Europe Heart Failure Software Market Overview: Key Drivers and Challenges

Other |

2026-03-16 08:53:41

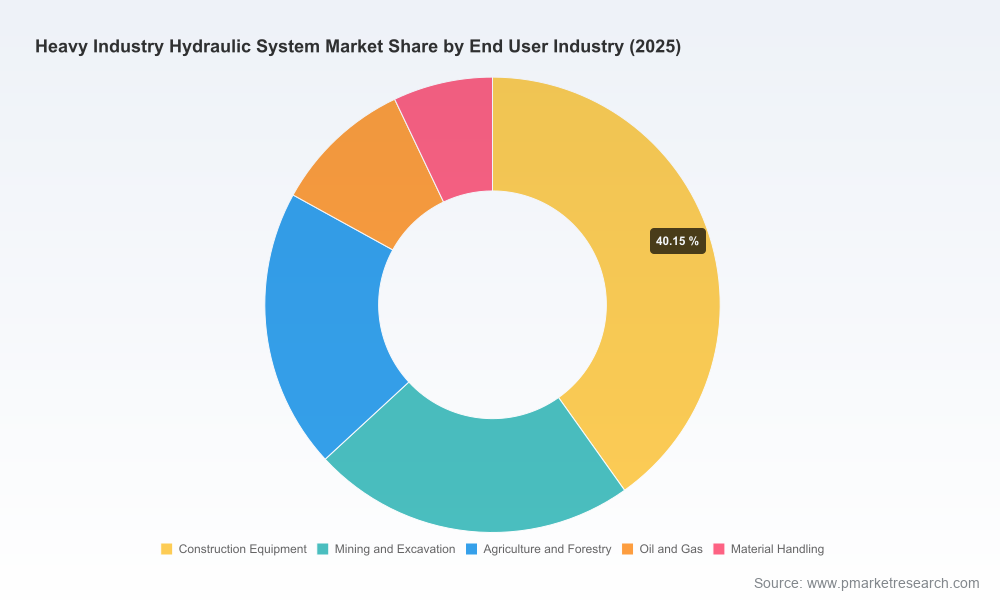

As heavy industry transitions toward higher efficiency, tighter regulations, and selective electrification, hydraulic systems remain a foundational technology across construction, mining, material handling and other heavy-duty applications. Our new PW Consulting market study — grounded in a 2020–2025 historical baseline and a 2026–2032 forecast horizon — shows the global heavy industry hydraulic systems market reached roughly USD 40.8 billion in 2025 and is projected to grow at a 4.85% CAGR through the forecast window. By 2032 the market is expected to be materially larger, underscoring steady, investable demand for both core hydraulic hardware and the adjacent service and systems business models.

Heavy Industry Hydraulic System Market

Decision-grade foresight: The pace of technology adoption (electrified power units, digitally enabled controls, energy-optimization standards) and material-cost volatility mean that mid- and long-range capital plans made in 2026 must be stress-tested across regulatory and input-price scenarios. This study provides scenario outputs that translate market trajectories into actionable capex and sourcing windows.

Heavy Industry Hydraulic System Market

Risk-adjusted supplier playbooks: With a moderately concentrated market structure — where the top three players control roughly one-third of the market and the top five approach the mid-forties in aggregate share — procurement teams must balance the benefits of incumbent scale against the agility and cost profiles of regional specialists. Our analysis enables procurement to quantify trade-offs between single-source partnerships and diversified supplier strategies.

Heavy Industry Hydraulic System Market

Revenue mix optimization: For OEMs and aftermarket services providers, the study quantifies where margin expansion is likeliest — not only through unit sales, but via electrified retrofit packages, predictive-maintenance subscriptions, and parts-as-a-service offerings that capitalize on fleet digitalization.

The market’s path over 2020–2025 reflects resilience with episodic impacts from macro and supply-side shocks: an expansion phase followed by a transient adjustment period, then renewed growth into 2024–2025 as capital spending resumed in heavy construction and mining. Looking forward, a steady mid-single-digit CAGR reflects the combined effect of continued demand for heavy-duty mechanical power, the rise of energy-efficiency upgrades mandated by new standards, and selective substitution as electrification captures specific use cases.

Three structural forces will shape outcomes through 2032:

Regulatory acceleration: Standards such as ISO 18464:2025, which codify design methodologies to minimize energy consumption in hydraulic fluid power systems, will drive product redesign and create first-mover advantages for suppliers who can demonstrate compliance and tangible lifecycle energy savings.

Input-cost volatility: Steel and other commodity price swings materially affect component production economics (cylinders, housings, valve bodies). Manufacturers that combine flexible sourcing, modular design, and value-engineered alloys will better defend margin.

Technology convergence: The integration of electrified hydraulic power units (eHPUs), advanced servo controls, and machine-level telematics is shifting value from discrete components to system-level solutions and service contracts.

The competitive map is characterized by global engineering leaders, diversified conglomerates, and regional specialists. Established players emphasize system integration, durability and scale; several regional and niche players are advancing in electrified and purpose-built hydraulics for off-highway and mobile work.

Bosch Rexroth AG: Strong in connected and energy-efficient industrial hydraulics, with deep integration into steel processing and heavy machinery OEMs. Companies evaluating system-level partnerships should weight Rexroth’s engineering footprint and digital integration capabilities.

Parker Hannifin Corporation: Offers a broad portfolio and engineered solutions with strong aftermarket and sustainability positioning, making them a logical partner for fleets seeking retrofit and predictive-maintenance pathways.

Danfoss Power Solutions: Focused on energy efficiency and electrification integration; well suited to co-develop hybrid and eHPU architectures with OEMs pursuing decarbonization roadmaps.

Eaton Corporation: Emphasizes high-pressure and durable solutions for the harshest applications. Where uptime and serviceability define procurement criteria, Eaton remains a benchmark supplier.

HYDAC, HAWE, Bucher, Linde, Kawasaki, KYB, Caterpillar, and others: These firms represent a mix of component specialists and system integrators that collectively define a competitive ecosystem. Regional champions can unlock lower-cost, faster-delivery options; global players deliver scale, R&D depth and warranty breadth.

Recent industry activity reinforces these directional shifts. The 2026 trade show cycle showcased purpose-built hydraulic cylinders, next-generation mobile hydraulic solutions and eHPUs — validating both continued demand for classical hydraulic robustness and accelerating innovation toward electrified and digitally managed systems. An awarded eHPU at the 2026 World Ag Expo exemplifies how product innovation is already moving into commercial validation.

We designed the report to be operationally useful for strategy, procurement, product and corporate development teams. Highlights include:

Market sizing and quantified outlook (2020–2032) with scenario pathways that map to capex timing decisions.

Competitive scorecards and supplier capability matrices — evaluating engineering depth, electrification readiness, aftermarket footprint, and supply-chain resilience — presented without disclosing confidential segment-level market shares so users can judge fit for purpose.

TCO and lifecycle models comparing conventional hydraulics, hybrid/eHPU solutions and electrified alternatives under multiple regulatory and commodity-price scenarios.

Go-to-market frameworks for OEMs and service providers to monetize digital offerings (subscription models, fleet analytics, retrofit bundles) and capture aftermarket growth.

M&A playbook and valuation sensitization: targets by capability set (controls/software, power units, filtration) and integration risk checklists.

Operational playbooks: procurement hedging strategies, dual-sourcing templates, and inventory policies designed specifically for hydraulic component supply chains under commodity volatility.

Compliance and product design guidance aligned to ISO 18464:2025 to accelerate time-to-market for energy-optimized systems.

Prioritize retrofitable electrification pathways: For many fleets, early ROI will come from hybridization and eHPU retrofits rather than full electrification. Build pilot programs that capture operational data and create repeatable retrofit packages.

Embed energy-efficiency as a product differentiator: Certify designs against ISO 18464 and quantify lifecycle energy savings in bids; dozens of prospective buyers now treat verified energy metrics as procurement filters.

Rebalance supplier portfolios: Combine proven global suppliers for mission-critical components with regional specialists to reduce lead times and cost exposure. Use supplier scorecards to operationalize this balance.

Monetize service and data: Convert telemetry into predictive maintenance offers and outcome-based contracts. Even modest adoption of subscription pricing materially improves lifetime gross margins.

Stress-test supply chains for steel price shocks and sourcing disruptions: Execute hedging pilots, material-substitution R&D, and dual-sourcing contracts for long-lead components.

Invest in systems engineering capability: The competitive frontier is shifting to integrated electro-hydraulic architecture and software controls — make systems-level competence a hiring and M&A priority.

Use the study as the primary market intelligence input for Q2–Q3 2026 capital allocation and supplier negotiation rounds. Apply the report’s TCO templates to at least three prioritized projects (e.g., new product launch, fleet retrofit program, aftermarket subscription pilot) and use the scenario outputs to define trigger points for accelerated investment or restrained spending.

If you are a corporate strategist, the report’s M&A playbook helps prioritize targets that close capability gaps with minimal integration drag. For procurement leaders, the supplier matrices and risk-adjusted sourcing frameworks give immediate negotiation levers tied to service-level economics. For product teams, our ISO-aligned design checklist and eHPU performance benchmarks compress time to compliant, saleable solutions.

This release purposefully highlights the report’s strategic value while reserving full segment-level tables and proprietary supplier scoring for the complete report package. For executive teams seeking the detailed regional, component and end-user split data, the supplier-by-capability dossiers, and exportable TCO models, visit our report page to access the full dataset and downloadable decision-support tools.

PW Consulting’s Heavy Industry Hydraulic System Market study is engineered to convert data into defensible decisions in 2026 — enabling you to prioritize investments, hedge risks, and capture the margin-rich opportunities created by the electrification and digitization of heavy hydraulic systems.

For detailed analysis of this topic, please visit the official page:Heavy Industry Hydraulic System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com