What Is Driving Growth in the Microinsurance Market for Financial Inclusion?

Networking |

2026-04-23 18:34:32

PW Consulting’s latest Robot Joint Actuator Market research synthesizes five years of historical performance, fresh primary research from industry shows (including CES 2026), and a rigorous seven‑year forecast to give strategic leaders a decision‑grade view entering 2026. The sector is no longer a niche mechanical subassembly — joint actuation has become a systems battleground determining robot performance, cost structure, and time‑to‑market for the next generation of industrial, collaborative, humanoid, and service robots.

Robot Joint Actuator Market

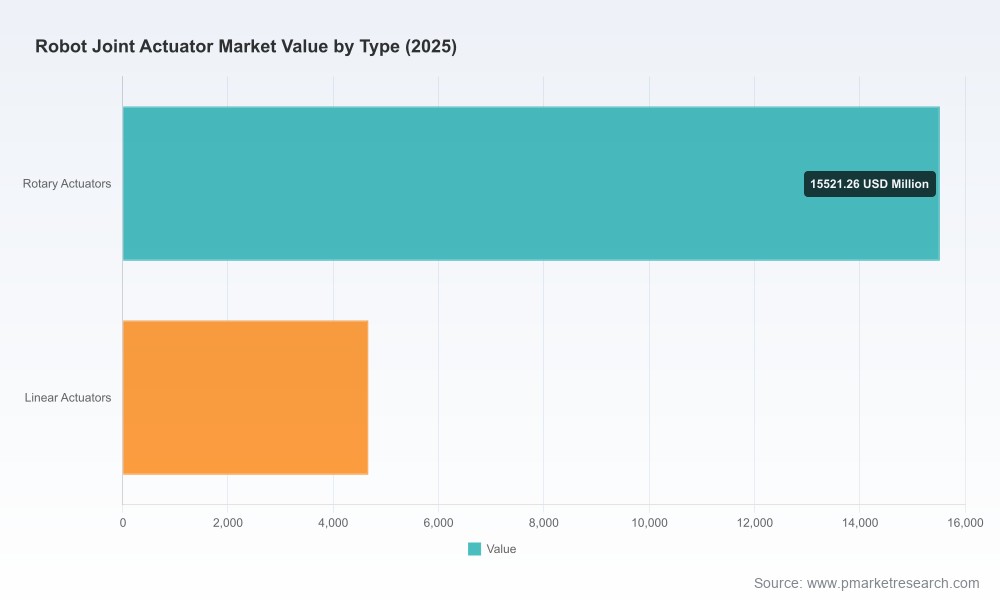

At the macro level, the market scaled rapidly over 2020–2025 (from approximately USD 8.9 billion in 2020 to about USD 20.2 billion in 2025) and is forecast to continue accelerating in the forecast window. PW Consulting projects a sustained compound annual growth rate (CAGR) of 18.52% through 2032, with the global market trajectory reflecting both widening application sets and rising unit complexity. Importantly, market concentration measurements demonstrate meaningful clustering: the top three suppliers control roughly the low‑forties percent of industry revenue, while the top five approach the mid‑fifties percent — underscoring a competitive environment of strong incumbents alongside a fast‑growing set of challengers.

Robot Joint Actuator Market

Timing: 2026 is a hinge year. Investments made now in supplier selection, actuator architecture, and integration capabilities will determine whether firms capture early humanoid deployments and the next wave of collaborative automation.

Robot Joint Actuator Market

Cost and complexity: Advances in actuator integration (motors, gearing, encoders, electronics and thermal management) mean that joint modules are increasingly the locus of value capture and differentiation. For certain robot classes, actuator cost can represent a dominant share of production cost — a structural change that forces OEMs to treat actuators as strategic platforms rather than commodity parts.

Standards and risk: Recent international updates to industrial robot standards and the harmonization into U.S. guidance tighten requirements around collaborative use, end‑effector interfaces, and cybersecurity — affecting certification paths, design cycles, and supplier due diligence.

The market has transitioned from steady equipment replacement and industrial automation growth into a rapid expansion driven by new form factors and applications. Between 2020 and 2025 the global robot joint actuator market more than doubled; PW Consulting’s forecast indicates further acceleration through 2032, propelled by the commercial scaling of humanoid platforms, increasing adoption of cobots in new verticals, and ongoing upgrades in industrial fleets seeking higher dexterity and safety.

Key structural takeaways:

Accelerating unit complexity: A rise in integrated joint modules — incorporating precision gearing, embedded electronics, dual encoders, and active thermal management — is shifting supplier economics and purchasing behavior.

Consolidation pressure amid fragmentation: While a handful of established vendors account for a significant share of revenue, numerous specialized suppliers and scale‑up entrants are eroding legacy channel dynamics, especially in humanoid and service robotics niches.

Standards and supply‑chain resilience are now strategic axes: compliance with updated ISO/ANSI guidance and control of critical material inputs will materially affect time to revenue and warranty exposure for OEMs.

The report is built as a hands‑on strategic toolkit for executives, with deliverables designed to be directly usable in 2026 planning cycles:

Market framework and TAM modeling — transparent methodology, demand drivers, and scenario variants for conservative, base, and aggressive adoption curves.

Supplier scorecards and risk matrices — technology and commercial assessments for leading and emerging vendors, including integration maturity, manufacturing footprint, IP posture, and supply‑chain risk indicators.

Technology roadmaps — component‑level evolution (gearbox topologies, encoder architectures, motor materials and thermal strategies) and implications for product lifecycles and serviceability.

Procurement playbooks — request for proposal (RFP) templates, total cost of ownership (TCO) calculators, and criteria for qualifying integrated actuator suppliers versus modular sourcing.

Go‑to‑market scenarios and partnership blueprints — options for captive development, strategic sourcing, joint ventures, and licensing to accelerate deployment while controlling cost and IP.

Board‑level briefings and investment memos — concise executive summaries keyed to M&A, capex, and strategic sourcing choices.

The landscape comprises established precision‑gear and motion specialists, vertically integrated robotics groups, and fast‑moving regional innovators. PW Consulting’s benchmarking identifies several archetypes and strategic postures among the most consequential players:

Precision gear incumbents (e.g., Harmonic Drive family of companies) — strong IP in zero‑backlash strain wave gearing and long histories supplying high‑precision positioning systems. Their advantage lies in proven durability and deep application engineering support, but they face margin pressure as system integrators push for bundled actuator modules.

Integrated actuator specialists (e.g., Maxon Group, Kollmorgen, Moog) — these firms are packaging motors, gearboxes, encoders, and control electronics into sealed, serviceable joint modules. They win where customers prioritize turnkey performance, environmental protection, and predictable certification paths.

New challengers and regional champions (e.g., CubeMars, ZeroErr, RealMan Robotics, Arcsec Drive) — these vendors are targeting humanoid, service and legged robot niches with ultra‑high torque‑density designs and compact modularity. Their strengths are rapid iteration cycles and competitive unit economics; weaknesses include limited field data and variable quality control at scale.

Platform integrators and OEMs (e.g., ABB, ROBOTIS, Boston Dynamics partnerships) — some robot OEMs are moving toward captive sourcing or exclusive supplier agreements to lock down performance differentiation. Recent strategic supplier relationships announced at CES underscore the speed at which platform OEMs are securing actuator supply for new product rollouts.

Recent industry moves reinforce these patterns: demonstrations of compact integrated modules at CES 2026, the launch of new branded actuator offerings by large electronics firms, and strategic supply agreements for humanoid platforms all signal that incumbents and newcomers are contesting system integration as the primary value lever.

Standards update: Revisions to major robot standards (ISO 10218 updates and the ANSI adoption) broaden requirements for collaborative operations and add cybersecurity and classification guidance — affecting design validation, documentation, and supplier contracts.

Materials and durability: Component metallurgy (high‑carbon steel alloys in flexsplines, for example) remains a determinant of fatigue life and warranty exposure; specifications focusing on extended duty cycles and rated hours are now common in supplier negotiations.

Cost structure shifts: As humanoid programs mature, actuator modules can represent a dominant share of unit BOM cost, pushing product teams to justify premium actuator choices through lifecycle value (uptime, maintenance, and enablement of higher‑value functions).

PW Consulting advises executives to treat the actuator decision as strategic, not tactical. Our recommendations are intended to be directly executable in 2026 planning cycles:

Segment your procurement strategy by risk and differentiation: Use three procurement lanes — strategic (exclusive or co‑developed modules for differentiated platforms), managed (preferred suppliers with multi‑year supply agreements), and commodity (standardized components). This approach balances speed, cost and IP protection without over‑allocating capex.

Invest in joint integration capability: Capabilities in thermal management, embedded control, and firmware harmonization pay off quickly. OEMs that invest in integration testbeds and standardized interfaces reduce time‑to‑certification and cut warranty costs.

Pursue modular product architectures: Design robots so joint modules can be upgraded in the field. This extends product life, enables performance tiering, and opens aftermarket revenue channels.

Prioritize standards and cybersecurity compliance early: Regulatory revisions are enforcing new documentation and cybersecurity obligations. Early compliance reduces certification risk and is increasingly a procurement precondition for large enterprise buyers.

Consider strategic partnerships or minority investments: For firms lacking integrated actuator expertise, minority equity stakes or exclusive supply agreements with high‑potential actuator specialists are effective ways to secure roadmaps and preferential access without full vertical integration.

Build supply‑chain resilience into TCO: Account for materials, fatigue life guarantees, and single‑source dependencies in your TCO models; include scenario stress tests for raw‑material lead times and regional production constraints.

Use the PW Consulting report as an operational playbook rather than a descriptive summary. Key use cases we recommend for executive teams:

Align procurement and product roadmaps: apply supplier scorecards to upcoming RFPs and select pilots to validate integration assumptions within your 2026 product cadence.

Inform board and investor conversations: our scenario‑based forecasts and TCO models provide defensible narratives for capital allocation to robotics initiatives.

Guide M&A and partnership diligence: use the vendor benchmarking and risk matrices to prioritize targets and structure earn‑outs tied to integration performance.

The robot joint actuator market is entering a decisive phase where technological integration, standards compliance, and supplier strategy will define winners and losers. PW Consulting’s report equips leaders with the frameworks, vendor assessments, and executable playbooks needed to act in 2026 with confidence. For granular segment economics, vendor‑level metrics, and downloadable procurement tools referenced throughout this summary, consult the full report and data annex on PW Consulting’s website.

For detailed analysis of this topic, please visit the official page:Robot Joint Actuator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com