Facioscapulohumeral Muscular Dystrophy Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-15 11:24:19

As senior strategic advisor and chief industry analyst at PW Consulting, I present a concentrated preview of our latest Baby Monitoring System Market report — an operationally focused intelligence package designed to shape executive decisions in 2026. This brief distills the report’s strategic value, highlights the macro trajectory and competitive dynamics of the market, and outlines the practical pathways we recommend for product, channel, and regulatory strategy — while reserving the full granularity for the complete report.

Baby Monitoring System Market

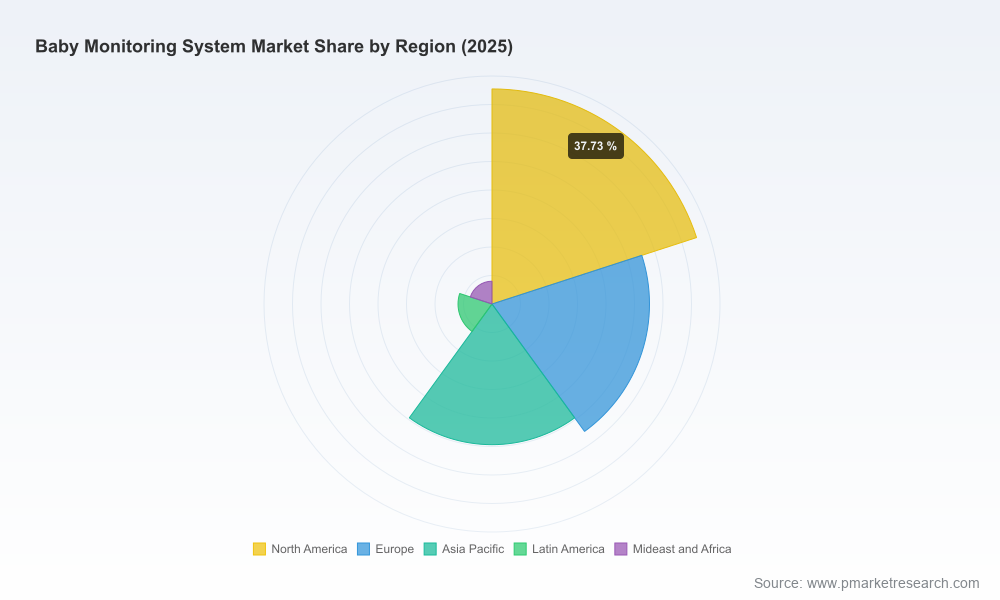

Our modelling places 2025 as the analytical base year. The global baby monitoring system market is estimated at roughly 1,850 USD Million in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of 8.7% across the 2026–2032 forecast horizon. By the end of the forecast window the market reaches the low‑thousands (USD Million), reflecting sustained consumer demand for video, audio, and increasingly smart/connected monitoring solutions.

Baby Monitoring System Market

This growth is not homogeneous: technology transitions, evolving privacy regulation, and channel shift dynamics create pockets of accelerated adoption as well as transient softness in specific quarters. Importantly, market concentration is moderate — the top three players account for about one-third of the market, and the top five just under half — a structure that enables both scale advantages for incumbents and continued opportunity for differentiated entrants.

Baby Monitoring System Market

Actionable growth scenarios: We translate the headline CAGR into investor‑grade scenarios and short‑cycle tactical plans for R&D, manufacturing, and channel investments.

Regulatory-to‑product roadmaps: The report maps immediate compliance pathways (privacy-by-design, edge processing, end-to-end encryption) into product development timelines so teams can convert regulatory risk into competitive advantage.

Commercial playbooks: From premium smart monitors to value audio units and omnichannel distribution, we provide go-to-market templates and margin models geared to 2026 market realities.

M&A and partnership screening: We screen technology adjacencies (AI sleep analytics, wearable vitals, home-security convergence) and provide a prioritized short list of capability targets for bolt-on acquisition or JV.

Methodology & datasets: Transparent modelling assumptions, primary interviews, and a replicable forecasting engine keyed to product, channel, and regulatory variables.

Executive playbooks: Board‑level recommendations, 90‑day tactical checklists, and a 24‑month product and commercialization roadmap tailored to different budget and risk appetites.

Technology & product intelligence: Comparative assessment of sensor types, connectivity architectures (Wi‑Fi vs. low‑power alternatives), on‑device vs. cloud AI processing, and recommendations for firmware lifecycle management.

Channel & pricing models: Optimized margin ladders for online-first vs. traditional retail distribution, and guidance on bundling wearables with camera systems to maximize basket size and retention.

Regulatory & security playbooks: Step‑by‑step compliance templates for jurisdictional requirements, privacy impact assessment templates, and engineering specifications for secure provisioning and certificate management.

Competitive benchmarking: Strategic profiles, strengths/weaknesses, and near‑term moves for the market’s most consequential players, plus indicators to watch for shifts in market power.

The market features a mix of legacy consumer electronics brands, specialist baby‑care players, and a cohort of focused smart‑device startups. Key firms profiled in the report include long‑standing global electronics incumbents and specialist innovators — each with distinct strategic positions. Incumbents bring distribution scale and brand trust; specialists drive feature innovation (wearables, AI sleep analytics) and rapid product iteration; and smart‑home vendors aim to fold baby monitoring into broader connected‑home value propositions.

Large consumer electronics and baby‑care brands maintain broad product portfolios and global channels, and they remain important partners for channel presence and retail availability.

Specialist innovators have been the source of many high‑value features (wearable vitals, breathing monitoring, AI‑driven sleep coaching). These firms are the most active targets for strategic acquisitions and licensing deals.

Security and software capability is a decisive differentiator. Brands that demonstrate robust privacy engineering and clear data governance are winning both consumer trust and key retail placements.

Recent corporate movements underline these dynamics: a leading toy-turned-tech brand consolidated its position as the most trusted name in several core markets in 2025, while a prominent wearable‑monitor company expanded its product line to integrate camera and sock-based vitals monitoring in late 2025. These developments exemplify how brand trust and product innovation continue to co-evolve.

Regulation is shaping product architecture as much as consumer preference. Several regulatory developments are especially material for 2026 strategies:

State and national security requirements that mandate encryption, certificate‑based authentication, and the elimination of unauthenticated remote access are now influencing baseline product security design.

Privacy frameworks — including AI‑specific rules in some jurisdictions and children’s data protections — push vendors toward transparency, minimization of data collection, and favoring edge processing for sensitive signals.

Documented IoT security incidents and growing consumer awareness are raising expectations for third‑party certification and visible trust marks; brands that proactively pursue independent audit and certification will extract pricing and distribution advantages.

For product teams, the implication is clear: incorporate privacy-by-design and secure provisioning early, adopt modular architectures that enable regional feature gating, and build a certification roadmap as part of the product launch plan.

Prioritize secure, modular firmware and certificate‑based device provisioning to meet both consumer expectations and regulatory baselines.

Define a staged AI strategy: begin with edge analytics for sensitive signals and augment with cloud services that deliver differentiated insights while keeping data minimization front and center.

Adopt an “availability-first” channel strategy: maintain presence in online retail while using curated retail partnerships to reinforce trust and serviceability for premium buyers.

Use a value ladder pricing approach: bundle monitoring hardware with subscription‑based analytics for recurring revenue while preserving a low‑friction entry product to sustain adoption.

Build an M&A watchlist focused on AI/vision startups and wearable sensor specialists to accelerate access to proprietary features and speed-to-market.

The full PW Consulting report functions as both a strategic compass and an operational manual. Product leaders will find prioritized feature roadmaps and engineering specs; commercial teams will find channel and pricing models; legal and compliance teams will find templates and jurisdictional checklists. For boards and investors, the report translates the market’s macro growth trajectory into scenario-based revenue and ROI projections tailored to acquisition, organic growth, and partnership plays.

We intentionally omit detailed regional and product-line breakdowns in this brief to preserve the “trailer” intent: the full report contains the granular tables, segmentation matrices, and company‑level revenue modeling that underpin the strategic recommendations summarized here.

Request the complete dataset and modeling workbook to run bespoke scenarios aligned to your cost structure and channel mix.

Engage PW Consulting for a 6‑week strategic sprint to convert the report’s playbooks into an executable 12‑month plan, including an M&A diligence framework and a regulatory compliance timeline.

Use our certification roadmap to sequence product launches by jurisdiction and reduce time-to-market friction from security and privacy audits.

In an industry that sits at the intersection of intimate consumer trust, fast‑moving product innovation, and tightening regulatory expectations, the ability to synthesize macro momentum with operational discipline will determine winners in 2026 and beyond. PW Consulting’s Baby Monitoring System Market report equips leadership teams with the scenarios, playbooks, and risk maps needed to act decisively — while the full report provides the granular data you will need to implement and measure success.

Contact PW Consulting to access the full report, datasets, and bespoke advisory services that translate this strategic preview into a competitive roadmap for 2026.

For detailed analysis of this topic, please visit the official page:Baby Monitoring System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com