to capture aftermarket replacement demand; aftermarket expansion proved defensive during recent vehicle fleet shifts.

- M&A and partnership scouting: Use targeted acquisitions to acquire specialized adsorbent technology, testing capabilities or regional distribution networks. Prioritize bolt-on deals where integration can be completed within 12–18 months to capture near-term regulatory-driven demand.

Decisioning toolkit included in the report

To operationalize the five priorities above, the PW Consulting report includes ready-to-use tools: supplier scorecards and negotiation playbooks, a capex phasing model keyed to regulatory scenario triggers, a parts-coverage heat map for aftermarket prioritization, and KPI dashboards for regulatory-cost-of-compliance. These deliverables transform strategic intent into executable workstreams for product, procurement and commercial teams.

Why now: the economics of acting early

The market’s moderate compound growth masks asymmetry: early movers that align product portfolios with next-generation test protocols, secure decoupled feedstock sources and expand aftermarket reach will capture disproportionate margin and share as competitors scramble to comply. Conversely, late action can force costlier redesigns, lengthen validation cycles and concede aftermarket share to nimble challengers.

Next steps and how PW Consulting can accelerate your program

PW Consulting’s Automotive Fuel Vapor Canisters Market report is designed as both a strategic compass and an implementation accelerator. The full study contains the granular segmentation, regional demand drivers, supplier-by-supplier scorecards, price and cost curves, and scenario-specific investment models that underpin the executive-level guidance summarized here. To convert these insights into a 90-day execution plan tailored to your organization—covering supplier contracts, testing-rig investments, SKU rationalization and aftermarket rollouts—contact our industry team or download the full report page.

Note: This briefing highlights high-impact trends and recommended responses while withholding detailed segment-level figures and supplier share matrices to preserve the value of the full report. The complete dataset and operational templates are available in the PW Consulting report and are essential for transactional decisions and capital allocation in 2026.

For detailed analysis of this topic, please visit the official page:Automotive Fuel Vapor Canisters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com