Professional Termite Control Services for Long Lasting Home Protection

Other |

2026-02-06 14:19:11

PW Consulting’s latest Smd Common Mode Chokes Market study equips leaders with the forward-looking intelligence required to make high-consequence choices in 2026. Anchored on a base year of 2025 and tracing historical dynamics across 2020–2025, the report projects the market through 2032. The market expanded from USD 620.4 Million in 2020 to USD 850.0 Million in 2025 and is forecast to reach USD 1,320.89 Million by 2032, reflecting a compound annual growth rate (CAGR) of 6.5% over the forecast horizon. This briefing highlights the strategic value of the full study for product planning, sourcing, M&A and commercial strategy — while reserving granular segment-level tables and vendor scorecards for subscribers who access the complete report.

Smd Common Mode Chokes Market

Actionable foresight for resource allocation: With steady mid-single-digit CAGR and accelerating pockets of demand in power-sensitive applications, 2026 is a year for decisive capacity and technology investments rather than incremental optimizations.

Smd Common Mode Chokes Market

Supplier strategy under stress: Our supply-chain modelling shows that lead-time sensitivity for specialized core materials and price volatility in copper/ferrite inputs create a window where procurement choices materially affect gross margins and time-to-market.

Smd Common Mode Chokes Market

Product roadmap calibration: Advances in high‑current SMD chokes, alternative core materials and integrated protection features are shifting the competitive frontier. 2026 roadmaps must balance high-current power variants with compact, high-frequency solutions.

Regulatory and compliance alignment: Standards and automotive-grade certifications are decisive for customer qualification in target segments; a missed certification pathway in 2026 can delay commercial wins into 2027–2028.

Market sizing and validated forecasts: Base-year calibration (2025) and scenario forecasts to 2032, with sensitivity runs that isolate demand shocks, material cost inflation and substitution effects.

Segment strategy playbooks: Action-oriented guidance on product prioritization, pricing guardrails and go-to-market sequencing for segments where performance and reliability command premiums.

Supplier & partner intelligence: Comparative profiles, capability matrices and a procurement readiness checklist to accelerate supplier qualification and reduce onboarding cycle times.

Technology roadmap and standards matrix: Assessment of core technologies (ferrite, nanocrystalline, thin-film approaches), manufacturability constraints and compliance pathways including IEC/EN frameworks.

Supply-chain stress tests: Lead-time modelling and inventory optimization levers for nanocrystalline cores, copper wire, and other critical inputs — with pre-built scenarios for constrained vs. normalized markets.

M&A & partnership playbook: Target scouting criteria, integration risk checklists and valuation sensitivities for bolt-on acquisitions in manufacturing, materials or assembly capabilities.

Commercial tools: Price sensitivity maps, tender strategies for high-volume customers and an OEM segmentation framework to align sales motions with technical value propositions.

Growth is durable but selective: The overall market trajectory supports investments in capacity and R&D, yet returns will be concentrated in product lines that address high-current demands, thermal reliability and EMC compliance.

Product differentiation wins: Suppliers that combine high-current capability with compact footprint, robust thermal behavior and simplified assembly (reflow-ready packages) will capture value premiums.

Procurement levers matter more than ever: Given lead‑time variability for advanced core materials, firms that implement multi‑tier sourcing, longer-term agreements and strategic buffer inventories will preserve delivery reliability and margin.

Standards accelerate market access: Early investment in compliance and automotive-grade qualification (e.g., AEC-level protocols where relevant) reduces time-to-revenue with OEMs and Tier‑1 customers.

Consolidation is meaningful but not lock-in: Market concentration metrics indicate a market where leading vendors have influence, yet substantial opportunity remains for differentiated challengers, especially those that excel in niche performance characteristics or cost-to-serve.

The SMD common mode choke arena blends multinational incumbents and specialized component houses. Our competitive analysis synthesizes product portfolios, manufacturing footprints and recent go-to-market initiatives to surface partners, suppliers and likely acquisition targets.

TDK Corporation (Tokyo) — Strength: high-current SMD solutions with reflow-compatible packages. Recent product launches underline a focus on telecom and industrial power electronics applications that demand 24–36A capability at elevated ambient temperatures.

Murata Manufacturing (Kyoto) — Strength: broad EMC portfolio across varied sizes and current ratings; depth in miniaturized SMD coils useful for dense consumer and comms boards.

YAGEO Group / Pulse Electronics (Taipei) — Strength: targeted high-current designs for DC/DC converters and power lines, with form-factor innovations suited to modern power architectures.

Bourns, Inc. (Riverside) — Strength: automotive-qualified (AEC) SMD chokes and proven flavor for industrial robustness.

Vishay, Schaffner, Eaton, Littelfuse — Strengths vary from high-current series to integrated protection features and systems-level EMC expertise; each brings channels into industrial, automotive and power-management ecosystems.

Sumida, Coilcraft — Strengths: focused capabilities for consumer and high-frequency suppression applications, with rapid development cycles for emerging product needs.

Recent product launches in 2025 demonstrate that vendors are racing to own high-current, reflow-compatible and application-specific variants. These moves create short windows of competitive advantage; buyers and OEMs should evaluate vendor roadmaps when making 2026 sourcing commitments.

Core materials dominate risk profiles: Ferrite cores remain a primary input; nanocrystalline cores, when required for advanced filters, exhibit standard lead times in the 8–12 week band and can extend to 16–22 weeks in constrained periods. Procurement scenarios in the full report quantify the P&L impact of these delays.

Commodity volatility: Copper wire and ferrite pricing are subject to market swings and geopolitical pressures; small per-unit cost shifts compound into meaningful margin erosion at scale unless hedged.

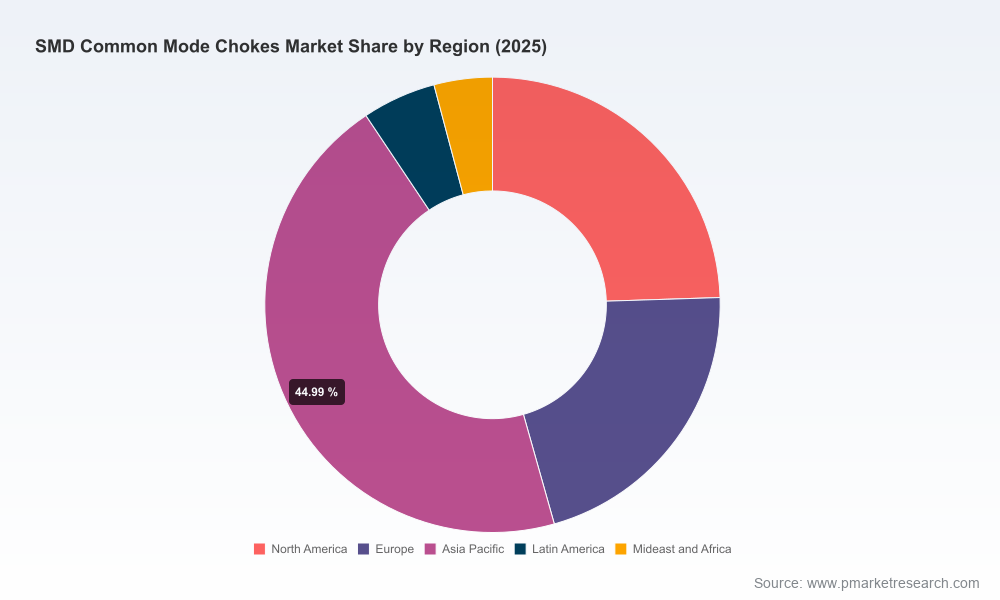

Manufacturing geography: Asia‑Pacific remains a core manufacturing hub for SMD choke production. This geography advantage facilitates scale but also calls for geopolitical risk mitigation strategies for Western OEMs.

Mitigation playbook: The report prescribes tactical options — dual-region sourcing, vendor diversification, engineered substitution and contractual lead-time SLAs — to shield 2026 operations from upstream shocks.

Common mode chokes intended for power applications are bounded by IEC/EN frameworks; early adoption of standards-based test protocols reduces qualification cycles for customers that are standards-driven.

Automotive and industrial specifications require distinct qualification paths. The full report maps typical elapsed times and test sequences to help R&D and claims teams de-risk product launches slated for 2026.

Integrate the forecast scenarios into CAPEX reviews: use the report’s demand trajectories and sensitivity tables to size investments in winding capacity and thermal test facilities.

Adopt a supplier-risk scorecard: the report includes a ready-to-use template to rate suppliers across capability, lead time resilience, certification readiness and cost trajectory.

Prioritize certification roadmaps: sequence AEC/industrial/IEC qualifications to align with customer procurement cycles and avoid missed revenue windows in 2026.

Define M&A screening criteria: use the included acquisition playbook to identify targets that add manufacturing scale, specialized core material access or complementary product lines.

Model margin scenarios with commodity shocks: apply the report’s cost-service templates to quantify breakeven pricing under 10–25% swings in key input costs.

PW Consulting’s Smd Common Mode Chokes Market report is designed to be a tactical companion for executives, product leaders and procurement teams making binding decisions in 2026. It demonstrates the depth of our market measurement and scenario analysis while reserving granular breakdowns by region, application and product type for the full document — a deliberate choice to provide a concise, actionable public briefing while directing decision-makers to the comprehensive intelligence needed to execute with confidence.

For access to the complete market maps, vendor scorecards, segment tables and downloadable models that underpin these conclusions, please visit our report page or contact PW Consulting’s industry team to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Smd Common Mode Chokes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com