Elderly Care Market Overview: Key Drivers and Challenges

Other |

2026-05-06 09:32:51

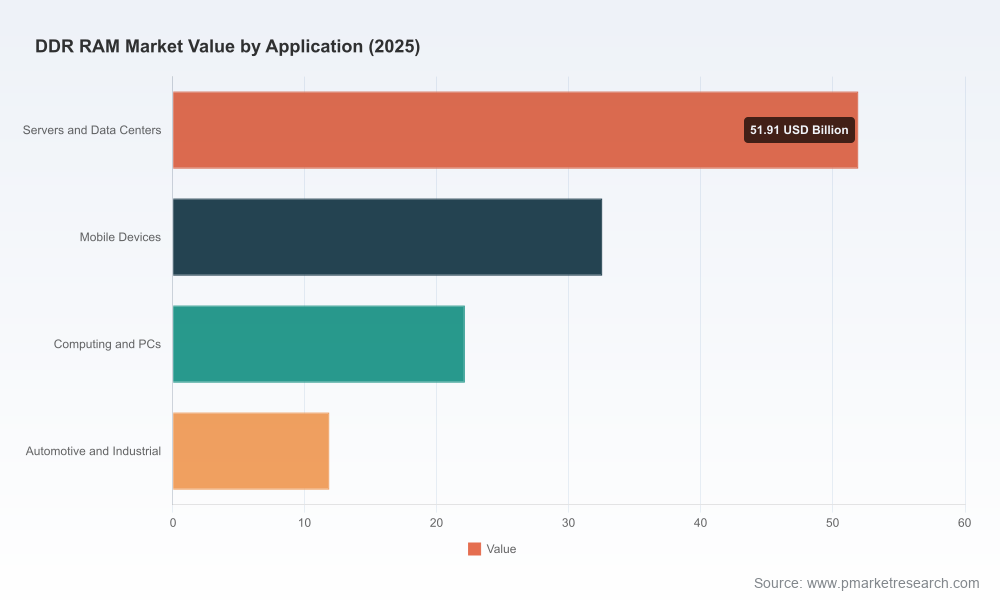

PW Consulting’s new Ddr Ram Market Research report—anchored on a 2025 base year and projecting through 2032—delivers the practical, scenario-tested intelligence that corporate leaders, procurement chiefs, and product strategists need to set confident plans for 2026. The global DDR RAM market has moved from cyclical fragility to structurally higher demand intensity: our analysis finds the market growing at a compound annual growth rate (CAGR) of 12.18% across the 2026–2032 forecast window, with an underlying market value that rose to approximately USD 118.4 billion in 2025 and is projected to pass the USD 260 billion mark by the end of the forecast horizon. This report is designed as a decision-grade briefing—demonstrating rigorous methods, transparent assumptions, and executable recommendations—while reserving granular segment tables and vendor scorecards for the full study.

Ddr Ram Market Research

Procurement and inventory strategies are now strategic levers. With wafer allocation shifting toward high-margin HBM and AI accelerators, standard DDR production is rationed in many supply chains. Our report synthesizes supply-side constraints, price inflection triggers, and timing windows to help buyers avoid both excess inventory and supply shortfalls.

Ddr Ram Market Research

Product roadmap prioritization requires tight alignment with memory roadmaps and JEDEC standard transitions. The report maps how evolving standards and module capabilities change performance-cost trade-offs across client, server, and mobile platforms—essential for engineering and product management teams setting 2026 release plans.

Ddr Ram Market Research

Capital and M&A decisions must factor structural concentration and geopolitical risk. The market’s high concentration among a small number of producers and recent policy dynamics materially alters the risk/return calculus for expansion, partnership, or localized supply strategies.

The memory market’s trajectory over the past half-decade shows pronounced volatility followed by structurally higher demand. From a 2025 base near USD 118.4 billion, our forecast anticipates continued expansion driven by data-center acceleration, AI workload proliferation, and next-generation client and mobile architectures. By 2026 the market is expected to reflect continued upward pressure—supported by enterprise spend and AI-driven module allocation—and to then compound at the forecast CAGR to reach a materially larger market by 2032.

Importantly, growth is not uniform. The drivers of near-term premiums in 2025–2026 differ from the medium-term secular trends that underpin our 12.18% CAGR: short-term capacity reallocation and spot-market squeezes are overlaying a multi-year shift toward higher-density DDR5 adoption and new module types. PW Consulting’s approach separates cyclical pricing shocks from structural adoption curves so executives can make differentiation decisions that reflect both immediate tactical needs and long-term value creation.

Supply reallocation toward HBM and AI accelerators. Leading manufacturers have reassigned wafer capacity to higher-margin HBM products. The consequence for standard DDR markets has been constrained supply and elevated contract and spot pricing. For buyers, this raises the premium on demand flexibility and supplier diversity strategies.

Price shock and forward curve risk. Contract prices for next-generation DDR segments experienced steep increases in late 2025, and our scenario workmodels several quarters of elevated pricing into 2026 unless fresh fabrication capacity or allocation policies change.

Standards evolution. JEDEC’s recent updates to DDR5 and LPDDR standards materially alter module reliability and performance baselines for server and AI deployments. Engineering teams must incorporate JESD79-5D and related SPD updates into validation plans to avoid time-to-market penalties.

Geopolitics and export controls. Policy measures enacted in 2025–2026, including targeted export controls and critical-mineral negotiations, create additional timing uncertainty for capacity expansion projects and cross-border supply chains. Risk managers should layer political-exposure metrics into procurement and sourcing models.

Concentration and supplier risk. The market remains highly concentrated among a few manufacturers. This concentration amplifies the systemic impact of capacity allocation decisions by any single supplier, making supplier health, capacity roadmaps, and technology node roadmaps critical inputs to scenario planning.

PW Consulting’s competitive analysis foregrounds how each major producer’s strategic posture and capacity choices translate into commercial risk and opportunity for customers, ODMs, and cloud providers.

Samsung Electronics: As the most vertically integrated player, Samsung’s decisions on production extension and DDR5 ramp timing determine much of the market’s supply balance. The company’s selective extension of legacy DDR production through 2026 and aggressive advancement of higher-density DDR5 and HBM capacity create both supply-side constraints and upgrade opportunities for enterprise customers seeking validated high-performance modules.

SK hynix: SK hynix’s emphasis on server- and AI-oriented DDR5 reinforces the bifurcation between commodity standard modules and premium, high-performance inventories. Their capacity choices and node migration timelines directly influence pricing dynamics in enterprise segments.

Micron Technology: With a high-margin focus and a broad enterprise-facing portfolio, Micron’s strategy centers on supplying higher-density DDR5 optimized for data-center use cases. Their product mix and commercial allocation strategy make them a pivotal counterparty in negotiating supply contracts for critical deployments.

CXMT (ChangXin Memory Technologies): CXMT’s emergence as a growing alternative supplier at advanced nodes introduces a new competitive variable—particularly in regional procurement strategies where supply-chain diversification is a priority.

Nanya Technology and Winbond: These players occupy distinct niches—Nanya in mainstream DDR continuity and Winbond in specialty and embedded DRAM—both of which are important to OEMs balancing performance requirements with supply continuity.

Our report provides vendor scorecards that synthesize capacity, node roadmap, declared allocation policies, and supplier resilience. For confidentiality and commercial reasons these granular supplier matrices and vendor-specific volume forecasts are available in the full report package.

Production adjustments: Leading manufacturers have extended DDR4 production windows into late 2026 while prioritizing DDR5 and HBM capacity—an operational trade-off with immediate pricing implications for legacy and transitional modules.

Standards updates: JEDEC’s recent releases refine DDR5 and LPDDR requirements relevant to server, AI, and mobile platforms. These updates accelerate the need for compatibility testing and module validation cycles.

Policy shifts: Government actions addressing critical-mineral flows and ongoing export control regimes impose additional lead-time and localization considerations for capital projects and cross-border procurement.

PW Consulting’s report translates these dynamics into a concise, prioritized playbook that executives can execute immediately. Key recommendations include:

Adopt a tiered procurement posture: blend long-term supply contracts for core capacity with tactical spot purchases to capture price anomalies. Contract duration and flexibility clauses should be renegotiated to reflect current allocation volatility.

Accelerate validation and qualification workflows for DDR5 and updated SPD profiles. Engineering teams that front-load compatibility testing will avoid downstream integration delays as module mixes evolve.

Implement supplier resiliency KPIs: incorporate exposure to single-supplier allocation, percentage of demand covered by long-term contracts, and the time-to-qualify metric for alternative suppliers into quarterly risk reviews.

Revisit inventory economics: with price volatility higher, holding marginal inventory can be economically optimal if backed by rapid deployability and defined obsolescence protections.

Embed geopolitical scenario triggers into capex approvals and partner selection. Where applicable, consider near-shore or allied-region sourcing as an insurance instrument against sudden export-control escalations.

The published summary is a bridge to an operational deliverable set contained in the full PW Consulting study. Clients will receive:

Transparent modeling files with baseline and alternative scenarios, sensitivity analyses, and forward curves for 2026–2032.

Procurement playbooks with contract templates, inventory optimization models, and supplier shortlists segmented by risk appetite and geography.

Engineering and product management checklists aligned to JEDEC updates and module validation timelines.

Vendor scorecards and CRx concentration analysis, mapped to the strategic implications for customers in cloud, enterprise, client, and mobile segments.

Executive dashboards that distill early-warning indicators (capacity reallocations, price index breaks, policy announcements) into actionable signals for board-level decision-making.

Use the report as a living instrument: integrate the dashboard into monthly procurement reviews; require engineering leads to certify DDR5 compatibility milestones; and make capex approvals conditional on scenario-tested returns that explicitly include memory-price volatility. For organizations preparing for major product launches or data-center expansions in 2026, the report’s scenario packages reduce execution risk by converting supply uncertainty into quantified trade-offs.

PW Consulting’s Ddr Ram Market Research is purpose-built to be directly actionable: we show you the market mechanics, expose the levers that matter, and lay out the practical steps that reduce risk and capture upside. In keeping with our “trailer” principle, this release highlights key findings and strategic recommendations while reserving the full segmentation tables, vendor-specific volume forecasts, and contract-level pricing curves for the complete report. These detailed datasets and executable templates are available through our report portal; stakeholders seeking immediate operational support can also arrange custom workshops to translate findings into a bespoke 2026 execution plan.

To access the full report, the interactive dashboards, and our supplier scorecards, please visit the PW Consulting research center or contact our strategy team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Ddr Ram Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com