Semiconductor O-Rings and Seals Market: Size, Emerging Trends, Top Players, Regional Analysis & Forecast 2026–2034

Other |

2026-06-29 12:29:02

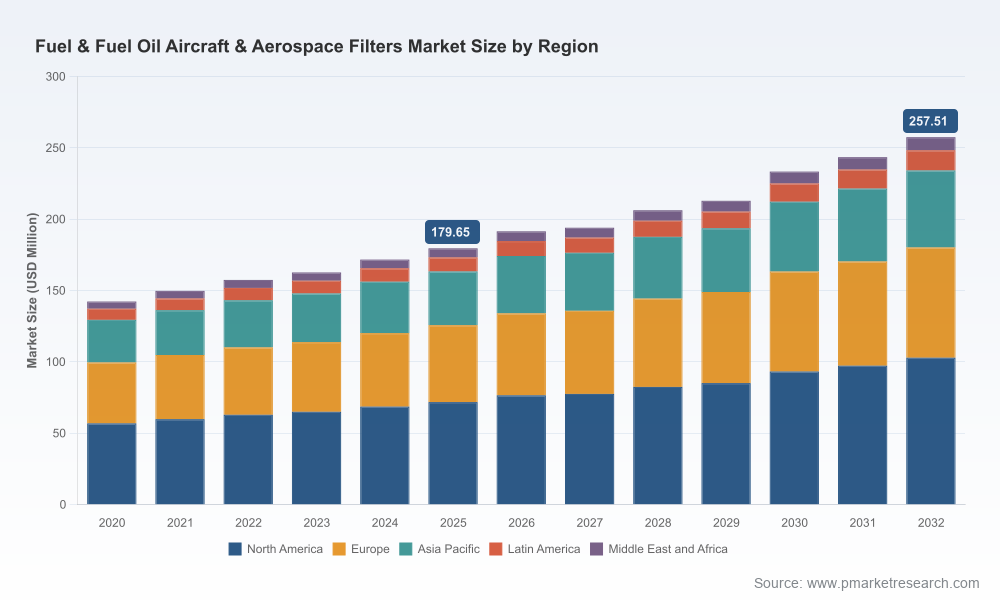

PW Consulting’s new market research briefing on the Fuel, Fuel Oil & Aircraft Aerospace Filters market synthesizes proprietary modeling, primary interviews, and regulatory mapping to give executives an operational blueprint for 2026. Using a 2025 base year and a 2026–2032 forecast horizon, our view shows a market expanding at a compound annual growth rate (CAGR) of 5.25%. In absolute terms the global market is estimated at USD 179.65 Million in 2025, rising to USD 191.55 Million in 2026 and targeting USD 257.51 Million by 2032 under the base forecast scenario. These topline numbers validate an investment-grade growth corridor — large enough to justify targeted R&D, M&A and supply-chain reconfiguration, yet concentrated enough to preserve margin upside for differentiated suppliers.

Fuel Fuel Oil Aircraft Aerospace Filters Market

Regulatory inflection: The accelerating introduction and progressive tightening of rules such as ReFuelEU Aviation (minimum SAF blending mandates) create near-term technical and operational demands on filter performance and certification. Our analysis models how evolving fuel specifications cascade into filter lifecycle, maintenance intervals and retrofit cycles.

Fuel Fuel Oil Aircraft Aerospace Filters Market

Standards and safety: Industry standards (for example EI specifications) continue to codify two-stage filtration and water-separation requirements. Purchasers and specification engineers must reconcile legacy systems with contemporary two-stage architectures to avoid service disruptions and costly uncoupling at shop visits.

Fuel Fuel Oil Aircraft Aerospace Filters Market

Fuel quality risk profile: Non-fuel contaminants remain a systemic hazard — from DEF contamination-crystallization events to emulsified water and particulate ingress. The report quantifies contamination vectors and maps expected failure modes into maintenance cost impact and AOG risk matrices.

Technology and product transition: Recent supplier moves — from product phase-outs to acquisitions aimed at expanding mission-critical capabilities — signal a period of product rationalization and capability consolidation. The result is a compressed window for buyers to revalidate vendor roadmaps.

Executive dashboard: Clear topline sizing (2020–2032 historic and forecast series), growth drivers, and a short-list of the three most impactful scenarios for 2026 procurement planning.

Scenario modelling: Three alternative pathways (Conservative, Accelerated SAF Adoption, and Technology-Driven Efficiency) that translate policy and cost shocks into expected inspection cycles, filter unit demand and aftermarket revenue implications.

Buy-side playbook: RFP templates, evaluation scorecards, and a Supplier Performance Index designed to accelerate sourcing decisions while protecting continuity of supply and certification risk.

Vendor benchmarking: Qualitative and quantitative profiles for the market’s core vendors, including capability maps, route-to-certification timelines and technology differentiators. (Note: detailed split tables by region, type and application are excluded from this press summary to preserve the report’s proprietary value — they are included in the full report.)

Implementation guidance: Step-by-step technical checklists for SAF compatibility testing, water barrier retrofits, and lifecycle-cost calculators that convert filter performance metrics into fleet-level OPEX/availability outcomes.

M&A and partnership playbook: Identification of capability adjacencies where bolt-on acquisitions or JV structures yield rapid entry into higher-margin, certified product segments.

The market exhibits a mid-level concentration: the three largest firms account for a meaningful share of installed performance (CR3 ~48.5%), and the top five consolidate a majority of the commercial presence (CR5 ~62.8%). This structure favors focused differentiation strategies — leading incumbents combine deep OEM relationships and certification expertise while specialist vendors compete on agility and niche approvals.

Parker Hannifin Corporation (Cleveland, OH) — A long-standing supplier of aviation fuel filtration systems and branded Velcon product lines. Parker’s product rationalization (including a phase-out notice on an EI-qualified SAP monitor late in 2025) signals a platform transition: expect investments in next-generation water barrier and contamination-detection technologies as the company repositions its fleet support proposition.

Donaldson Company, Inc. (Minneapolis, MN) — A durable player in filter cartridges and system integration, with strategic inorganic expansion verified by its completion of the Facet Filtration acquisition in May 2026. That move broadens Donaldson’s mission-critical capabilities and accelerates its route to avionics-adjacent filtration solutions.

Pall Corporation (Port Washington, NY) — Known for high-performance filters compatible with SAF blends and for persistent OEM relationships. Pall continues to underpin large fleet programs and has maintained operational ties to major carriers for fleet-level filter supply and lifecycle services.

Porvair Filtration Group (Fareham, UK) — Niche specialist in bespoke and last-chance filtration and tank inerting filters. Porvair’s advantage is customization and rapid engineering cycles for retrofit programs.

Safran (Paris, France) — Integrates filtration within broader aerospace equipment portfolios; an attractive partner for airframe and engine OEMs pursuing systems-level performance improvements.

Eaton Corporation (Dublin, Ireland) — Supplies modular components and assemblies for aerospace fuel systems; competitive where supply-chain resiliency and standards compliance are purchase criteria.

Tempest Aero Group, Chase Filters & Components, Global Filtration, Norman Filter Company — Smaller, agile firms that defend market share through PMA certifications, high/low pressure niches, and specialized military/space-grade filtration products.

May 2026 — Donaldson finalizes acquisition of Facet Filtration to expand aviation filtration offerings.

December 2025 — Parker Hannifin issued final notice on cessation of production for a legacy EI-qualified SAP monitoring product, accelerating buyer attention to replacement technologies and migration pathways.

February 2026 — Pall Corporation continued fleet support programs with major carriers, underscoring enduring OEM and airline tie-ins for aftermarket supply.

SAF cost and availability: Sustainable Aviation Fuel remains materially more expensive than conventional jet kerosene (by multiples in industry practice), creating asymmetric incentives for operators and fuel suppliers. Filters must be validated against a widening spectrum of fuel chemistries — our testing matrices quantify expected degradation modes and retrofit schedules for common SAF blends.

Contamination incidents: DEF contamination continues to be a low-frequency, high-impact risk. The crystallization and clogging pathways that follow contaminate filter systems; decision-makers must prioritize contamination-detection and containment measures in fuelling operations.

Standards alignment: Adherence to EI filtration standards and to evolving cert requirements will drive upfront testing and documentation costs. Early alignment reduces downstream AOG exposure and approval lag for new filter technologies.

Supply-chain concentration: While top-tier suppliers wield certification advantages, there exists a material opportunity for specialist vendors to capture aftermarket share through PMA pathways and retrofit service models.

Airlines and lessors — Initiate a two-track procurement strategy: (1) immediate audit of installed filter inventories and failure-mode histories to mitigate near-term AOG risk; (2) pilot SAF compatibility validation with two vendors under flight-like conditions to de-risk full-fleet rollouts.

OEMs and engine manufacturers — Revisit filter specifications and collaborate with filter suppliers on co-developed, certified solutions optimized for new fuel chemistries and two-stage separation architectures.

Filter manufacturers — Accelerate investment in water barrier, coalescer and contamination-detection technologies; consider inorganic growth to gain cartridge-level IP and to expand aftermarket reach into MRO networks.

Fuel suppliers & airports — Implement contamination monitoring upgrades at fueling points and integrate filter performance feedback into fuel quality management systems.

Investors — Prioritize targets with certification footprints and retrofitting service models; look for acquisition targets that can deliver rapid route-to-market for SAF-compatible filtration technologies.

Use the full report to convert strategic intent into procurement and engineering action plans. The document includes downloadable decision-support spreadsheets, RFP templates, certification timelines, and a prioritized vendor list. It is specifically designed to be pluggable into 90–180 day transformation sprints so that 2026 budgets and roadmaps translate to measurable reductions in AOG exposure and lifecycle cost.

For readers of this summary: we have intentionally withheld detailed segmentation tables, regional/application split values and certain proprietary supplier scorecards to preserve the report’s actionable value. The full dataset, including complete regional and application breakdowns, unit economics, and scenario-specific demand curves, is available through PW Consulting’s publication page.

To access the full report and the supporting toolkits that operationalize these insights for 2026 decision-making, please visit the PW Consulting research portal or contact our industry team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Fuel Fuel Oil Aircraft Aerospace Filters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com