Hematology Diagnostics Market to Reach US$ 7.6 Billion by 2031, Driven by Rising Demand for Advanced Blood Testing and Precision Healthcare

Other |

2026-06-03 06:43:52

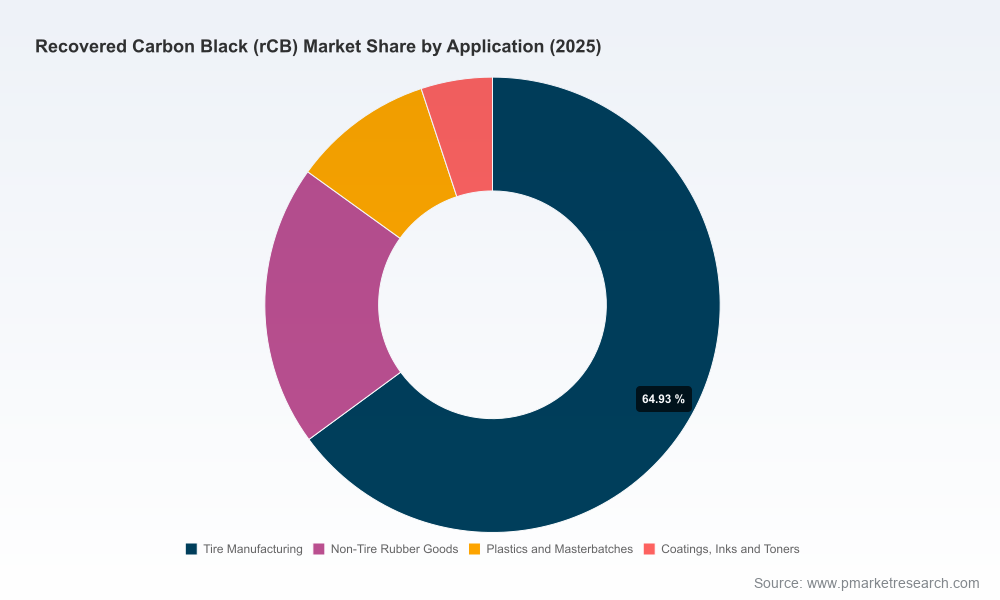

As circularity moves from corporate ambition to procurement condition, recovered carbon black (rCB) is rapidly transitioning from pilot technology to strategic raw material. PW Consulting’s new Recovered Carbon Black (rCB) Market study—based on a 2025 base year and a 2026–2032 forecast horizon—quantifies that transition and translates it into actionable choices for executives planning capital allocation, sourcing strategies, and product roadmaps in 2026. The market grew from approximately USD 425 million in 2020 to roughly USD 718.5 million in 2025, and our model projects a continued compound annual growth rate (CAGR) of 11.5% through the 2026–2032 forecast period, pushing the market well into the billion‑dollar range by the end of the decade.

Recovered Carbon Black Rcb Market

Supply security and input cost volatility: rCB converts a growing waste stream (end‑of‑life tires) into a reusable feedstock, altering how tire makers and polymers processors manage raw‑material risk.

Recovered Carbon Black Rcb Market

Regulatory and procurement tailwinds: policy recognition of tire pyrolysis as a recovery process within core jurisdictions, combined with certification frameworks for circularity, creates both compliance incentives and market access hurdles.

Recovered Carbon Black Rcb Market

Commercial maturation: a meaningful cohort of commercial‑scale producers and strategic industry partnerships have moved rCB from demonstration to contracted supply, enabling multi‑year supply agreements and industrial adoption pathways.

Our base‑case market model, grounded in historical observations (2020–2025) and bottom‑up plant and demand build‑out through 2032, indicates a structurally resilient market expanding at ~11.5% CAGR over the forecast window. This trajectory is not linear: growth is driven by clustered capacity additions, certification milestones that unlock procurement mandates, and accelerating substitution in mid‑performance applications. The model explicitly scenarios demand penetration across tire and non‑tire uses, price arbitrage vs. virgin carbon black, and logistics/supply constraints—each of which can materially affect timelines for adoption at a corporate portfolio level.

Pyrolyx AG (Germany) — A commercial producer using proprietary pyrolysis technology. Recent capacity expansion to first commercial‑scale production in Germany (announced 2023) demonstrates the feasibility of scaled domestic supply for European tire and industrial customers. Their product grading strategy targets parity with established reinforcement grades.

Black Bear Carbon B.V. (Netherlands) — Now operating at industrial scale following a major milestone in 2023 supported by strategic backing that includes a global tier‑1 OEM. This supplier‑OEM alignment is a template for how offtake, technical collaboration, and co‑investment de‑risk market entry for both sides.

Enviro AB (Sweden) — The company has secured ISCC PLUS certification for its pyrolysis‑based rCB, a critical enabler for customers requiring audited mass‑balance and sustainability claims. Certification is increasingly a gating criterion for procurement in regulated markets.

Hi‑Green Carbon Limited (India) — An example of regional manufacturing scale‑up in cost‑sensitive markets, offering multiple grades and ISCC‑aligned products. Regional tax and trade regimes will shape where production and consumption scale fastest.

Market concentration is moderate and evolving: the top three suppliers account for a meaningful but not dominant share of industry output, and the top five consolidate roughly half of current capacity. That concentration profile signals both the presence of scale economics and opportunity for new entrants with differentiated technology, feedstock access, or integrated value propositions.

Policy recognition: In key jurisdictions the classification of tire pyrolysis as a recovery process enables rCB to be treated as a non‑waste commercial input—unlocking procurement by OEMs and industrial buyers that must demonstrate circular sourcing.

Certification regimes: Standards such as ISCC PLUS are becoming de facto requirements for customers that need mass‑balance accounting and traceability; producers without certification face restricted market access.

Feedstock economics: Tire feedstock prices have moved materially in recent periods as recycling demand and logistics constraints tighten supply. This dynamic transmits into rCB unit economics and regional arbitrage.

Trade and tariff frictions: Import duties, for example region‑specific taxes on rCB imports, materially affect where downstream processors choose to source or locate capacity.

Material performance ceiling: Technical limitations remain—commercial rCB purity typically ranges below virgin carbon black in the highest‑performance applications, limiting immediate displacement in premium tire treads and demanding blended or tiered product strategies.

The report is structured to serve both strategic and commercial users and contains the following operationally focused elements:

Market model and scenarios — detailed top‑down and bottom‑up demand forecasts (2026–2032), sensitivity testing for price and certification penetration, and risk‑weighted adoption curves.

Vendor due diligence packs — standardized manufacturer profiles, technology readiness assessments, capital intensity benchmarks, and commercial risk matrices for leading and emerging producers.

Supply‑chain maps — feedstock flow analysis, logistics cost buckets, and practical supplier qualification checklists for procurement teams.

Policy & certification playbook — regulatory mapping across major markets, checklist for ISCC PLUS alignment, and engagement templates for policymakers and industry consortia.

Commercial templates — term‑sheet examples for offtake agreements, sample cost‑builds, and a pricing outlook to support contract negotiations.

Investment case modules — capital expenditure sizing for greenfield rCB plants, break‑even and IRR sensitivities, and M&A acquisition screening criteria.

Note: while this synopsis outlines the report architecture and key takeaways, detailed regional/application splits, vendor‑level cost curves, and granular revenue forecasts are available exclusively in the full report and online dashboard.

For tire OEMs: Lock in blended supply strategies that combine rCB and virgin grades for tread and sidewall families; pilot co‑processing in compounding lines during 2026 while securing certified offtake for sustainable product lines.

For polymer processors and compounders: Prioritize formula migration studies to identify segments where rCB meets performance needs today and establish dual‑sourcing contracts to capture near‑term cost and sustainability upside.

For rCB producers and technology providers: Invest selectively in capacity where policy classification and feedstock access reduce market entry risk; pursue ISCC or equivalent certification early to shorten sales cycles with conscious buyers.

For investors: Model deal returns under multiple policy and certification adoption scenarios; prefer assets with proven quality specs, off‑take backing, and proximity to feedstock to protect margins.

For governments and trade bodies: Harmonize certification expectations and avoid punitive trade barriers that could fragment global supply chains and discourage scale economies.

Quality ceiling risk: The intrinsic purity gap between rCB and virgin carbon black constrains penetration in premium segments. Mitigation: focus on blended applications and incremental material innovation to push grade quality upward.

Feedstock competition: As demand for tire‑derived feedstock grows, prices and collection logistics may tighten. Mitigation: vertical integration into collection networks or long‑term feedstock contracts.

Regulatory divergence: Different regional classifications and import duties can create arbitrage and unpredictability. Mitigation: diversify production footprint and secure certifications that carry cross‑jurisdictional recognition.

By 2026 the rCB market will have moved definitively into commercial application across a spectrum of use cases, but the pace and shape of adoption will depend on a handful of binary outcomes: certification adoption rates, the trajectory of feedstock economics, and the degree to which producers can close the quality gap to virgin carbon black. For executives planning 2026 actions, the strategic priority is clear: convert experimental procurement and partnerships into contracted supply‑chain architecture that balances sustainability, cost, and performance risk.

PW Consulting’s full Recovered Carbon Black (rCB) Market report contains the datasets, vendor profiles, contractual templates, and model access required to convert insight into contracts and investments. The executive summary is available for immediate download, while the complete dataset and interactive dashboard—containing the country and application detail, supplier‑level metrics, and scenario tools—are available through our website. Contact PW Consulting to arrange a briefing or to license the model for internal use in 2026 planning cycles.

For detailed analysis of this topic, please visit the official page:Recovered Carbon Black Rcb Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com