Closeouts Market 2026 — Strategic Preview from PW Consulting

PW Consulting’s Closeouts Market report (base year 2025; forecast 2026–2032) provides a decision-ready lens for executives shaping go-to-market, procurement, and capital-allocation choices in 2026. The market we track is substantial and expanding: by our accounting the closeouts industry reached approximately USD 285.5 Billion in 2025 and, under our central forecast trajectory, is on course to approach roughly USD 454.0 Billion by 2032 — an implied compound annual growth rate of 6.85% through the forecast window. This briefing highlights the report’s strategic value without revealing the granular splits reserved for subscribers; consider this a trailer that demonstrates analytical depth while directing you to the full dataset for transaction-grade detail.

Closeouts Market

Why this report matters for 2026 decisions

- Actionable market sizing: The market’s near-term resilience and mid-term growth signal both cyclical arbitrage opportunities and durable structural channels for secondary-value capture across retail ecosystems.

- Platform-driven disruption: Digital auction and wholesale marketplaces are reshaping price discovery and time-to-liquidity for surplus inventory — a dynamic that impacts margins across retail, manufacturing, and distribution.

- Policy and macro risk: Trade policy (notably U.S. tariff passthrough to consumer categories) and heightened insolvency events among retailers are driving volatility in supply and pricing. Firms that incorporate tariff-sensitivity and bankruptcy-driven inventory influx into planning will materially outperform peers.

- Fragmentation = optionality: Market concentration remains low relative to mainstream consumer-goods channels, creating immediate opportunities for scale plays, roll-ups, and specialized vertical strategies.

What’s inside the report — practical deliverables

- Proprietary market model (base 2025, forecast 2026–2032) that converts macro drivers into demand-supply scenarios and revenue trajectories in USD Billion, including sensitivity to tariffs, consumer demand elasticity, and liquidation velocity.

- Competitive mapping and capability matrices for leading platform operators, auction houses, wholesalers, and B2B resellers; each profile includes business models, typical supplier relationships, monetization levers, and go-to-market vectors.

- Operational playbooks: pallet-to-retailer margin archetypes, auction cadence optimization, grading & inspection protocols, and recommended SLAs for buyer-seller platforms that materially reduce return rates and increase recovery.

- Data suite and dashboards: calibrated KPIs (days-to-liquidation, recovery rate, price-realization index, buyer-lift by channel) and a template analytics stack for near-real-time monitoring.

- M&A & partnership decision framework: screeners for tuck-in targets, valuation heuristics for platform vs. physical-asset businesses, and integration KPIs to capture synergies quickly.

- Scenario-based strategic roadmaps (immediate, medium, long term) tied to three policy and demand scenarios — each with recommended capex, commercial, and inventory-management plays.

- Compliance and risk annex: customs and tariff playbooks, cross-border logistics checklists, and recommended contractual language for supplier agreements in high-tariff environments.

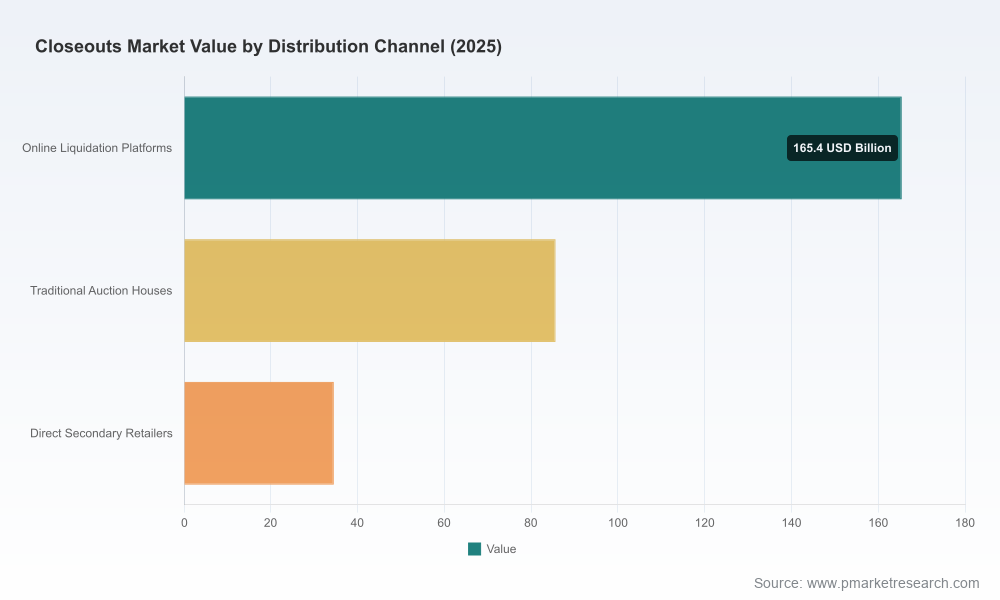

Note: the report reserves detailed regional, product-category, and distribution-channel splits for our subscribers and clients. These granular tables are intentionally withheld in this preview to protect the optimized intelligence that informs transactional decisions.

Closeouts Market

Competitive landscape: who moves the market

The closeouts ecosystem is populated by three functional archetypes: platform marketplaces that connect large institutional sellers with an on-demand buyer base, pallet- and truckload wholesalers with physical logistics scale, and specialized B2B resellers that curate niche channels. Representative firms that illustrate these archetypes include:

Closeouts Market

- Platform marketplaces: B-Stock and Liquidation.com — digital-first businesses that enable retailers and manufacturers to auction returns and overstock globally, leveraging buyer networks and automated bidding to enhance price discovery.

- Large-scale liquidators and wholesalers: Direct Liquidation, BULQ, and UpLiquidation — operators with significant logistics capabilities, reverse-supply-chain know-how, and relationships across retail estates.

- B2B specialists and import-distributors: Overstock Trader, Total Surplus Solutions, Kole Imports, and Countryside Closeouts — firms that trade on curation, off-price retail channels, and local reseller networks.

- Market intermediaries: Global Distributors and other regional consolidators who coordinate loads, grading, and distribution into secondary retail and export channels.

Two structural conclusions emerge from our competitive read:

- The market’s CR3 and CR5 concentration metrics are low (indicative of a fragmented competitive set), making it amenable to consolidation and partnership plays for any firm that can combine scale with superior data and logistics.

- Digital platforms that invest in buyer quality controls, pricing algorithms, and transparent grading systems are increasingly capturing higher price realization and faster turnover, creating an advantage that physical wholesalers must neutralize through service differentiation and supply exclusivity.

Recent dynamics shaping 2026 strategy

- Trade shows and supplier ecosystems: Industry events such as ASD Market Week (March 2026) continue to be critical deal forums, surfacing supplier innovations and accelerating B2B matchmaking across over 250 suppliers.

- Policy volatility: Ongoing tariffs on imported consumer categories are exerting uneven cost pass-throughs across electronics, apparel, toys, and household items — an input shock that affects liquidation pricing, cross-border arbitrage, and the attractiveness of export channels.

- Supply-side shocks: Elevated levels of overstock driven by cautious consumer spending patterns and increased insolvencies among specialty retailers have expanded available inventory pools, compressing short-term recoveries but creating long-term volume opportunities for scale players.

Strategic implications and prioritized actions for 2026

Executives need a short list of calibrated actions that translate market intelligence into faster cash recovery, improved margins, and optionality for expansion. We recommend the following prioritized roadmap:

- Immediate (0–6 months): Implement tariff-sensitivity stress tests across SKU categories; convert high-risk SKUs to digital-auction channels to accelerate turnover; add grading and condition-code standardization to reduce buyer disputes.

- Near-term (6–18 months): Invest in platform partnerships or build lightweight marketplace capabilities — prioritize buyer-quality uplift, data-driven floor-pricing, and integrated reverse-logistics to improve recovery rate by several percentage points.

- Medium-term (18–36 months): Execute targeted M&A to aggregate supply (geography or category roll-ups) and capture warehousing/logistics synergies; deploy advanced analytics for dynamic allocation between auction, wholesale pallet, and direct secondary retail channels.

Operational KPIs to track execution include days-to-liquidation, realized recovery as a percentage of retail price, buyer churn by channel, and tariff-driven margin erosion. In addition, institutions should adopt a decision rule for inventory triage that converts SKU-level forecasts and tariff-exposure into predetermined disposition pathways (auction, pallet, export, charitable donation) to remove ad hoc decision friction.

Three scenarios to test strategy against

- Accelerated consolidation: Platform economics push market concentration higher; winners are those that combine superior data with logistics. Focus: scale M&A and tech integration.

- Tariff-driven arbitrage: Persistently high tariffs create export arbitrage and favor local liquidation; focus on cross-border compliance capabilities and diversified destination channels.

- Structural oversupply: Continued retail stress maintains elevated overstock; value accrual shifts to those who can monetize volume through optimized grading, refurbished-product channels, and downstream secondary retail relationships.

Each scenario maps back to the same directional growth profile (our central case assumes a 6.85% CAGR through 2032) but implies materially different allocation of capex and commercial effort. The playbooks in the full report map those levers to financial outcomes and integration checklists.

How PW Consulting can help

We support boards and executive teams with rapid diagnostics built on the report’s data model, including custom scenario runs, acquisition target screens, and operational playbooks tailored for logistics footprint and buyer-network composition. For clients preparing 2026 budgets, we can produce a tailored “liquidation value capture plan” that converts market dynamics into a three-year P&L and cash-impact dashboard.

Next steps — where to get the full intelligence

This preview underscores the breadth and applicability of the Closeouts Market report as a 2026 strategic input. The full report includes the detailed regional, product-category and distribution-channel breakouts, complete company profiles and financial heuristics, and the downloadable data model used to generate our forecasts and scenario outputs. To access the complete dataset, buyer playbooks, and subscription options, please visit our report page (link in the release) or contact PW Consulting’s research team for a private briefing.

For leaders tasked with converting surplus into strategic advantage in 2026, the difference between reactionary discounting and disciplined value capture will be driven by the combination of data, logistics, and policy-aware playbooks — exactly what PW Consulting’s Closeouts Market report is designed to deliver.

For detailed analysis of this topic, please visit the official page:Closeouts Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com