Micro System Analyzer Market — 2026 Strategic Briefing

Introduction

PW Consulting’s new Micro System Analyzer Market report is released as a targeted strategic briefing for senior leaders planning investments, product roadmaps, and procurement strategies in 2026. Built from multi-year primary research and validated forecasting, the study translates instrument-level technical complexity and end-market adoption dynamics into clear business implications. This press summary previews the report’s analytical depth and the strategic choices it enables — while deliberately withholding the full segmented data tables to encourage direct access to the underlying intelligence.

Micro System Analyzer Market

Market snapshot and trajectory

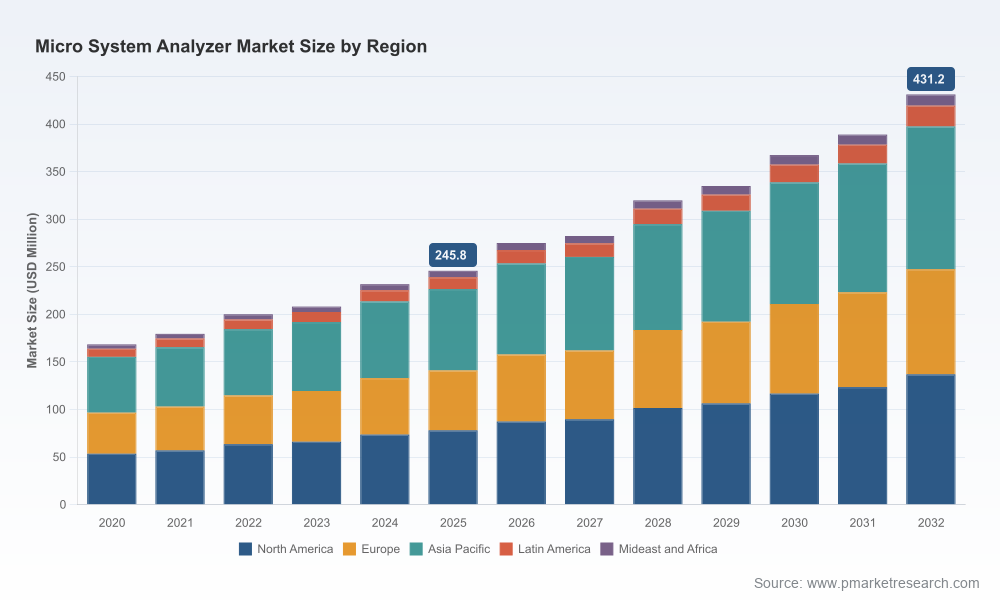

The Micro System Analyzer market has moved from a niche laboratory toolset into a core enabling technology for the broader MEMS and microsystems ecosystem. Our market model (USD Million, base year 2025) shows steady expansion through the 2026–2032 forecast window, underpinned by cross-industry adoption and rising test complexity. After consistent growth during 2020–2025, the market is projected to grow at a compound annual growth rate (CAGR) of 8.36% across the forecast period. The combination of accelerating demand for non-contact dynamic characterization, higher-frequency instrumentation, and integrated software analytics is driving a meaningful upshift in total addressable revenue.

Micro System Analyzer Market

Market concentration remains moderate: the top three suppliers account for approximately 48.6% of the market and the top five about 62.3%. That structure signals a competitive environment where established instrument makers hold scale advantages, yet specialist entrants and solution-focused service providers can capture high-margin niches.

Micro System Analyzer Market

Principal demand drivers and technology inflection points

- Miniaturization and MEMS proliferation — As sensors and actuators shrink and integrate into consumer, automotive, medical, and aerospace products, test complexity rises. Manufacturers increasingly require non-contact, high-bandwidth characterization to avoid mass-loading artifacts and to preserve device integrity at wafer and package levels.

- Dynamic characterization needs — New device classes push dynamic measurement beyond traditional bandwidths. Instruments that can reliably resolve in-plane and out-of-plane motion across broad frequency ranges are central to R&D, reliability testing, and production verification strategies.

- Regulatory and clinical validation pressures — Medical and biomedical MEMS are subject to rigorous regulatory scrutiny. Non-contact optical metrology solutions that support vibration, acoustic, and reliability testing without altering device behavior provide a clear compliance advantage for medical-device development programs.

- Software and analytics — Hardware commoditization creates room for software-driven differentiation (analysis pipelines, automated test sequences, digital twins). Buyers are valuing integrated analytics, traceability, and standardized KPIs alongside instrument performance.

- Service and lab-as-a-service models — CapEx constraints and the need for specialized expertise are accelerating outsourced test services and on-demand access to advanced measurement platforms.

What the report delivers — practical, operational intelligence

Beyond headline forecasts, the PW Consulting Micro System Analyzer report is structured to support operational decision-making in 2026. Key deliverables include:

- Proprietary market model and scenario engine — flexible, downloadable models that let users test bespoke assumptions (adoption curves, price erosion, regional pacing) without exposing sensitive segment tables in this summary.

- Technology assessment framework — side-by-side evaluation criteria for optical, stroboscopic, and interferometric approaches, including measurement envelopes, throughput implications, and integration complexity.

- Vendor scorecards and capability matrices — balanced profiles that highlight product families, support footprints, and service models (note: the full scorecards and numerical rankings are part of the full report).

- Buyers’ playbook — procurement checklists, acceptance test protocols, lifecycle cost models, and KPIs tailored to R&D, wafer-level testing, and production QC use cases.

- Go-to-market and commercial strategy templates — recommended channel structures, pricing levers, and value-added service bundles for instrument manufacturers and lab operators.

- Regulatory and validation impact analysis — practical guidance for integrating non-contact metrology into medical device development pathways to minimize regulatory friction.

- Case studies and deployment blueprints — anonymized examples showing timelines, resourcing, and measured ROI for several representative adopter profiles.

Competitive landscape — focus on capability, not conjecture

Our competitive analysis highlights a mix of established optical-instrument vendors and specialized measurement startups. Polytec GmbH stands out as the primary active manufacturer of dedicated Micro System Analyzer product lines. With an established MSA portfolio — including integrated optical, non-contact workstations capable of static and dynamic 3D characterization — Polytec’s capabilities exemplify the class of solutions that buyers are prioritizing:

- All-in-one measurement workstations designed for surface topography and multi-axis vibration analysis.

- High-frequency dynamic characterization supporting both in-plane and out-of-plane motion at bandwidths relevant to cutting-edge MEMS designs.

- Application coverage that explicitly includes biomedical samples and medical-device testing, enabling wafer-level testing and reliability assessment without mass loading — an important differentiator where regulatory validation is critical.

Polytec and similar incumbents benefit from mature optics expertise, broad instrument portfolios, and installed service bases. However, their positioning also highlights the strategic openings available to challengers: modular architectures, cloud-enabled analytics, lab-network orchestration, and turnkey measurement-as-a-service offerings.

Strategic implications for 2026 decision-makers

Whether you are a device OEM, a test-equipment OEM, an investor, or a lab operator, the market dynamics identified in our report point to clear near-term choices:

- For device OEMs: codify measurement requirements early in the design lifecycle. Prioritize non-contact dynamic metrology for validation routines where regulatory or functional risk from mass-loading is material.

- For instrument manufacturers: invest in software and service layers. Hardware differentiation will narrow; recurring revenue from analytics, calibration services, and managed lab access will drive valuation premiums.

- For lab operators and service providers: scale lab networks with standardized test stacks and self-service portals to capture OEMs’ outsourcing demand while reducing per-test marginal costs.

- For investors and M&A strategists: target assets that combine precision optics with digital analytics and a path to recurring revenue. Look for tuck-in opportunities that accelerate time-to-market for lab-as-a-service offerings.

- For regulatory and QA leaders: align measurement protocols with non-contact capabilities to shorten approval cycles in regulated segments such as medical devices. Early engagement with instrument vendors on traceability and calibration is essential.

Risks, blind spots, and tactical mitigations

- Supply-chain and component risk — precision optical systems depend on specialized subcomponents; diversify suppliers and validate long-lead items in capital plans.

- Skill and training gaps — advanced metrology requires skilled operators. Invest in training programs and remote-support capabilities to reduce adoption friction.

- Standardization deficiencies — lack of industry-wide test standards for certain MEMS dynamics can create procurement ambiguity; proactive development of test standards (or alignment to vendor-neutral protocols) can accelerate uptake.

Why PW Consulting’s report is essential for 2026 decision cycles

This report is engineered to convert metrology complexity into boardroom-grade decisions. It blends a rigorous market model (with customizable scenarios), vendor capability analytics, tactical procurement tools, and regulatory impact mapping. We validate our findings through primary interviews, instrument-level bench tests, and cross-checks against public and proprietary datasets. The summary presented here demonstrates the scale, growth trajectory, and competitive contours — while the full dataset, segmentation tables, and granular vendor scorecards are provided in the complete deliverable and data portal.

Next steps

Executives preparing capital plans or product roadmaps in 2026 should prioritize three actions now: (1) request the PW Consulting market model to stress-test internal assumptions, (2) run a blind technical evaluation of candidate measurement suppliers against your acceptance criteria, and (3) pilot a lab-as-a-service engagement to validate commercial models with minimal capex. Detailed templates, checklists, and the full segmentation and vendor benchmarking are available in the full report.

PW Consulting’s Micro System Analyzer Market report equips leaders to turn measurement complexity into strategic advantage. For full access to the market tables, scenario models, and vendor scorecards referenced in this briefing, please consult the report landing page.

For detailed analysis of this topic, please visit the official page:Micro System Analyzer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com