Can I Track Order Status in a Top Mutual Fund Software in India?

Other |

2026-06-26 09:27:53

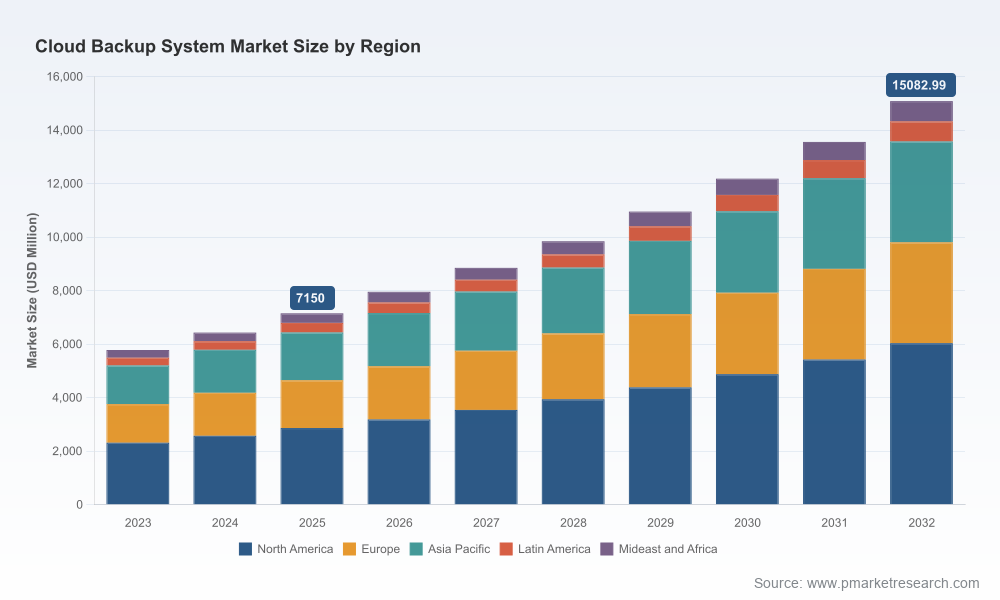

As enterprises enter 2026, cloud backup has shifted from a tactical insurance policy to a strategic infrastructure pillar. PW Consulting’s latest Cloud Backup System Market report — built on a 2025 baseline and a five-year historical window (2020–2025) — projects a sustained expansion through our forecast horizon (2026–2032). The global market, having reached USD 7,150 Million in 2025, is expected to grow at a compound annual growth rate (CAGR) of approximately 11.25%, more than doubling to roughly USD 15,083 Million by 2032. These macro dynamics belie structural changes in regulation, energy economics, vendor go-to-market models, and risk calculus that will decisively influence enterprise technology and procurement choices in 2026.

Cloud Backup System Market

Regulatory pressure and compliance complexity — New reporting mandates and energy-efficiency directives, such as the EU’s strengthened requirements around PUE and WUE, are forcing IT and facilities stakeholders to treat backup strategy as part of broader sustainability and audit programs. Backup architectures now carry reporting obligations that go beyond data protection: they influence corporate ESG disclosures and facility-level compliance.

Cloud Backup System Market

Energy and infrastructure costs — Rising data center construction and operating costs (industry projections indicate construction outlays averaging around USD 11.30 million per MW in 2026, with upward pressure on power pricing) are reshaping placement and retention strategies for backup workloads. The electricity intensity of large-scale compute also factors into resiliency design and vendor SLAs.

Cloud Backup System Market

Data sovereignty and edge proliferation — Persistent data sovereignty regimes and privacy frameworks are accelerating localized and edge data center deployments. Backup strategies must therefore contend with hybrid topologies and distributed recovery objectives that include local retention, regional vaulting and compliance-aware failover.

Security and resiliency economics — The ransomware threat landscape and the growth of cyber insurance tie data protection more explicitly to business continuity. Buyers are prioritizing demonstrable cyber-resilient features — immutable storage, air-gapping, automated recovery playbooks — as part of procurement criteria and insurance negotiations.

We designed the Cloud Backup System Market report as a playbook for 2026 decision-makers. Rather than abstract high-level forecasts alone, the report contains an integrated set of practical tools and analytics that firms can use immediately:

Market sizing and forward scenarios — A rigorous top-down and bottom-up model covering 2020–2025 history and multiple forecast scenarios for 2026–2032, enabling stress-testing of CAPEX and OPEX plans against upside/downside demand and energy-price pathways.

Purchase and procurement frameworks — Decision matrices that map workloads to backup modalities (cloud-native, cloud-to-cloud, hybrid, and edge) with vendor shortlists, scoring criteria and contract negotiation playbooks tailored to SLA, recovery time objectives (RTO), recovery point objectives (RPO) and compliance clauses.

Implementation playbooks and TCO models — Step-by-step migration pathways, cost breakdowns, and three-year TCO comparators that incorporate energy and data transfer costs, storage tiering, and retention policies to surface hidden lifecycle costs.

Cyber-resilience templates — Operational runbooks, breach-recovery simulations and evidence packages aligned with insurer and regulator expectations to reduce mean-time-to-recovery and preserve post-incident reputational capital.

Vendor feature matrix and integration maps — An anonymized but detailed capability comparison across form-factor, security features, automation, ransomware protection, backup frequency support and cloud-native integration patterns.

Region- and industry-specific advisories — Practical recommendations for regulated industries (financial services, healthcare, telecom) and for regions grappling with sovereignty or energy constraints, including alternative architectures for constrained power environments.

The market exhibits a moderate level of concentration. The top three vendors account for just under 40% of market share, while the top five approach the low‑50s — a structure that supports both deep enterprise incumbency and continual disruption by specialized providers. Our competitive analysis focuses on three axes: platform breadth, hybrid integration capability, and cyber-resilience innovation.

Hyperscalers (AWS, Microsoft Azure, Google Cloud) — These providers continue to press advantages in integrated, policy-driven backup services that simplify centralization across native cloud services and hybrid workloads. Their strengths are scale, regional footprint, and deep integration with adjacent cloud platform services, while buyers must weigh lock‑in risks and cross-cloud recovery complexity when relying solely on hyperscaler-native tooling.

Enterprise-focused incumbents (Veeam, Commvault, Veritas) — These vendors are executing on multi-cloud and cyber-resilience plays. Recent product updates and tighter platform integrations — including extended scanner coverage, air-gap protect features and deeper DR capabilities — signal an emphasis on cross-platform continuity and automated recovery orchestration.

Next‑gen specialists (Rubrik, Druva, Cohesity, Acronis) — Smaller, agile vendors are differentiating on automation, ransomware detection/response, and SaaS-delivered simplicity. Partnerships and recognitions (for example, channel acknowledgements between cloud vendors and specialist providers) point to an ecosystem where best-of-breed and hyperscaler offerings coexist and intertwine.

Cost-focused entrants (Backblaze, Barracuda) — These players compete on price and straightforward backups for specific use cases (SaaS app protection, endpoint consolidation). They are attractive for SMBs and for large-scale cold-storage strategies as part of tiered retention.

Recent vendor developments underscore rapid feature evolution: new releases in early 2026 enhanced backup cadence and scanner coverage across major cloud platforms; partner recognitions and expanded collaborations indicate an accelerant toward integrated multi-vendor solutions; and incremental product pushes target ransomware detection and automated recovery orchestration. Collectively, these moves compress time-to-value but raise the bar on interoperability and governance.

Adopt a workload-centric backup taxonomy — Map business-criticality to recovery objectives and cost-to-restore. Treat backup policy as a dynamic cost center that is revisited quarterly as energy and regulatory conditions evolve.

Design for hybrid and multi-region resilience — Combine local retention for immediate recovery with geo-diverse vaulting for compliance and disaster scenarios. Explicitly model cross-region egress and transfer costs into procurement decisions.

Require cyber-resilience KPIs in contracts — Embed measurable ransomware resilience metrics (time-to-restore, immutability guarantees, restoration validation) and tie portions of vendor compensation to demonstrable recovery outcomes.

Incorporate energy and sustainability constraints into backup policies — Work with facilities and sustainability teams to align retention and compute scheduling with PUE/WUE objectives and utility tariff optimization strategies.

Negotiate ecosystem integration and escape clauses — Given hyperscaler dominance in platform-native backups, ensure contractual flexibility to port data or orchestrate cross-cloud recovery without prohibitive penalties.

Use proof-of-value pilots with rigorous success criteria — Short, measurable pilots reduce rollout risk and clarify hidden costs around network egress, restore performance and operational overheads.

Vendors must balance breadth and depth: platform incumbency requires continuous investment in security and automation, while specialized vendors can win with superior UX, stronger cyber-resilience features and channel strategies. Investors should look for companies that can demonstrate sticky enterprise contracts, differentiated recovery IP, and unit economics resilient to rising data centre construction and energy costs. Partnerships between hyperscalers and best-of-breed backup vendors are emerging as effective go‑to‑market accelerants — a pattern that will create attractive consolidation and growth opportunities.

Organizations using our report will gain a compact, executable strategy for vendor selection, contractual negotiation, sustainability alignment and incident-readiness. The report’s scenario suite helps CFOs and CTOs evaluate alternatives under varying energy-price, regulatory and threat-intensity trajectories. The tactical annexes — from procurement templates to automated recovery runbooks — enable immediate implementation without waiting for bespoke consulting engagements.

This article summarizes the strategic value of PW Consulting’s Cloud Backup System Market report for decision-makers in 2026. The full report contains the detailed segmentation, vendor scorecards, downloadable TCO models and confidential annexes that enterprises and investors need to act. For executives who require the underlying tables, scenario outputs, and step-by-step playbooks, please visit PW Consulting’s report page to license the complete study and supporting datasets.

For detailed analysis of this topic, please visit the official page:Cloud Backup System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com