Does a Skin Booster Injection Work on Aging Neck Skin?

Health |

2026-06-20 06:43:49

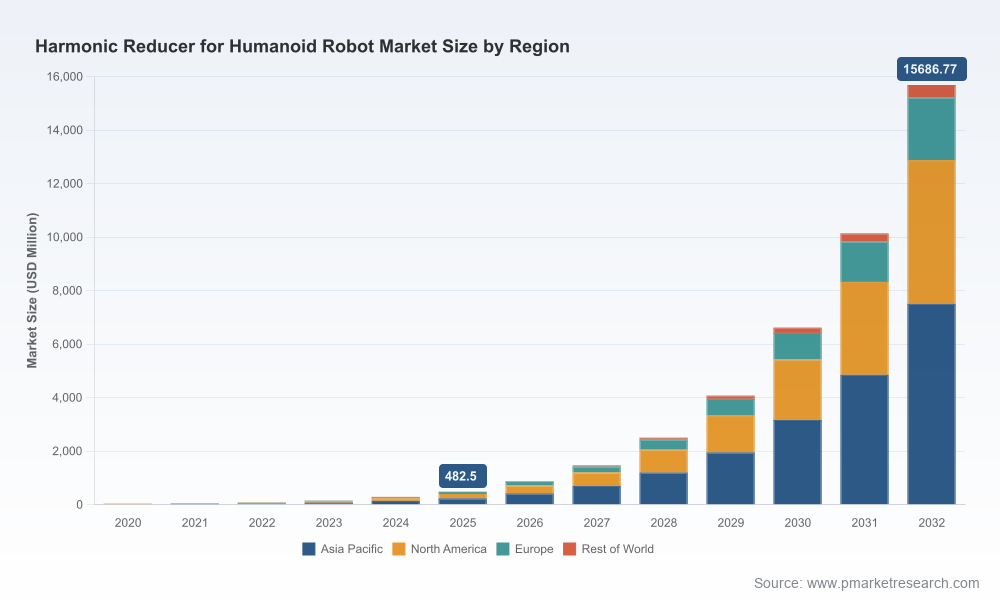

PW Consulting’s latest market intelligence on harmonic reducers for humanoid robots reframes what “scale” and “strategic timing” mean for the next investment cycle. Our analysis consolidates five years of historical data, a detailed 2026–2032 forecast horizon, supplier diagnostics, cost-model frameworks, and scenario planning aimed specifically at executives making procurement, R&D, M&A, and partnering decisions in 2026. At the macro level the market is growing at a sustained, disruptive clip — a compound annual growth rate of 58.94% — rising from early-stage niche volumes to an industry measured in multiple hundreds of millions by 2025 and projecting into the multi-billions by the end of the decade. That scale transforms harmonic reducers from a component procurement decision into a strategic axis for humanoid platform competitiveness.

Harmonic Reducer For Humanoid Robot Market

Timing: 2026 is the inflection point where actuator-level performance and system economics intersect; choices now lock in long-term cost structure and product differentiation.

Harmonic Reducer For Humanoid Robot Market

Supplier Strategy: The sector shows high supplier concentration at the top — our concentration metrics indicate dominant incumbents control a large share of supply — making supplier selection, dual-sourcing, and strategic partnerships critical.

Harmonic Reducer For Humanoid Robot Market

Technology & Materials: Advances in composite materials and integrated actuator architectures mean design decisions earlier in development cycles materially affect weight, space, and life‑cycle costs.

Regulatory & Safety: Certifications and functional safety are not optional for humanoid joints used in collaborative or mission-critical contexts; achieving them is a multi-quarter program that impacts go-to-market timing.

Market sizing and high-fidelity forecast model (base year 2025, historical 2020–2025, forecast 2026–2032) with scenario branches for conservative, base, and accelerated adoption cases.

Supplier scorecards and benchmarking covering design attributes (backlash, torque density, form factor), manufacturing maturity, quality systems, IP posture, and service capabilities.

Technology roadmaps and performance trade-off matrices that map reducer topology (cup, hat, ultra-thin/pancake and alternative architectures) against joint-level requirements.

Cost-build and total-cost-of-ownership models that account for materials, processing, assembly, testing, warranty exposure, and service models — essential for sourcing negotiations.

Regulatory and safety playbook: certification pathways (functional safety categories, PLe, SIL3) and recommended test protocols for humanoid joint integration.

Commercial strategies and go-to-market templates for OEMs, contract manufacturers, and component suppliers including licensing, JV, and co-development options.

1) Phenomenal market acceleration — but uneven strategic opportunity. The market has moved quickly from embryonic use to broad adoption across experimental and commercial humanoid programs. Measured against our base-case, the industry has already scaled into the hundreds of millions by 2025 and projects into multi‑billion dollar territory over the forecast period. That breadth creates blue‑ocean opportunities for firms who align actuator performance with system-level value (weight, energy efficiency, and reliability).

2) High supplier concentration with clear incumbents. A small group of established suppliers continues to dominate upper tiers of quality and reliability, reflected in high CR3 and CR5 concentration metrics — an important structural reality for procurement teams. Entrants and regional manufacturers are closing gaps rapidly, but top-tier relationships still command premium pricing, preferential capacity, and co-development paths with leading humanoid OEMs.

3) Material and packaging innovation is a force multiplier. Composite and engineered plastics (notably PEEK-based assemblies in several development programs) are delivering meaningful reductions in weight and space, enabling system-level gains in payload and runtime. Designers who adopt these materials early capture both performance and integration advantages, but must plan for qualification timelines and supplier audit processes.

4) Functional safety and certification are gating factors. Leaders in the space are aligning harmonic reducer designs with Category 3 / PLe and SIL3 expectations for safe torque and position control functions, while maintaining ISO 9001 and AS9100 processes for mission-critical applications. Compliance with chemical and environmental standards (REACH, RoHS) and IP-rated testing is becoming a procurement prerequisite.

5) Architecture diversity and the competition for joint-level dominance. Traditional strain-wave harmonic designs remain favored for zero-backlash, high-precision joints. At the same time, hybrid and alternative actuator architectures (integrated gear+motor modules, cycloidal hybrids, compact planetary actuator solutions presented at major trade events) are challenging the harmonic incumbent in specific axes where backdrivability, force control, or integration density are prioritized.

Established precision gear specialists and global incumbents retain leadership on performance and certification readiness. Their strengths are scale, long product pedigrees, and ecosystem relationships with servo providers and integrators.

Regional manufacturers and newer entrants are rapidly improving quality and cost position, often focusing on modular joint assemblies and localized supply to key OEMs; these players are the primary source of pricing pressure and specialization (e.g., ultra-thin or high-efficiency cup-type designs).

OEMs and integrators should evaluate three supplier archetypes: (a) elite precision incumbents for mission-critical axes and long-term reliability, (b) high-value challengers for cost-effective scale and rapid iteration, and (c) platform partners who can co-develop integrated actuator+control solutions.

Investors and corporate development teams should prioritize deal structures that bring forward manufacturing capacity, safety-certification maturity, and lightweight material know-how — these are the assets that accelerate OEM time-to-market.

Lock in multi-year co-development agreements with suppliers that can deliver both prototyping agility and scaled manufacturing capacity. Prioritize suppliers with documented quality systems and functional safety track records.

Invest in material qualification programs (e.g., PEEK and other high-performance polymers) early. The timeline for certifying new materials and assembly processes can exceed product development cycles.

Design for dual‑sourcing and modularity. Given supplier concentration and the pace of technology shifts, architectures that allow swap‑in of alternative reducer types reduce commercial risk.

Build integrated actuator verification laboratories (or secure long-term test partnerships) to compress validation timelines for torque, back-drive, thermal, and life testing under realistic humanoid duty cycles.

Pursue certification roadmaps alongside hardware development. Functional-safety gaps and environmental compliance can be the critical path to market entry in regulated applications.

For investors: favor companies that combine IP in compact, high-reduction assemblies with demonstrable supply scalability and certification pipelines — these create defensible multiples as the sector professionalizes.

Raw-material supply constraints and price volatility can erode margin assumptions; mitigation requires alternative materials strategies and long-lead purchasing agreements.

Regulatory or certification delays can push commercialization timelines; teams must budget for iterative testing and third-party audits.

Technology substitution (e.g., successful alternative actuator architectures) could reallocate value away from some harmonic reducer form factors; continuous benchmarking is essential.

Concentration risk among top suppliers makes contingency planning and inventory strategy non-negotiable for OEMs with aggressive production roadmaps.

Procurement leaders should use the supplier scorecards and cost models to renegotiate terms or qualify alternate sources before committing to large production orders.

R&D teams should map their joint architecture against the report’s performance trade-offs to prioritize materials and actuator choices in upcoming design sprints.

Corporate development teams should overlay the report’s forecast scenarios with their M&A screens to time acquisitions or JVs aligned to market inflection points.

Executives should consult the full report for granular segmentation, supplier-level financial implications, and downloadable models that support board-level decisions; the executive summary here is a strategic primer designed to guide priority setting for 2026.

PW Consulting’s Harmonic Reducer for Humanoid Robot Market report is deliberately structured as a decision‑enablement tool: it delivers the strategic context, actionable frameworks, and supplier diagnostics executives need to convert rapid market growth into sustainable competitive advantage. For the proprietary segmentation, detailed scorecards, and downloadable scenario models that underpin 2026 decision-making, please visit the full report page to access the complete intelligence package.

For detailed analysis of this topic, please visit the official page:Harmonic Reducer For Humanoid Robot Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com