Automotive Body Repair Fillers Market — Strategic Preview for 2026

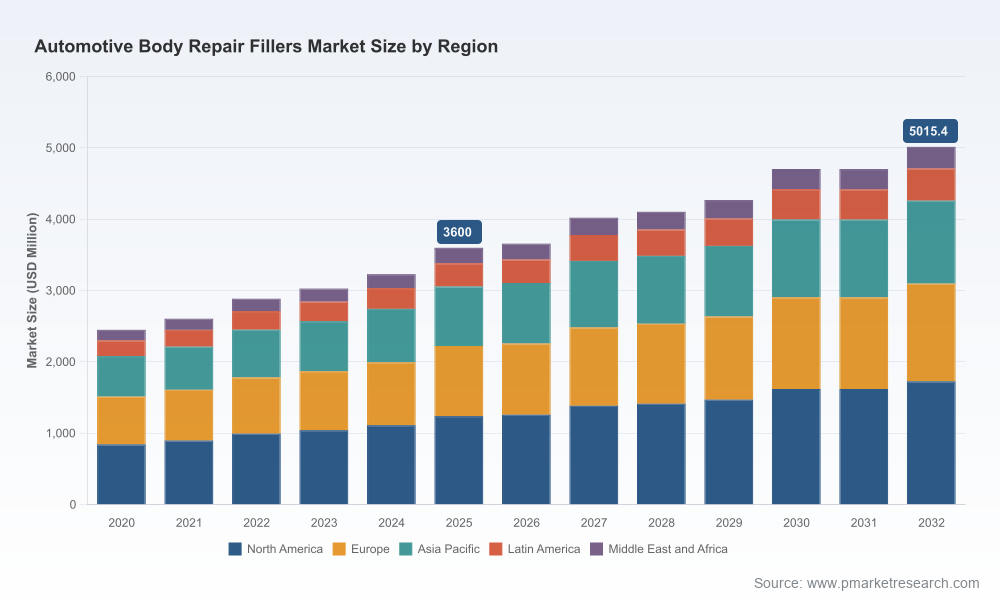

PW Consulting’s latest market research on the global Automotive Body Repair Fillers market is designed as a strategic playbook for executives planning investments, product launches, supply-chain hedges, and M&A activity in 2026. The 2025 base-year study places the market at approximately USD 3,600 Million and establishes a 2026–2032 compound annual growth rate (CAGR) of 4.85%, reaching roughly USD 5,015 Million by 2032. This release highlights the macro drivers, competitive moves, and tactical responses that will matter most next year — while intentionally withholding granular segment tables to encourage access to the full report for transaction‑level detail.

Automotive Body Repair Fillers Market

Market Snapshot and Near-Term Outlook

The body repair fillers market is in a phase of steady expansion. Growth is supported by a combination of a rising global vehicle parc, resilient collision repair volumes in mature markets, and increasing adoption of refinishing and restoration services in emerging regions. At the same time, structural changes in vehicle construction (aluminum, high-strength steels, and composites), coupled with professionalization of collision repair shops, are shifting product requirements toward lightweight, fast-curing, and multi‑substrate formulations.

Automotive Body Repair Fillers Market

Key headwinds include raw-material volatility and regulatory pressure. Unsaturated polyester resin prices have swung by more than 40% between 2020 and 2025, demonstrating the supply-side risk that directly compresses margins for formulators. Petroleum‑derived feedstock exposure remains a strategic vulnerability, and European regulatory scrutiny — including ECHA evaluations of styrene under REACH — could add compliance costs or restrict legacy polyester formulations. These factors are material to any 2026 procurement, R&D, or pricing decision.

Automotive Body Repair Fillers Market

Strategic Implications for 2026 Decision‑Making

- Procurement and Raw‑Material Risk Management: With resin and petrochemical inputs remaining volatile, leading firms should employ multi-scenario cost models, extend hedging horizons where practical, and negotiate index‑linked supplier contracts. Dual-sourcing and qualifying secondary suppliers in low-cost geographies reduce single‑point risk.

- Product Portfolio Prioritization: Expect stronger demand for rapid-cure, low‑VOC, and low‑styrene or styrene‑free formulations. Investing selectively in water‑based, UV‑curable, or hybrid chemistries addresses both regulatory risk and shop productivity demands. Prioritize product roadmaps that deliver faster cycle times and lower sanding effort — attributes repeatedly cited by bodyshops.

- Manufacturing and Quality Control: Vacuum processing and better degassing controls reduce pinholes and rework — important differentiators in premium segments. Automation of batch control and traceability are cost‑effective ways to improve yield and meet professional customers’ quality expectations.

- Pricing and Contracting: Implement transparent raw‑material surcharges and indexation clauses in commercial agreements. Invest in a cost‑pass‑through model to balance margin protection with competitive positioning in price‑sensitive channels.

- Go‑to‑Market and Channel Strategy: Reinforce installer loyalty through certified training programs, digital application guides, and bundled service offerings (product + training + warranty). Private‑label partnerships and distributor exclusives will remain effective for scale, but brand owners should protect margin by offering value‑added services.

- Regulatory Readiness and Sustainability: Prepare for potential restrictions on styrene-containing systems with a regulatory heatmap and phased reformulation program. Sustainability claims are becoming commercially relevant — Lifecycle Assessment (LCA) and improved occupational safety messaging can be leveraged in both B2B and DIY segments.

- M&A and Portfolio Optimization: The market’s moderate concentration creates opportunities for tuck‑ins and capability buys (e.g., niche chemistries, UV‑cure expertise, or regional distribution networks). Set clear return thresholds and integration playbooks focused on formulation IP and channel synergies.

Competitive Landscape: What Leading Players Signal

The sector combines multinational chemical majors, specialist formulators, and agile regional producers. Concentration metrics indicate a market that is neither fully fragmented nor dominated by a handful of players — the top three and top five firms collectively account for a notable, but not overwhelming, share of industry sales. That dynamic creates room for both premium differentiation and cost‑focused competition.

- ITW Evercoat (Cleveland, Ohio) — Known for premium and lightweight ranges (e.g., Rage, EverGold, Z‑Grip), Evercoat’s emphasis on sandability and minimal pinholing targets professional collision repair shops. The company’s October 2025 product refresh — including a Light Speed Premium Lightweight Filler and a UV‑cure primer showcased at SEMA — signals a push into faster‑turnaround, technician‑productivity solutions.

- 3M (St. Paul, Minnesota) — 3M’s portfolio spans Platinum and Lightweight Body Fillers and benefits from proprietary processing techniques (vacuum processing) and cross‑platform chemistry. The group’s global distribution and brand recognition allow it to compete across both premium professional and mass DIY segments, including through the Bondo brand.

- U.S. Chemical & Plastics (USC) — With products like Feather‑Rite, USC competes on spreadability and workability for professional markets. Its strengths are operational flexibility and responsiveness to shop preferences.

- U‑POL (UK) — U‑POL’s high‑performance fillers (e.g., Flyweight Gold) target adhesion and finishing attributes important to refinish technicians, reinforcing a premium positioning in Europe and select export markets.

- AkzoNobel — AkzoNobel’s refinish portfolio, including UV‑capable solutions, leverages coatings expertise to deliver curing-speed advantages and integration with finishing systems.

- SYNEW (China) — A competitive regional supplier producing high‑performance fillers for global distributors and local workshops. Cost advantage and supply proximity make such players influential in price‑sensitive regions.

Collectively, these firms demonstrate two concurrent strategic plays: (1) chemistry and process innovation to command premium pricing, and (2) channel and cost optimization to defend volume. Watch for partnerships between formulators and equipment/curing providers as a way to create integrated productivity propositions.

Practical Content in the Full PW Consulting Report

PW Consulting’s full study is built for action. Practical deliverables include:

- Interactive demand-forecast model (scenario‑driven, customizable by input assumptions)

- Raw‑material risk matrix and supplier stress tests

- Cost pass‑through and pricing toolkit with a sample contract clause language

- Regulatory heatmap (including potential REACH/styrene impacts and mitigation paths)

- Technology readiness assessment for water‑based, UV and hybrid chemistries

- Go‑to‑market playbooks for professional vs DIY channels, including distributor scorecards and training program templates

- M&A screening framework and shortlist methodology (deal rationale, valuation multiples, integration risks)

- Operational KPIs and production benchmarking templates

These assets are intentionally prescriptive — designed to minimize execution ambiguity for commercial, R&D, and procurement teams. To maintain the report’s role as an actionable purchase, we withhold the granular segmentation tables, regional shares, and application‑level numerical line items from this preview.

Recommended Near‑Term Roadmap for 2026

- 0–90 days: Run a sensitivity analysis using three raw‑material price scenarios; revise supplier contracts with short‑term hedges and contingency suppliers.

- 3–6 months: Fast‑track pilot formulations for low‑styrene or UV‑curable variants; initiate field trials in high‑value professional shops and capture technician feedback.

- 6–12 months: Deploy commercial trials with selected distributors, implement indexed pricing mechanisms, and evaluate one strategic bolt‑on acquisition or distribution partnership to expand capability or footprint.

Conclusion — Why This Matters for 2026

The body repair fillers market offers durable growth but is being reshaped by material science, regulation, and supply‑chain volatility. For executives, 2026 is a pivotal year to convert strategic intentions into concrete capabilities: secure input cost resilience, accelerate reformulation where regulation and customer productivity demand, and sharpen channel value propositions. PW Consulting’s full report provides the models, regulatory detail, and commercial tools you need to prioritize investments and de‑risk execution — including the granular segment and regional data not disclosed in this preview.

Access the full report on our website to obtain the detailed segmentation, downloadable models, and supplier benchmarking tables necessary for transaction‑level decisions in 2026.

For detailed analysis of this topic, please visit the official page:Automotive Body Repair Fillers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com